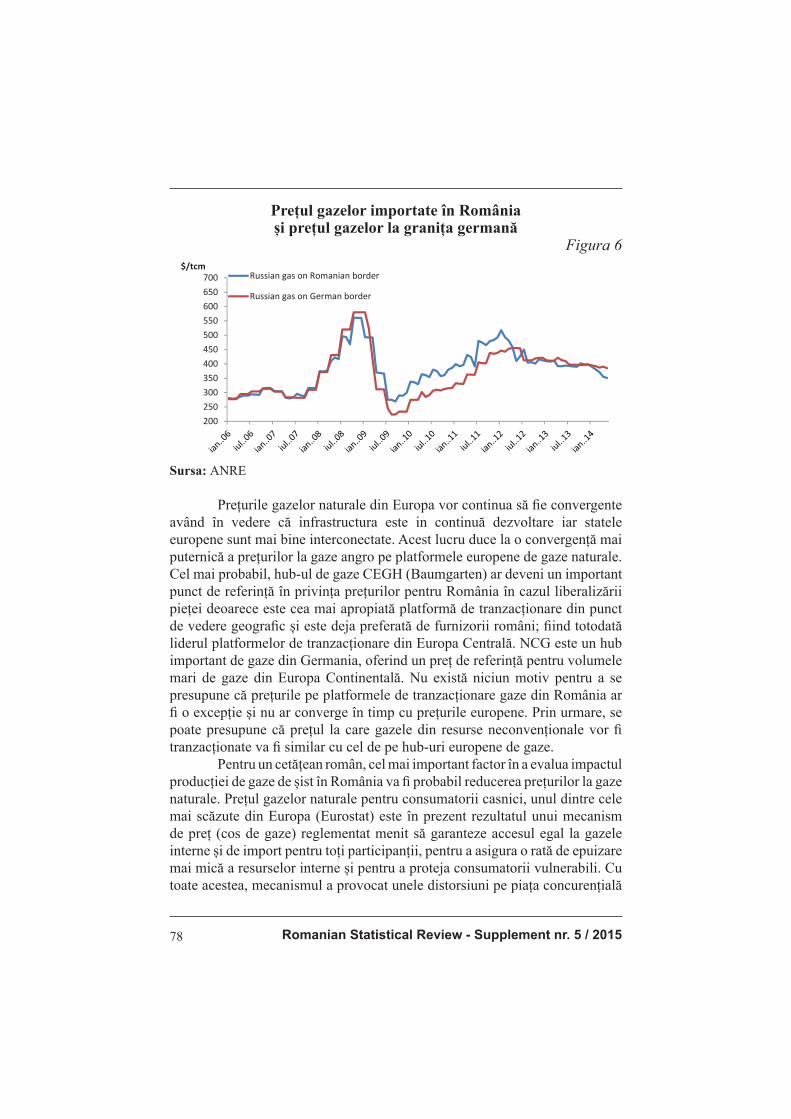

REVISTA ROMÂNĂ DE STATISTICĂ SUPLIMENT SUMAR / … · 2015-06-30 · Revista Română de...

100

Revista Română de Statistică - Supliment nr. 5 / 2015 SUMAR / CONTENTS 5/2015 REVISTA ROMÂNĂ DE STATISTICĂ SUPLIMENT SCENARII DE REGIONALIZARE: ANALIZĂ ASUPRA INDUSTRIEI DIN ROMÂNIA FOLOSIND STATISTICA INFORMAŢIONALĂ ONICESCU 3 SCENARIOS FOR REGIONALIZATION: ANALYSIS ON ROMANIA’S INDUSTRY USING ONICESCU INFORMATIONAL STATISTICS 11 Drd. Ioana-Ruxandra Lie Academia de Studii Economice din Bucureşti ANALIZA INTENŢIEI DE ÎNTOARCERE A ROMÂNILOR DIN SPANIA 19 AN INVESTIGATION OF ROMANIANS’ RETURN INTENTIONS FROM SPAIN 31 Elena-Maria Prada Academia de Studii Economice din Bucureşti STUDIU COMPARATIV DE CONVERGENŢĂ REGIONALĂ NUTS3 PE ŢĂRI DIN UE 43 CONVERGENCE REGIONAL STUDY COMPARING EU MEMBER STATES 55 Drd. Natalia Dumitrescu (Moroianu) Academia de Studii Economice, Bucureşti PRINCIPALELE VARIABILE ÎN EVALUAREA IMPACTULUI GAZELOR DE ŞIST ASUPRA PREŢURILOR ENERGIEI 66 KEY DETERMINANTS OF SHALE GAS IMPACT ON ENERGY PRICES 84 Drd. Valentina Ivan Academia de Studii Economice www.revistadestatistica.ro/supliment

Transcript of REVISTA ROMÂNĂ DE STATISTICĂ SUPLIMENT SUMAR / … · 2015-06-30 · Revista Română de...

Revista Română de Statistică - Supliment nr. 5 / 2015

SUMAR / CONTENTS 5/2015REVISTA ROMÂNĂ DE STATISTICĂ SUPLIMENT

SCENARII DE REGIONALIZARE: ANALIZĂ ASUPRA INDUSTRIEI DIN ROMÂNIA FOLOSIND STATISTICA INFORMAŢIONALĂ ONICESCU 3

SCENARIOS FOR REGIONALIZATION: ANALYSIS ON ROMANIA’S INDUSTRY USING ONICESCU INFORMATIONAL STATISTICS 11

Drd. Ioana-Ruxandra Lie Academia de Studii Economice din Bucureşti

ANALIZA INTENŢIEI DE ÎNTOARCERE A ROMÂNILOR DIN SPANIA 19 AN INVESTIGATION OF ROMANIANS’ RETURN INTENTIONS FROM SPAIN 31 Elena-Maria Prada Academia de Studii Economice din Bucureşti

STUDIU COMPARATIV DE CONVERGENŢĂ REGIONALĂ NUTS3 PE ŢĂRI DIN UE 43

CONVERGENCE REGIONAL STUDY COMPARING EU MEMBER STATES 55 Drd. Natalia Dumitrescu (Moroianu) Academia de Studii Economice, Bucureşti

PRINCIPALELE VARIABILE ÎN EVALUAREA IMPACTULUI GAZELOR DE ŞIST ASUPRA PREŢURILOR ENERGIEI 66

KEY DETERMINANTS OF SHALE GAS IMPACT ON ENERGY PRICES 84 Drd. Valentina Ivan Academia de Studii Economice

www.revistadestatistica.ro/supliment

Romanian Statistical Review - Supplement nr. 5 / 20152

Revista Română de Statistică, editată de Institutul Naţional de Statistică, este unica publicaţie de specialitate din ţara noastră, în domeniul teoriei şi practicii statistice. Articolele publicate se adresează oamenilor de ştiinţă, cercetătorilor, precum şi utilizatorilor de date şi informaţii statistice interesaţi în lărgirea şi aprofundarea orizontului cunoaşterii prin asimilarea noţiunilor de specialitate, abordarea de noi lucrări şi studii de referinţă pe care să le aplice ulterior în domeniul în care îşi desfăşoară activitatea. Prin prezentarea unor lucrări ştiinţifi ce şi de promovare a culturii statistice, necesară în economia de piaţă funcţională, revista se doreşte a fi un spaţiu propice schimbului de idei şi, totodată, o provocare. Orice studiu sau opinie care poate contribui la dezvoltarea gradului de înţelegere a statisticii ca ştiinţă este binevenit.

The Romanian Statistical Review, issued by the National Institute of Statistics, is in our country specialising in the fi eld of statistical theory and practice. The articles published are addressed to the scientists, researchers and statistical data and information users interested in broadening and deepening their horizon of knowledge by acquiring specialised notions and coming into contact with new papers and reference studies they can later apply in their own fi eld. Through the presentation of papers that are scientifi c in nature and that promote statistical culture, which is necessary in a functional market economy, the Review aims to be a favourable space for exchange of ideas and a challenge at the same time. Any study or opinion that can contribute to the development of the degree understanding statistics as a science is welcome.

La Revue Roumaine de Statistique, éditée par l’Institut National de la Statistique, est la seule publication de spécialité de notre pays dans le domaine de la théorie et de la pratique statistique. Les articles y étant publiés s’adressent aux scientifi ques, aux chercheurs, ainsi qu’aux utilisateurs de données et d’informations statistiques, intéressés d’élargir leur horizon de connaissances avec des notions de spécialité et de nouveaux travaux et études de référence qu’ils peuvent appliquer ultérieurement dans leurs domaines d’activité. Par la présentation de certains ouvrages scientifi ques et de promotion de la culture statistique nécessaires dans l’économie de marché fonctionnelle, la Revue se veut être un espace propice à l’échange d’idées et en même temps une provocation. Toute étude et opinion qui pourraient contribuer au développement du degré de compréhension de la statistique en tant que science sont bienvenues.

Revista Română de Statistică - Supliment nr. 5 / 2015 3

Scenarii de regionalizare: analiză asupra industriei din România folosind statistica

informaţională Onicescu Drd. Ioana-Ruxandra Lie

Academia de Studii Economice din Bucureşti, [email protected]

Abstract

Am arătat că este necesar să luăm în considerare mai multe criterii pentru a lua o decizie cu privire la formula optimă de regionalizare a României. Obiectivul acestei lucrări este de a studia unul din aceste criterii, respectiv sectorul industrial. Cu ajutorul instrumentelor oferite de statistica informaţională Onicescu analizăm omogenitatea regiunilor României în ceea ce priveşte două variabile, indicele producţiei industriale şi indicele valoric al cifrei de afaceri din industrie. Am descoperit că din acest punct de vedere regiunile nu sunt omogene, ceea ce duce la concluzia că industria este un aspect care poate fi luat în considerare atunci când se decide cu privire la regionalizare. Clasifi care JEL: C49, L60, L70, R13 Cuvinte-cheie: regionalizare, industrie, statistică informaţională, energie informaţională

Introducere

Regionalizarea a fost în ultimii ani un important subiect de discuţie în România, datorită faptului că Uniunea Europeană se concentrează pe regiuni ca bază a cooperării la nivelul continentului. Cum regiunile noastre de dezvoltare nu au personalitate juridică, este necesar să o obţină, dar, înainte de acesta, este nevoie să fi e găsită formula optimă de regionalizare, capabilă să stimuleze dezvoltarea. Această lucrare este a doua parte a unui studiu mai extins, realizat cu scopul de a găsi structura optimă pentru fi ecare regiune din cele menţionate anterior. Aici ne concentrăm pe studierea industriei României, a omogenităţii regiunilor din acest punct de vedere şi a relaţiei dintre variabile din domeniul industriei. Realizând o analiză cu ajutorul instrumentelor oferite de statistica informaţională Onicescu am ajuns la concluzia că există o legătură între indicele producţiei industriale şi indicele valoric al cifrei de afaceri din industrie. În plus, am afl at că regiunile nu sunt omogene în ceea ce priveşte

Romanian Statistical Review - Supplement nr. 5 / 20154

industria, ceea ce înseamnă că variabilele din acest domeniu pot fi utilizate pentru a decide asupra formulei optime de regionalizare. Prima parte a lucrării prezintă principalele caracteristici ale industriei României, concentrându-se pe evoluţia acestui sector după sfârşitul perioadei comuniste şi, de asemenea, pe consecinţele recentei crize economice. A doua parte a lucrării se referă la datele şi metodele folosite pentru a realiza analiza, şi este urmată de prezentarea rezultatelor obţinute. Lucrarea se încheie cu câteva concluzii şi direcţiile pentru cercetarea ulterioară.

Evoluţia şi caracteristicile sectorului industrial din România

Unul din principalele obiective ale regionalizării este de a crea structuri care ar creşte şi stimula dezvoltarea în România, iar industria are un rol important în dezvoltare. De exemplu, Danciu (2012: 40-44) observă că una dintre cauzele subdezvoltării este predominanţa activităţilor rurale. În plus, conform altor autori, în prezent „industria trebuie să joace rolul cel mai important în noul model de dezvoltare a Uniunii Europene, pentru soliditatea şi viabilitatea economiei UE” (Chivu, L., Ciutacu, C., 2014: 157-166). Industria românească s-a dezvoltat în special în perioada comunistă, dar câteva sectoare industriale au apărut încă de dinainte, de exemplu sectorul extractiv şi cel energetic. Aşa cum subliniază Bulearcă et. all (2014: 106-112), România s-a afl at printre pionierii Europei şi ai lumii în ceea ce priveşte extracţia şi utilizarea gazelor naturale; tot ei observă şi faptul că avem o lungă istorie în alte domenii ale sectorului energetic, precum exploatarea cărbunelui, a petrolului, şi generarea de energie electrică în termocentrale şi în hidrocentrale. Dezvoltarea acestor sectoare a continuat şi în anii 1950 România era „pe unul dintre primele cinci locuri din lume în ceea ce priveşte producţia şi consumul de energie primară” (Bulearcă et. all, 2014: 106-112). După mulţi ani de producţie şi consum de enrgie în creştere, datorate industrializării intensive din perioada comunistă (Bulearcă et. all, 2014: 106-112), din 1990 am fost martorii unei schimbări în structura acestui sector: ca o consecinţă a scăderii consumului, acum se produce mai puţină energie electrică, iar contribuţia energiei electrice din termocentrale la producţia totală a scăzut, în timp ce parcurile de eoliene s-au extins” (Bădileanu et. all, 2014: 53-59). Trebuie menţionat şi fapul că, dintre toate sectoarele industriale din România, „cea mai mare creştere în termeni reali a valorii adăugate brute în 2010 faţă de 1990 a fost înregistrată în producţia şi vânzarea de energie electrică, termică, de gaze şi de apă caldă” (Chivu, L., Ciutacu, C., 2014: 157-166).

Revista Română de Statistică - Supliment nr. 5 / 2015 5

Cum acest studiu se concentrează asupra regiunilor României, este de asemenea important de menţionat faptul că acest sector nu este dezvoltat în mod egal în ţară: în 2013 „regiunile Sud-vest şi Sud-Est administrau aproape 60% din capacităţile din sistemul energetic”, iar aceste disparităţi tind să se accentueze, având în vedere că se prognozează continuarea dezvoltării parcurilor de eoliene, în timp ce producţia bazată pe combustibili fosili va scădea (Bădileanu et. all, 2014: 53-59). Un alt sector industrial important în România este industria automobilelor, nu doar pentru că „a devenit un motor al redresării economice în ultimii ani” (Dachin, A., Burcea, F. C., 2014: 207 -216), dar şi pentru că alte ramuri industriale sunt strâns legate de aceasta: industria metalurgică şi cea chimică, sectorul energetic, industria textilă, industria electrică şi a calculatoarelor (Dachin, A., Burcea, F. C., 2014: 207 -216). Deşi „piaţa europeană a automobilelor a fost grav afectată de criza economică” (Niminet, L. A., 2013: 108-114), iar vânzările au scăzut şi pentru producătorii români în 2010 şi 2011 (Niminet, L. A., 2013: 108-114), în timpul crizei „Industria automobilelor şi-a crescut contribuţia la export” (Dachin, A., Burcea, F. C., 2014: 207 -216). În plus, două din cele 35 de clustere industriale identifi cate pentru economia românească de către Management Authority for the Sectoral Operation Program în 2011 au fost din industria automobilelor: Dacia Renault şi Automobile Sud-Vest Oltenia (Dachin, A., Burcea, F. C., 2014: 207 -216). În ceea ce priveşte alte ramuri industriale, merită menţionat faptul că, per total, valoarea adăugată brută din industrie reprezintă cam 30% în majoritatea regiunilor, cu valori care depăşesc 35% în Centru şi Sud-Muntenia (Iordan, M., Chilian, M. N., 2014: 397-406). După 1990 industria românească este caracterizată de o scădere a gradului de concentrare, datorată liberalizării pieţei, şi, de asemenea, de o creştere a „ponderii capitalului străin, care deţine acum aproximativ 70% din cifra de afaceri din industrie” (Chivu, L., Ciutacu, C., 2014: 157-166). Pe de altă parte, mai ales între 1990 şi 2000, industria din România s-a confruntat cu „o dispariţie accelerată a mai mult de jumătate din producţia industrială, a infrastructurii tehnice şi de know-how, a competenţelor şi a muncii” (Chivu, L., Ciutacu, C., 2014: 157-166). Având în vedere această situaţie, este necesar să fi e luate în considerare caracteristicile sectorului industrial din fi ecare judeţ, pentru a decide asupra celei mai bune formule de regionalizare. Această analiză va fi realizată în următoarea secţine a lucrării de faţă.

Romanian Statistical Review - Supplement nr. 5 / 20156

Metodologie şi sursa datelor

Această analiză a fost realizată folosindu-se instrumente oferite de statistica informaţională Onicescu, precum energia informaţională şi proprietăţile sale. Datele folosite pentru realizarea studiului provin din „Buletinul Statistic Lunar al Judeţelor” emis în mai 2013 de către Institutul Naţional de Statistică al României. Aşa cum este menţionat în respectivul document, datele cu privire la industrie se referă la industria extractivă şi de manufacturare, la producţia şi furnizarea de electricitate, gaze naturale, apă caldă şi aer condiţionat. Cele două variabile folosite pentru analiză au fost indicii producţiei industriale şi indicii valorici ai cifrei de afaceri din industrie pe total (piaţa internă şi piaţa externă) corespunzători fi ecărui judeţ din România.

Analiza datelor

În prima etapă a studiului a fost cercetată existenţa unei legături între indicii producţiei industriale şi indicii valorici ai cifrei de afaceri din industrie, pe baza indicilor generali (01.01.-31.05.2013 faţă de 01.01-31.05.2012). De asemenea, s-a cercetat dacă această posibilă legătură este infl uenţată de structura regiunilor. În acest scop, a fost calculată frecvenţa de apariţie a unor indici sub 100%, respectiv peste 100% în fi ecare regiune. După aceea, au fost calculate energiile informaţionale şi câştigul informaţional. Calculele au fost realizate atât pentru actuala structură a regiunilor României, cât şi pentru versiunile propuse într-o lucrare anterioară (Lie, I. R, 2015). Rezultatele obţinute au condus la următoarele concluzii: - Pentru regiunea Nord-Vest se observă o infl uenţă importantă a indicelui producţiei industriale asupra indicilor cifrei de afaceri din industrie (câştig informaţional 35.56%). Infl uenţa a fost uşor mai scăzută (33.33%) în cazul versiunii fără judeţele Cluj and Bistriţa-Năsăud. - Pentru regiunea Vest infl uenţa este mult mai mică, dar îşi păstrează importanţa, având în vedere că depăşeşte 5%. Cu toate acestea, atunci când judeţul Hunedoara este exclus din regiune, se observă o creştere importantă a infl uenţei (de la 8.33 la 22.2%). O situaţie similară apare şi în regiunea Sud-Muntenia, dar aici infl uenţa indicelui producţiei industriale asupra indicilor cifrei de afaceri din industrie este mult mai mare, atât în formula din prezent, cât şi în cea din care sunt excluse judeţele Călăraşi şi Ialomiţa (17.01% pentru structura curentă şi 42.67% pentru formula propusă).

Revista Română de Statistică - Supliment nr. 5 / 2015 7

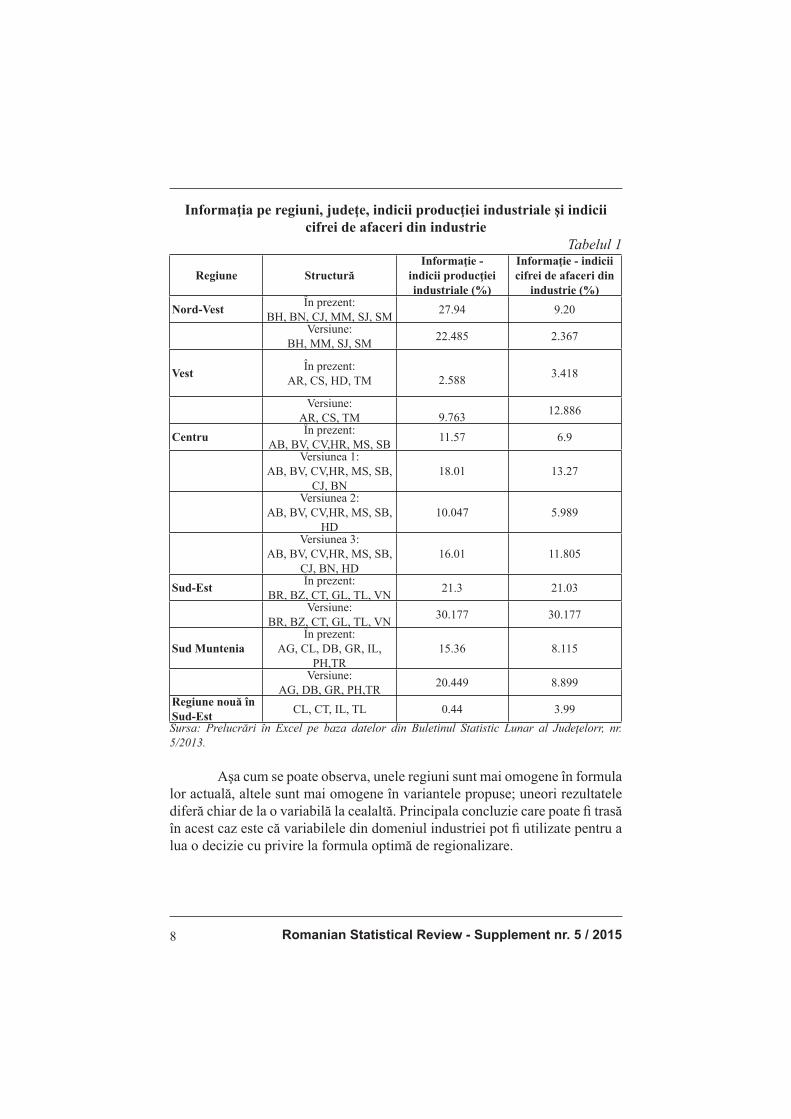

- Pentru regiunea Centru informaţia obţinută este zero; una din posibilele cauze ale acestei situaţii este faptul că aici toate judeţele au indicii cifrei de afaceri din industrie peste 100%, ceea ce face imposibile calculele tipice statisticii informaţionale. - În cazul noii regiuni propuse pentru a fi creată în Sud-Est, compusă din Tulcea, Constanţa, Călăraşi şi Ialomiţa, se poate demonstra o anumită infl uenţă a indicelui producţiei industriale asupra indicilor cifrei de afaceri din industrie, dar aceasta nu este foarte ridicată (8.3%). A doua parte a analizei se referă la omogenitatea regiunilor din România, din punctul de vedere al celor două variabile studiate anterior. Datele au fost grupate folosindu-se câte două criterii, judeţ şi frecvenţa indicilor producţiei industriale mai mari, respectiv mai mici de 100%, şi, de asemenea, judeţ şi frecvenţa indicilor cifrei de afaceri din industrie mai mari şi mai mici de 100%. Pasul următor a fost de a calcula energiile informaţionale, energiile informaţionale ajustate şi infl uenţele pentru fi ecare judeţ şi regiune. În Tabelul 1 sunt prezentate rezultatele obţinute în urma analizei indicilor producţiei industriale şi ai cifrei de afaceri din industrie pentru regiunile României.

Romanian Statistical Review - Supplement nr. 5 / 20158

Informaţia pe regiuni, judeţe, indicii producţiei industriale şi indicii cifrei de afaceri din industrie

Tabelul 1

Regiune StructurăInformaţie -

indicii producţiei industriale (%)

Informaţie - indicii cifrei de afaceri din

industrie (%)Nord-Vest În prezent:

BH, BN, CJ, MM, SJ, SM 27.94 9.20Versiune:

BH, MM, SJ, SM 22.485 2.367

Vest În prezent:AR, CS, HD, TM 2.588 3.418

Versiune:AR, CS, TM 9.763 12.886

Centru În prezent:AB, BV, CV,HR, MS, SB 11.57 6.9

Versiunea 1:AB, BV, CV,HR, MS, SB,

CJ, BN18.01 13.27

Versiunea 2:AB, BV, CV,HR, MS, SB,

HD10.047 5.989

Versiunea 3:AB, BV, CV,HR, MS, SB,

CJ, BN, HD16.01 11.805

Sud-Est În prezent:BR, BZ, CT, GL, TL, VN 21.3 21.03

Versiune:BR, BZ, CT, GL, TL, VN 30.177 30.177

Sud MunteniaÎn prezent:

AG, CL, DB, GR, IL, PH,TR

15.36 8.115

Versiune:AG, DB, GR, PH,TR 20.449 8.899

Regiune nouă în Sud-Est CL, CT, IL, TL 0.44 3.99Sursa: Prelucrări în Excel pe baza datelor din Buletinul Statistic Lunar al Judeţelorr, nr. 5/2013.

Aşa cum se poate observa, unele regiuni sunt mai omogene în formula lor actuală, altele sunt mai omogene în variantele propuse; uneori rezultatele diferă chiar de la o variabilă la cealaltă. Principala concluzie care poate fi trasă în acest caz este că variabilele din domeniul industriei pot fi utilizate pentru a lua o decizie cu privire la formula optimă de regionalizare.

Revista Română de Statistică - Supliment nr. 5 / 2015 9

Concluzii

Acest studiu asupra industriei din regiunile şi judeţele României face parte dintr-o cercetare mai extinsă, care are ca scop găsirea unei formule optime de regionalizare (nivelul NUTS 2) a ţării.Folosind instrumentele noi, oferite de statistica informaţională, am analizat legătura dintre două variabile importante din industrie, indicele producţiei industriale şi indicele cifrei de afaceri din industrie, precum şi infl uenţa structurii regiunilor asupra acestei legături. Am studiat de asemenea omogenitatea regiunilor, atât în structura lor actuală, cât şi în versiunile propuse, luând în considerare cele două variabile menţionate anterior.Rezultatul este că indicele producţiei industriale are o infl uenţă semnifi cativă asupra indicelui cifrei de afaceri din industrie; în unele cazuri infl uenţa este mai mare în structura actuală, în altele, în versiunile propuse.Am descoperit, de asemenea, că regiunile României nu sunt omogene în ceea ce priveşte industria, nici în forma lor prezentă, nici în variantele propuse. Aceasta înseamnă că decizia referitoare la formula optimă de regionalizare poate fi luată pe baza variabilelor din industrie, printre alte variabile din domenii precum comerţul sau turismul, care vor fi studiate în lucrări viitoare.

Acknowledgement

Această lucrare a fost cofi nanţată din Fondul Social European, prin Programul Operaţional Sectorial Dezvoltarea Resurselor Umane 2007-2013, proiect numărul POSDRU/159/1.5/S/134197 „Performanţă şi excelenţă în cercetarea doctorală şi postdoctorală în domeniul ştiinţelor economice din România”.

Surse bibliografi ce - Bădileanu, M., Băleanu, D., Georgescu, L. I. (2014), “Regional disparities of

the Romanian energy system”, 1st International Conference Economic Scientifi c Research - Theoretical, Empirical and Practical Approaches, ESPERA 2013, Procedia Economics and Finance, vol. 8: 53 – 59.

- Bulearcă, M., Neagu, C., Sima, C., Mărguș, D. (2014) “The Romanian extractive industry, from its early beginnings up to year 1948”, 1st International Conference Economic Scientifi c Research - Theoretical, Empirical and Practical Approaches, ESPERA 2013, Procedia Economics and Finance, vol. 8: 106 – 112.

- Chivu, L., Ciutacu, C. (2014) “About industrial structures decomposition and recomposition”, 1st International Conference Economic Scientifi c Research - Theoretical, Empirical and Practical Approaches, ESPERA 2013, Procedia Economics and Finance, vol. 8: 157 – 166.

Romanian Statistical Review - Supplement nr. 5 / 201510

- Dachin, A., Burcea, F. C., (2012) “Evaluations of Driving Effects of the Automotive Industry in the Romanian Economy – a Quantitative Analysis”, 7th International Conference on Applied Statistics, Procedia Economics and Finance vol. 10: 207 – 216.

- Danciu, A. R. (2012) “The ranking of the Romanian regions based on the potential to attract FDI”, WCBEM 2012, Procedia - Social and Behavioral Sciences, vol. 62: 40 – 44.

- Institutul Naţional de Statistică (2014) http://statistici.insse.ro/shop/ - Iordan, M., Chilian, M. N. (2014) “The sectoral structures in Romania, its regions and

the EU countries – key features of economic and social cohesion”, 1st International Conference Economic Scientifi c Research - Theoretical, Empirical and Practical Approaches, ESPERA 2013, Procedia Economics and Finance, vol. 8: 397 – 406.

- Lie, I.R, Mihaiţă N. V, (2014). “Regionalization: a few developed and applied methodologies”, in Proceedings of the Ninth International Conference on Economic Cybernetic Analysis Positive and Negative Effects of European Union and Eurozone Enlargement – PONE 2014, Editura ASE, București: 1-6.

- Lie, I.R (2015) “Scenarios for regionalization: analysis on Romania’s population using Onicescu informational statistics”, Romanian Statistical Review – Supplement, vol.3.

- Mihăiţă N. V. & Stanciu Capotă, R. (2003). “Relaţiile statistice puternice, ascunse, false şi iluzorii: aplicaţii ale statisticii informaţionale – ediţie bilingvă”, Editura ASE, Bucureşti.

- Mihăiţă N. V. (2001) “Metode cantitative în studiul pieţei – Statistica şi marketingul informaţional”, Editura Economică. Bucureşti.

- Onicescu, O. & Ştefănescu, V. (1979) „Elemente de statistică informaţională cu aplicaţii”, Editura Tehnică, Bucureşti.

- Niminet, L. A (2013) “The Automotive Market - An Ongoing Turmoil”, International Economic Conference of Sibiu 2013 Post Crisis Economy: Challenges and Opportunities, IECS 2013, Procedia Economics and Finance, vol. 6: 108-114.

Revista Română de Statistică - Supliment nr. 5 / 2015 11

SCENARIOS FOR REGIONALIZATION: ANALYSIS ON ROMANIA’S INDUSTRY USING ONICESCU INFORMATIONAL

STATISTICS PhD Student Ioana-Ruxandra Lie Bucharest University of Economic Studies

Abstract

We have shown that in order to make a decision regarding the optimal formula for Romania’s regionalization it is necessary to consider more than one criteria. The aim of this paper is to study one of these criteria – the industrial sector. Using instruments provided by Onicescu’s informational statistics we analyze the homogeneity of the Romanian regions regarding two variables, the industrial production index and the turnover value index in industry. We fi nd out that from this point of view regions are not homogeneous, which leads to the conclusion that industry is an aspect that can be considered when deciding on regionalization. JEL Classifi cation codes: C49, L60, L70, R13 Key words: regionalization, industry, informational statistics, informational energy

Introduction

Regionalization has been an important topic for discussion and research in Romania in the last few years, as the European Union focuses on regions as base for cooperation. As our development regions don’t have judicial personality, it is necessary to assign it to them, but, before that, it is necessary to fi nd the optimal structure for each region, in order to prompt development. This paper is the second part of a more extensive research, aiming to fi nd the optimal structure for each region that was mentioned above. Here, we focus on studying Romania’s industry, the homogeneity of its regions from this point of view and the connection between some variables from the industry fi eld. The analysis is carried out with the instruments provided by Onicescu’s informational statistics. As a result, we fi nd out that there is a connection between the industrial production index and the turnover value index in industry. More important, we also fi nd that regions are not homogeneous from

Romanian Statistical Review - Supplement nr. 5 / 201512

the industry’s point of view, which means that the variables from this fi eld can be used in order to decide on the optimal formula for regionalization. The fi rst part of the paper presents the main characteristics of Romanian industry, focusing on the evolution in this fi eld after the end of the communist era and, also, on the consequences of the more recent economic crisis. The second section of the paper focuses on the data and methods used in order to carry out the analysis, and it is followed the presentation of the results we obtained. We end with the conclusions and directions for further investigations.

Evolution and general characteristics of Romania’s industrial sector

One of the main reasons for regionalization is to create structures that would increase and stimulate development in Romania, and an important role in development is held by industry. For example, Danciu (2012: 40-44) notices that one of the causes of underdevelopment is the predominance of rural activities. Moreover, according to other authors, nowadays “industry is called to play the most important role in the new development model of the European Union, in the soundness and viability of the EU economy” (Chivu, L., Ciutacu, C., 2014: 157-166). Romanian industry developed especially in the communist era, but there were some industrial activities that emerged previously to that moment, for example extractive and energy sectors. As Bulearcă et. all (2014: 106-112) highlight, Romania was among the pioneers in the exploitation and use of natural gas, in Europe and in the world; they also notice that we have a long history with other areas of the energy sector, like coal mining, oil exploitation, and thermoelectric and hydroelectric power generation. The development of these sectors continued and by the 1950s, Romania was “among the top 5 places in the world in terms of production and consumption of primary energy” (Bulearcă et. all, 2014: 106-112). After many years of increasing production and consumption of energy due to the intensive industrialization in the communist era (Bulearcă et. all, 2014: 106-112), from the 1990s we have witnessed a change in the structure of this sector: as a consequence of the decrease in consumption, less electricity is now produced, the contribution of thermal energy to the total production has diminished, and wind farms have expanded (Bădileanu et. all, 2014: 53-59). It is worth mentioning that from all the industrial branches in Romania, “in real terms, the highest gross value added increment in 2010, by comparison to 1990, was recorded in the production and supply of electric power, heating, gas, hot water” (Chivu, L., Ciutacu, C., 2014: 157-166).

Revista Română de Statistică - Supliment nr. 5 / 2015 13

As we focus our study on Romania’s regions, it is also important to mention that this sector is not equally developed over the country: in 2013 “Sothwest and Southeast regions administered almost 60% of the capacities of the energy system”, and these disparities tend to increase as it is forecasted that wind farms will continue to expand, and production based on fossil fuels will decrease (Bădileanu et. all, 2014: 53-59). Another important industrial sector in Romania is the automotive industry, not only because it “became an engine for recovery in the last years”, (Dachin, A., Burcea, F. C., 2014: 207 -216), but also because there are other industrial branches strongly connected to this one: metallurgical industry, chemical industry, the energy sector, textile industry, electrical and computer industries (Dachin, A., Burcea, F. C., 2014: 207 -216). Even though the “European automotive market has been hit hard by the economic crisis” (Niminet, L. A., 2013: 108-114) and sales also dropped for Romanian producers in 2010 and 2011 (Niminet, L. A., 2013: 108-114), during this crisis “the automotive industry has increased its contribution to exports” (Dachin, A., Burcea, F. C., 2014: 207 -216). Moreover, two out of the 35 industrial clusters identifi ed for the Romanian economy by the Management Authority for the Sectoral Operation Program in 2011 were from the automotive industry: Dacia Renault and Automotive Southwest Oltenia (Dachin, A., Burcea, F. C., 2014: 207 -216). Regarding other industry sectors, it is worth mentioning that overall, the gross value added from industry is around 30% in most of the regions, with values that exceed 35% in Center and South Muntenia (Iordan, M., Chilian, M. N., 2014: 397-406). After 1990 Romanian industry is also characterized by a decrease in the degree of concentration, due to the market liberalization, and also by an increase of the “share of foreign capital, which is now holding some 70% of the turnover in industry” (Chivu, L., Ciutacu, C., 2014: 157-166). On the other hand, especially between 1990 and 2000, Romanian industry faced an “accelerated dissolution of more than half of the industrial production, technical and know-how infrastructure, competences, and labor” (Chivu, L., Ciutacu, C., 2014: 157-166). Considering this situation, it is necessary to take into account the characteristics of the industrial sector in each county in order to decide regarding the best formula for regionalization. This analysis will be carried out in the following section of the paper.

Romanian Statistical Review - Supplement nr. 5 / 201514

Methodology and data

This analysis was made using instruments provided by Onicescu’s informational statistics, like informational energy and its properties. The data used in order to complete the study was found in the “Statistical Monthly Bulletin of the Counties” issued in May 2013 by the Romanian National Institute of Statistics. As it is mentioned in this bulletin, data regarding industry refers to mining and quarrying, manufacturing, production and supply of electricity and heat, gas, hot water and air conditioning. The two variables used in order to perform this analysis were the industrial production index and turnover value index in industry for total (domestic and non-domestic markets) corresponding to each county in Romania.

Data analysis

The fi rst part of this study was to analyze, based on general indexes (01.01.-31.05.2013 to 01.01-31.05.2012), if there is a connection between industrial production indexes and those of turnover value. It was also studied if this possible connection is infl uenced by the regions’ structures. In order to achieve this, we calculated the frequency of occurrence of indexes below 100%, respectively above this value for each region. Then we calculated the weighted informational energies and the information gained. These calculations were made for the current composition of Romania’s regions, and also for the versions we proposed in a previous paper (Lie, I. R, 2015). The results obtained lead to the following conclusions: - For Northwest region there is an important infl uence of the industrial production index on the turnover value index in industry (information gain 35.56%). The infl uence was slightly lower (33.33%) in the case of the version without Cluj and Bistriţa-Năsăud counties. - For the West region the infl uence is much smaller, but it is still important, as it exceeds 5%. However, when excluding Hunedoara county from the region, a signifi cant increase in infl uence is noticed (from 8.33 to 22.2%). A similar situation occurs in South-Muntenia Region, but here the infl uence of the industrial production index on the turnover value index in industry is much higher both in the current formula and in the one excluding Călăraşi and Ialomiţa counties (17.01% for current situation, and 42.67% for the proposed version). - For the Center region the information obtained is zero; one of the

Revista Română de Statistică - Supliment nr. 5 / 2015 15

possible causes for this situation in the fact that here all the counties have the turnover value index in industry above 100%, which makes the calculations typical for informational statistics impossible. - In the current formula, it appears to be no connection between the two variables considered, in the Southeast region, but when excluding Tulcea and Constanţa counties, the infl uence increases signifi cantly (25%). - In the case of the new region proposed by us to be created in the Southeast of Romania, composed by Tulcea, Constanţa, Călăraşi and Ialomiţa, we can prove a certain infl uence of the industrial production index on the turnover value index in industry, but this is not very high (8.3%). The second part of the study is an analysis on the homogeneity of the regions in Romania, taking into account the two variables analyzed in the previous part. We grouped the data using two criteria, county and the frequency of industrial production indexes below and above 100%, and also county and the turnover value indexes in industry, below and above 100%. This was followed by the calculation of the informational energies, the adjusted informational energies and infl uences for each county and region. Table 1 presents the results obtained by analyzing the industrial production indexes and the turnover value indexes in industry for the Romanian regions.

Romanian Statistical Review - Supplement nr. 5 / 201516

Informational energies and information by regions, counties, industrial production indexes and turnover value indexes in industry

Table 1

Region StructureInformation -

industrial production indexes (%)

Information - turnover value indexes in

industry (%)Northwest Current:

BH, BN, CJ, MM, SJ, SM

27.94 9.20

Version:BH, MM, SJ, SM 22.485 2.367

West Current:AR, CS, HD, TM 2.588 3.418

Version:AR, CS, TM 9.763 12.886

Center Current:AB, BV, CV,HR, MS, SB 11.57 6.9

Version 1:AB, BV, CV,HR, MS,

SB, CJ, BN18.01 13.27

Version 2:AB, BV, CV,HR, MS,

SB, HD10.047 5.989

Version 3:AB, BV, CV,HR, MS,

SB, CJ, BN, HD16.01 11.805

Southeast Current:BR, BZ, CT, GL, TL, VN 21.3 21.03

Version:BR, BZ, CT, GL, TL, VN 30.177 30.177

South Muntenia

Current:AG, CL, DB, GR, IL,

PH,TR15.36 8.115

Version:AG, DB, GR, PH,TR 20.449 8.899

New region in the Southeast CL, CT, IL, TL 0.44 3.99Source: Excel calculations based on data from Statistical Monthly Bulletin of the Counties, no. 5/2013.

As it can be seen some of the regions are more homogeneous in their current formula, others are more homogeneous in the proposed versions; sometimes the results differ from one variable to the other. The main conclusion reached here is that when trying to decide on an optimal formula for regionalization, variables from the industry area can be used in order to make a decision.

Revista Română de Statistică - Supliment nr. 5 / 2015 17

Conclusions

This study on the industry in Romanian regions and counties is part of a more extensive research, aiming to fi nd an optimal formula for regionalization (NUTS 2 level) for Romania. Using the new instruments, provided by the informational statistics, we analyzed the relationship between two important variables in industry, the industrial production index and the turnover value index in industry, and the infl uence of the regions’ structure on this relationship. We also studied the homogeneity of the regions, both with their current structure and the proposed structures, taking into account the two variables mentioned before. The result is that the industrial production index has a signifi cant infl uence on the turnover value index in industry; in some cases this infl uence is bigger in the current situation, sometimes it is bigger in the proposed version. We also found that regions in Romania are not homogenous in terms of industry, in both current and proposed versions. This means that the decision on the optimal formula can be taken considering variables from industry, but also from other fi elds, like commerce and tourism, which will be studied in further works.

Acknowledgement

This work was cofi nanced from the European Social Fund through Sectoral Operational Programme Human Resources Development 2007-2013, project number POSDRU/159/1.5/S/134197 „Performance and excellence in doctoral and postdoctoral research in Romanian economics science domain”.

References

- Bădileanu, M., Băleanu, D., Georgescu, L. I. (2014), “Regional disparities of the Romanian energy system”, 1st International Conference Economic Scientifi c Research - Theoretical, Empirical and Practical Approaches, ESPERA 2013, Procedia Economics and Finance, vol. 8: 53 – 59.

- Bulearcă, M., Neagu, C., Sima, C., Mărguș, D. (2014) “The Romanian extractive industry, from its early beginnings up to year 1948”, 1st International Conference Economic Scientifi c Research - Theoretical, Empirical and Practical Approaches, ESPERA 2013, Procedia Economics and Finance, vol. 8: 106 – 112.

- Chivu, L., Ciutacu, C. (2014) “About industrial structures decomposition and recomposition”, 1st International Conference Economic Scientifi c Research - Theoretical, Empirical and Practical Approaches, ESPERA 2013, Procedia Economics and Finance, vol. 8: 157 – 166.

Romanian Statistical Review - Supplement nr. 5 / 201518

- Dachin, A., Burcea, F. C., (2012) “Evaluations of Driving Effects of the Automotive Industry in the Romanian Economy – a Quantitative Analysis”, 7th International Conference on Applied Statistics, Procedia Economics and Finance vol. 10: 207 – 216.

- Danciu, A. R. (2012) “The ranking of the Romanian regions based on the potential to attract FDI”, WCBEM 2012, Procedia - Social and Behavioral Sciences, vol. 62: 40 – 44.

- Institutul Naţional de Statistică (2014) http://statistici.insse.ro/shop/ - Iordan, M., Chilian, M. N. (2014) “The sectoral structures in Romania, its regions and

the EU countries – key features of economic and social cohesion”, 1st International Conference Economic Scientifi c Research - Theoretical, Empirical and Practical Approaches, ESPERA 2013, Procedia Economics and Finance, vol. 8: 397 – 406.

- Lie, I.R, Mihaiţă N. V, (2014). “Regionalization: a few developed and applied methodologies”, in Proceedings of the Ninth International Conference on Economic Cybernetic Analysis Positive and Negative Effects of European Union and Eurozone Enlargement – PONE 2014, Editura ASE, București: 1-6.

- Lie, I.R (2015) “Scenarios for regionalization: analysis on Romania’s population using Onicescu informational statistics”, Romanian Statistical Review – Supplement, vol.3.

- Mihaiţă N. V. & Stanciu Capotă, R. (2003). “Relaţiile statistice puternice, ascunse, false şi iluzorii: aplicaţii ale statisticii informaţionale – ediţie bilingvă”, Editura ASE, Bucureşti.

- Mihaiţă N. V. (2001) “Metode cantitative în studiul pieţei – Statistica şi marketingul informational”, Editura Economică. Bucureşti.

- Onicescu, O. & Ştefănescu, V. (1979) „Elemente de statistică informaţională cu aplicaţii”, Editura Tehnică, Bucureşti.

- Niminet, L. A (2013) “The Automotive Market - An Ongoing Turmoil”, International Economic Conference of Sibiu 2013 Post Crisis Economy: Challenges and Opportunities, IECS 2013, Procedia Economics and Finance, vol. 6: 108-114.

Revista Română de Statistică - Supliment nr. 5 / 2015 19

Analiza intenţiei de întoarcere a românilor din Spania

Elena-Maria Prada Bucharest Academy of Economic Studies

email: [email protected]

Abstract

Migrația este fenomenul care a însoțit fi ința umană de-a lungul vieții, oamenii căutând locuri potrivite traiului. Motivele pentru a migra au evoluat o data cu marile descoperiri ale lumii. În zilele noastre, conceptual de migrație este diferit din punctual de vedere al factorilor care o determină, dar motivul principal pentru a migra râmane bunăstarea. În analiza determinării factorilor migrației de revenire a românilor din Spania am utilizat chestionarul Institutului de Statistică din Spania ”Encuesta Nacional de Inmigrantes” din anul 2007. Rezultatele arată că înainte de începerea crizei fi nanciare intențiile de revenire nu erau atât de proeminente, totuși dacă persoana remitea în țara de origine sau avea o experiență sufi cientă în Spania existau și intenții de revenire, acest lucru confi rmând faptul că migrația nu era una permanentă, ci una temporară iar pe măsură ce scopul migrației era îndeplinit migrantul inteționa să revină. Cuvinte cheiei: revenire, migrație, probit, logit, Romania. JEL Classifi cation codes: C01,C30, O15

Introducere

Migrația este fenomenul care a însoțit fi ința umană de-a lungul vieții, oamenii căutând locuri potrivite traiului. Motivele pentru a migra au evoluat o data cu marile descoperiri ale lumii. În zilele noastre, conceptul de migrație este diferit din punctual de vedere al factorilor care o determină, dar motivul principal pentru a migra râmane bunăstarea. Migrația de întoarcere a devenit un subiect important mai ales după criza fi nanciară din 2007, mai din cauza efectelor acesteia precum creșterea prețurilor sau pierderea locurilor de muncă. În timp ce pentru emigrație s-a demonstrat că este determinată de condițiile mai bune de trai din țările gazdă (astfel că factorii bunăstării la nivel macroeconomic sunt principalii factori push), migrația de revenire necesită informații și la nivel microeconomic, deoarece reprezintă o decizie a individului în funcție de contextul socio-economic. Mulți autori plasează debutul crizei economice la sfârșitul anului 2008 rata șomajului a ajuns la niveluri neprevăzute (Hurd și Rohwedder, 2010) (Ötker-Robe și Podpiera, 2013).

Romanian Statistical Review - Supplement nr. 5 / 201520

În Romania studiile cu privire la migrația de revenire sunt doar la nivel incipent în principal din cauza lipsei datelor consistente cu privire la această temă. În acest context articolul de față expluateză baza de date a Institutului din Spania din 2007 - “Encuesta Nacional de Inmigrantes”, pentru a determina intențiile de revenire a emigranților români în anul 2007, înainte de criza fi nanciară. Articolul începe cu o descriere succintă a literaturii de specialitate cu privire la subiectul migrației de revenire și este structurat după cum urmează: mai întâi am precizat metodologia modelelor econometrice care au ca variabila dependentă binară, utilizate în analiza intenției migrației de revenire, urmată de specifi carea variabilelor utilizate în analiză folosind chestionarul “Encuesta Nacional de Inmigrantes - 2007”( ENI - 2007). În fi nal, am construit două modele econometrice Probit pentru determinare motivelor mgirației de întoarcere în privința migranților români din Spania. Articolul plasează analiza înaintea crizei fi nanciare și oferă imagine de ansamblu a întențiilor pre-criză, de altfel, trebuie luat în calcul acest aspect mai ales că din analiza descriptivă se observă că cei care doresc să revină au o pondere semifi cativ mai mica decât a celor care doresc să rămână.

Migrația de revenire. Contextul internațional și național

Literatura în domeniul migrației este foarte bogată, multe dintre studii se concentrează asupra determinaților migrației, aspectele și repercusiunile la nivel macroeconomic și microeconomic a țărilor care trimit și primesc migranți deopotrivă. Migrația de revenire, totuși, nu a fost o problemă intens dezbătută decât după ce criza fi nanciară a început. Date fi ind principalele teorii ale migrației cel care se întoarce poate fi un migrant care a eșuat în scopurile sale de a migra dar este puternic legat de țara de origine, chiar și așa unii dintre ei nu aleg să se întoarcă permanent (Cassarino, 2004). Migrația de revenire este importantă din perspectiva ambelor țări: atât cele care primesc, dar și cele care trimit migrant. Principalul motiv care determină revenirea îl reprezintă eșecul economic al migrantului, primele constatări arată că migrantul care este incapabil să găsească o slujbă potrivită este mult mai probabil să se întoarcă (DaVanzo, 1980). Totodată, migranții pot fi legați de tărâmurile natale, iar decizia de a se întoarce către țara natală în cazul celor din Noua Zeelandă este bazată pe atașamentul puternic fașă de familie, prieteni și locuri vechi și familiare (Gilson și Lidgard, 2002). Actualul context socio-economic a fost afectat de criza fi nanciară care a început în 2007 având un impact puternic asupra țărilor dezvoltate, fapt care poate determina migrația de revenire (Herm, 2008). In Ungaria jumatate dintre

Revista Română de Statistică - Supliment nr. 5 / 2015 21

migranții caer au revenit in perioda 2008 până în 2010 avaea vârste cuprinse între 30 și 45 ani și numai 20% dintre cei de peste 45 de ani s-au întors. Același trend este observant și în Romania pentru românii care s-au întors din Spania, numui 15% dintre cei de peste 45 de ani doresc să se întoarcă (Iglicka et al, 2012). Așa cum Dustmann (et al., 2007) a precizat, migrația ia diverse forme în funcție de motivele pentru care oamenii aleg să migreze. Folosind date ale sondajului britanic cu privire la migrația forței de muncă (”British labour Force Survey Migration”) a arătat că decizia de revenire este cauzată de raportul benefi ciu-cost, pe măsură ce oamenii care aleg să migreze și se decid asupra unei migrații permanente au benefi cii mai ridicate decât costurile migrației, pe de altă parte decizia de a reveni poate apărea în cazul în care costurile exced benefi ciile , generând migrația de revenire. De asemenea, au demonstrate că migrația de revenire este mult mai evidentă pentru imigranții din Uniunea Europeană, America și Australia în comparație cu imigranții din India Sub-Continentală și Africa, iar comparând migranții de rasă caucaziană cu cei care nu sunt din această rasă rezultatele arată că cei care sunt de origine cauzaziană au tendința de a reveni. Analizând datele sondajul “Encuesta Nacional de Inmigrantes - 2007” Ramos și Manatano (2013) au determinat dacă volumul remitențelor crește urmărind diverse varibile, în privința variabilei de control cu referire la planurile în următorii 5 ani ale persoanelor intervievate, astfel, există un effect pozitiv asupra deciziei de revenire în țara de origine, însă niciun effect semnifi cativ în privința mutării către o altă țară. Studii recente cu referire la migrația de întoarcere au folosit ca sondaj de referință “Encuesta Nacional de Inmigrantes - 2007”, Sandu (et. al., 2009) a efectuat un studiu în anul 2008 pentru a determina dacă față de anul 2007 opinia migranților români din Spania cu privire la revenire s-a modifi cat. Rezultatele arată că românii deveniseră mai îngrijorați de efectele crizei economice, în special de pierderea locului de muncă, totodată aproximativ jumătate din românii din Madrid intervievați declarau că aveau de gând să se întoarcă în România. Vlase (2011) arată într-un studiu făcut asupra membrilor comunității comunei Vulturu plecați în Italia că doresc să se întoarcă dacă aceștia trimit bani acasă. În cazul migranților români s-a demonstrat într-un studiu efectuat asupra persoanelor care lucrează în domeniul medical că sexul și vârsta persoanelor nu sunt caracteristici care să îi facă să revină, modelul regresiei logistice a arătat că variabila cu referire la numărul de copii al migranților este semnifi cativă, iar probabilitatea de a se întoarce creștea dacă migrantul avea cel puțin un copil. Totodată, dacă numărul de ani petrecuți în afară creștea

Romanian Statistical Review - Supplement nr. 5 / 201522

probabilitatea de a reveni creștea. Deasemenea, cei care remit intenționează să revină, iar venit are un impact negativ asupra intenției de revenire, întrucât, cu cât venitul migrantului este mai ridicat cu atât acesta este mai puțin dornic de a se întoarce în țară (Roman și Zizi, 2012) (Roman și Zizi, 2014).

Metodologia cercetării

Modele econometrice avansate cele mai utilizate în analiza de chestionar sunt modelele a căror variabilă dependent ia valori discrete. În funcție de tipul variabilei putem distinge urmatoarele două tipuri de modele econometrice (Andrei și Bourbonnais, 2008): • Modele cu variabila dependentă binară (în general valori acceptate

pentru această variabilă sunt 0 și 1). Aceste modele estimează probabilitatea pi este egală cu 1. Cele mai utilizate modele binare sunt Logit, Probit și regresia logistică.

• Modele cu răspunsuri multiple sunt modele a căror variabilă dependentă are mai mult de două variante de răspuns. În acest caz variabila dependentă poate fi nominală sau ordinală.

Un model econometric cu variabila dependentă de tip binar, Logit, a fost utilizat în analiza intenției de revenire a Românilor migranți care au studii superioare, asupra unei baze de date colectate cu ajutorul unui sondaj on-line, rezultatele arată că o dată cu înaintarea în vârstă intenția de revenire scade. Totodată, dacă aceștia au un serviciu stabil în țara gazdă afectează negative intențiile de revenire în țara de origine. Pe de altă parte, situații precum identitatea națională, faptul că sunt mândrii că sunt români, dar și faptul că au o rudă acasă (soț / soție / copil) în țara de orgine determină intenția de revenire (Predosanu et al., 2007). Modele Probit sunt și acestea utilizate în studiul intenției de revenire. Soon (2010) a studiat intenția de a reveni în țara de origine a studenților străini din Noua Zeelandă și a demonstrate că percepția asupra felului în care aceștia își pot folosi în țara lor de origine aptitudinile dobândite le afectează semnifi cativ intenția de a reveni, de asemenea, cu privire la perioada pe care au petrecut-o în Noua Zeelandă, studenții doresc să râmână pe măsură ce această perioadă crește. Modele binare sunt modele pentru variabile dependente dihotomice, forma generală a modelelor Probit și Logit este reprezentată după cum urmează:

(1)

Revista Română de Statistică - Supliment nr. 5 / 2015 23

Singura diferență dintre cele două modele este cu privire la distribuția termenului eroare. Distribuția termenului eroare a modelului Logit este reprezentat de o distribuție logistică după cum urmează:

(2)

Distribuția termenului eroare a modelului Probit model este o distribuție normală spre deosebire de distribuția logistică a modelului Logit (Pecican, 2009). În această situație probabilitatea ca pi = P (yi = 1) este defi nite de următoarea ecuație (Andrei și Bourbonnais, 2008):

(3), Unde:

Cu:

Atunci când se estimează parametrii unui model cu variabilă binară de tipul Probit sau Logit, totodată se estimează și efectele marginale ale acestora. Efectele marginale arată cu cât se modifi că probabilitatea variabile dependente atunci când y=1 dacă variabilele independente se modifi că cu o unitate(Greene, 1996). În analiză am folosit modelul Probit, deoarece în literatura de specialitate nu se recomandă un anumit model, iar pentru rezultatele analizate nu există diferențe semnifi cative între rezultaltele celor două modele.

Date și variabile

Pentru a analiza situația generală a emigranților Români în Spania, am folosit baza de date a unui chestionar efectuat asupra imigranților din Spania furnizată de către Institutul de Statistică al Spaniei în 2007 - “Encuesta Nacional de Inmigrantes”(ENI). ENI a fost desfășurat în perioada noiembrie 2006 și februarie 2007 și oferă informații cu privire la aspect soci-demografi ce precum statusul marital, naționalitate, țara unde s-a născut, educație, dar și informații cu privire la planurile în următorii 5 ani, venit, ani petrecuți în Spania, sau dacă sunt sau nu angajați.

Romanian Statistical Review - Supplement nr. 5 / 201524

Variabila dependent utilizată în model cu referire la intenția de revenire a respondenților a fost codifi cată după întrebarea ”Care sunt planurile dumneavoastra în următorii 5 ani?”: 1. Nu știu 2. Mă întorc în țara de origine 3. Rămân în Spania 4. Mă gândesc la o altă țară Analizând răspunsurile cu privire la planurile în următorii 5 ani observăm că o parte mică din respondenți 8,28% au declarat că doresc să revină în România. Variabila dependentă a fost recodifi cată după întrebarea care sunt planurile dumneavoastră în următorii 5 ani astfel: - Mai întâi am renunțat la variantele de răspuns ”nu știu” și ”consider

o altă țară” întrucât numărul de respondenți era foarte mic; - Apoi am codifi cat întrebarea astfel: 1 = Da, doresc să revin în

România și 0 = Rămân în Spania. Pentru a obține baza de date fi nală am fi ltrat baza de date după țara în care s-au născut, dar și după naționalitate, astfel încât baza de date să includă numai români. Totodată, din baza de date am eliminat și răspunsurile nefi rești, deoarece unii dintre respondenți au declarat că nu au vârsta de muncă deși aveau peste 30 de ani. De asemenea, am exclus persoanele care aveau vârsta sub 18 ani și peste 65 ani pentru a obține o bază de date care are populația în vârstă de muncă, astfel componența bazei de date fi nale este formată din 955 de observații însă dintre aceștia 946 de persoane au răspuns la întrebarea ”ce planuri aveți în următorii 5 ani”; repartizarea pe variante de răspuns este prezentată mai jos:

“Care sunt planurile în următorii 5 ani”: Frecvența- Mă întorc în țara de origine- Rămân în Spania

85393

Total 946

Analiza noastră a cuprins variabile socio-demografi ce, dar și variabile care țin de alte aspecte precum nivelul de vorbire al limbii spaniole introdus în analiză ca variabilă dummy în funcție de cel mai mic nivel al cunoașterii limbii spaniole (1 fi ind cel mai mic nivel - nu stie spaniola bine, iar 4 cel mai înalt nivel - știe spaniola foarte bine); sexul persoanelor variabilă de tip dihotomic 1 reprezentând sexul feminine și 0 sexul masculin; starea civilă dacă este căsătorit(1) sau nu(0); dacă are studii de orice fel(codifi cată cu 1 pentru da are studii și 0 pentru nu are studii); dacă are părinții în țara de origine, respectiv în România; variabila continuă numărul de persoane cu care locuiește în Spania; dacă are sau nu serviciu la momentul intervievării; dacă remite către țara de

Revista Română de Statistică - Supliment nr. 5 / 2015 25

origine; și anii petrecuți în Spania, care refl ect experința ca migrant, unde am pus restrictive maximum 10 ani întrucât până la acest număr de ani erau cei mai mulți dintre migranți.

Rezultate și comentarii

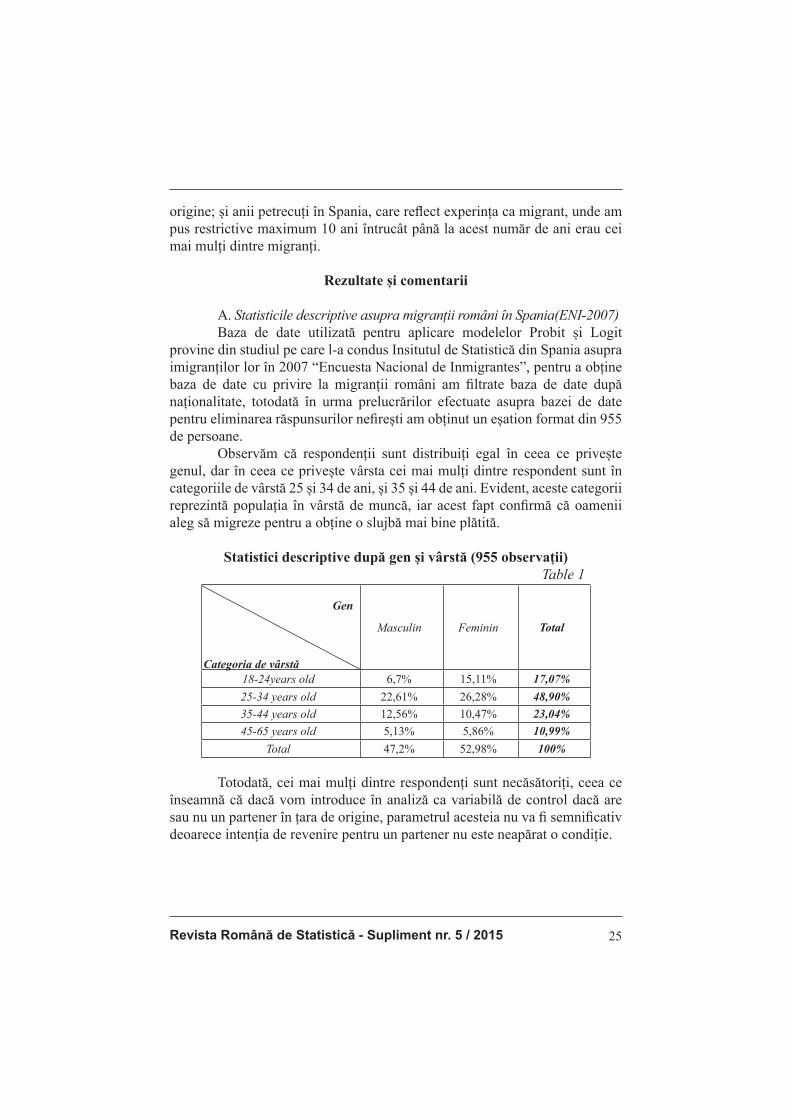

A. Statisticile descriptive asupra migranții români în Spania(ENI-2007) Baza de date utilizată pentru aplicare modelelor Probit și Logit provine din studiul pe care l-a condus Insitutul de Statistică din Spania asupra imigranților lor în 2007 “Encuesta Nacional de Inmigrantes”, pentru a obține baza de date cu privire la migranții români am fi ltrate baza de date după naționalitate, totodată în urma prelucrărilor efectuate asupra bazei de date pentru eliminarea răspunsurilor nefi rești am obținut un eșation format din 955 de persoane. Observăm că respondenții sunt distribuiți egal în ceea ce privește genul, dar în ceea ce privește vârsta cei mai mulți dintre respondent sunt în categoriile de vârstă 25 și 34 de ani, și 35 și 44 de ani. Evident, aceste categorii reprezintă populația în vârstă de muncă, iar acest fapt confi rmă că oamenii aleg să migreze pentru a obține o slujbă mai bine plătită.

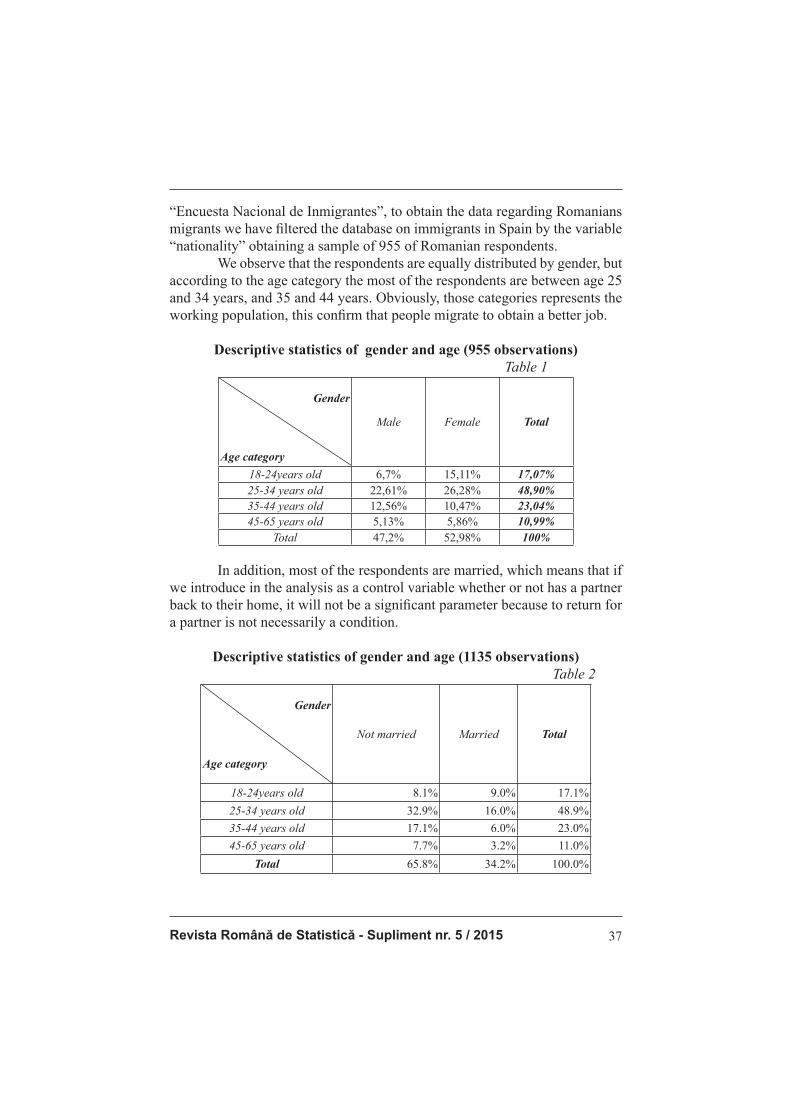

Statistici descriptive după gen și vârstă (955 observații) Table 1

Gen

Categoria de vârstă

Masculin Feminin Total

18-24years old 6,7% 15,11% 17,07%25-34 years old 22,61% 26,28% 48,90%35-44 years old 12,56% 10,47% 23,04%45-65 years old 5,13% 5,86% 10,99%

Total 47,2% 52,98% 100%

Totodată, cei mai mulți dintre respondenți sunt necăsătoriți, ceea ce înseamnă că dacă vom introduce în analiză ca variabilă de control dacă are sau nu un partener în țara de origine, parametrul acesteia nu va fi semnifi cativ deoarece intenția de revenire pentru un partener nu este neapărat o condiție.

Romanian Statistical Review - Supplement nr. 5 / 201526

Statistici descriptive după status marital și vîrstă(955 observații) Tabel 2

Gen

Categoria de vârstă

Necăsătorit Căsătorit Total

18-24years old 8.1% 9.0% 17.1%25-34 years old 32.9% 16.0% 48.9%35-44 years old 17.1% 6.0% 23.0%45-65 years old 7.7% 3.2% 11.0%

Total 65.8% 34.2% 100.0%

B. Analiza rezultatelor modelului Probit Pentru a analiza intenția de revenire am construit duă modele Probit: unul pentru categoria de vârstă 18 – 65 de ani care reprezinta populația în vârstă de muncă, și cel de-al doilea pentru categoria de vârstă 19-50 de ani întrucât în acestă categorie există proporția cea mai mare de migranți români care doresc să revină 10,16%. Având în vedere aceste rezultate, trebuie să luâm în considerare faptul că anul în care a fost culeasă baza de date este 2007, când cei mai mulți nu doreau să revină, în principal datorită boomul economic și faptului că efectel crizei fi nanciare încă nu erau resimțite. Analizând rezultatele observăm că variabilele socio-demografi ce precum sexul și starea civilă a persoanelor intervievate nu au efect asupra deciziei de revenire, deși pentru variabila cu referire la genul persoanei era egal distribuită. De asemenea, am introdus în model și variabile de control cu privire la dacă are părinții în România, dacă are orice fel de studii, fi e acestea la nivel minim sau superior, și dacă a dobândit o locuință în Spania, niciuna dintre aceste variabile neavând un efect semnifi cativ asupra intenției de revenire a respondenților. Nesemnifi cativitatea coefi cienților modelului se datorează în mod special ponderii mici a persoanelor care au declarat că doresc să revină. Totodată analizând intenția de revenire din perspectiva persoanelor care au nivel mai ridicat al cunoștintelor limbii spaniole față de cele care au nivel slab de cunoștințe se observă că persoanele care cunosc foarte bine limba spaniolă nu au intenția să revină în România, lucru care era de așteptat având în vedere că acestea au depășit foarte ușor barajul lingvistic.

Revista Română de Statistică - Supliment nr. 5 / 2015 27

Probit for age between 18-65 years oldTabel 3

Model Probit Model Probit II Efecte marginale p>|z|Constant -1,949 -1,700 - -VbSpan2 -0,213 - - -VbSpan3 -0,077 - - -VbSpan4 -0,413(*) -0,356(*) -0,056 0,012Remite 0,347(*) 0,343(*) 0,054 0,010Are serviciu -0,223(*) -0,254(*) -0,039 0,035Anii în Spania 0,364(*) 0,288(*) 0,045 0,019Locuință în Spania -0,209 - - -Sex 0,131 - - -Stare civilă 0,914 - - -Părinți în România -0,381 - - -Are studii 0,009 - - -Număr persoane 0,001 - - -Log likehood -265,234 -266,46Pseudo R2 0,038 0,0342LR chi2 21,35(*) 18,89(*)Numărul de observații 890 (*) semnifi cativ la 5%

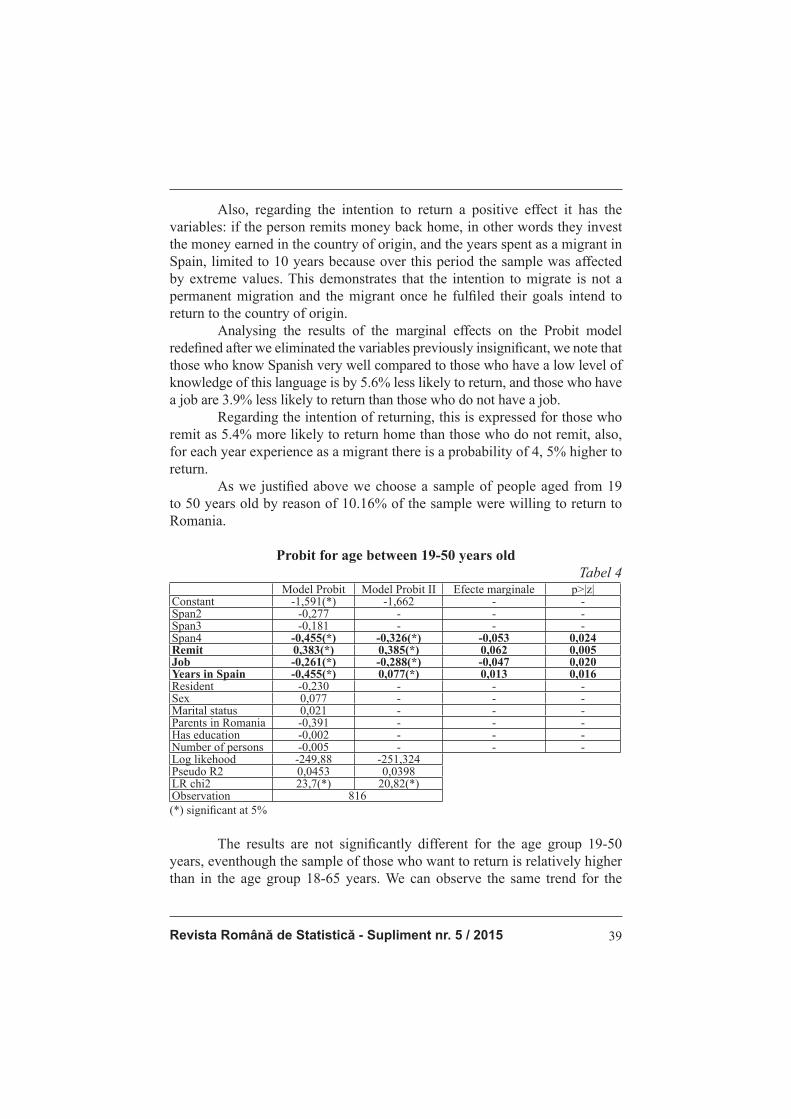

De asemenea, în privința intenției de revenire un efect pozitiv îl au variabilele cu privire la dacă persoana remite bani acasă, cu alte cuvinte investește banii câștigați și în țara de origine, și vechimea ca migrant în Spania, limitată la 10 ani deoarece peste această perioadă eșantionul era afectat de valori extreme. Acest lucru demonstrează că intenția de migra nu este una permanentă, iar migrantul o dată ce și-a îndeplinit scopul are intenția de reveni în țara de origine. Analizând rezultatele efectelor marginale asupra modelului Probit redefi nt după ce am eliminate variabilele nesemnifi cative din modelul Probit anterior, observăm că cei care cunosc foarte bine spaniola față de cei care au un nivel scăzut de cunoștințe al acestei limbi sunt cu 5,6% mai puțin probabil să revină, iar cei care au un serviciu sunt cu 3,9% mai puțin probabil să revină față de cei care nu au un serviciu. În privința intenției de revenire, aceasta se manifestă in cazul celor care remit fi ind cu 5,4% mai probabil să revină în țară față de cei care nu remit, de asemenea pentru fi ecare an care se adaugă experienței de migrant există o probabilitatea cu 4,5% mai mare de revenire. Așa cum am justifi cat anterior, am ales ca eșantion pentru cel de-al doilea model persoanele din categoria de vârstă 19-50 de ani deoarece aceștia aveau cea mai mare pondere a persoanelor care doresc să revină din totalul eșantionului, 10,16% declarau că doresc să revină.

Romanian Statistical Review - Supplement nr. 5 / 201528

Probit for age between 19-50 years oldTabel 4

Model Probit Model Probit II Efecte marginale p>|z|Constant -1,591(*) -1,662 - -VbSpan2 -0,277 - - -VbSpan3 -0,181 - - -VbSpan4 -0,455(*) -0,326(*) -0,053 0,024Remite 0,383(*) 0,385(*) 0,062 0,005Are serviciu -0,261(*) -0,288(*) -0,047 0,020Anii în Spania -0,455(*) 0,077(*) 0,013 0,016Locuință în Spania -0,230 - - -Sex 0,077 - - -Stare civilă 0,021 - - -Părinți în România -0,391 - - -Are studii -0,002 - - -Număr persoane -0,005 - - -Log likehood -249,88 -251,324Pseudo R2 0,0453 0,0398LR chi2 23,7(*) 20,82(*)Numărul de observații 816(*) semnifi cativ la 5%

Rezultatele nu sunt semnifi cativ diferite nici în cazul grupei de vârstă 19-50 de ani, chiar dacă eșantionul celor care doresc să revină este relativ mai mare decât în cazul grupei de vârstă 18-65 de ani. Observându-se aceiași tendință pentru persoanele care doresc să revină în România, aceștia având o vechime sufi cientă în Spania și totodată trimițând bani acasă, cel mai probabil în vederea investițiilor.

Concluzii

În Romania studiile cu privire la migrația de revenire sunt la început în mod special din cauza lipsei datelor consistente cu privire la această temă. Pentru a analiza situația generală a emigranților Români în Spania înainte de criza fi nanciară, am folosit baza de date a unui chestionar efectuat asupra imigranților din Spania furnizată de către Institutul de Statistică al Spaniei în 2007 - “Encuesta Nacional de Inmigrantes”(ENI). ENI a fost desfășurat în perioada noiembrie 2006 și februarie 2007 și oferă informații cu privire la aspect soci-demografi ce precum statusul marital, naționalitate, țara unde s-a născut, educație, dar și informații cu privire la planurile în următorii 5 ani, venit, ani petrecuți în Spania, sau dacă sunt sau nu angajați. Analizând rezultatele observăm că variabilele socio-demografi ce precum sexul și starea civilă a persoanelor intervievate nu au efect asupra deciziei de revenire, deși pentru variabila cu referire la genul persoanei era egal distribuită. De asemenea, am introdus în model și variabile de control cu privire la faptul dacă are părinții în România, dacă are orice fel de studii, fi e

Revista Română de Statistică - Supliment nr. 5 / 2015 29

acestea la nivel minim sau superior, și dacă a dobândit o locuință în Spania, niciuna dintre aceste variabile neavând un efect semnifi cativ asupra intenției de revenire a respondenților. Nesemnifi cativitatea coefi cienților modelului se datorează în mod special ponderii mici a persoanelor care au declarat că doresc să revină. Totodată analizând intenția de revenire din perspectiva persoanelor care au nivel mai ridicat al cunoștintelor limbii spaniole față de cele care au nivel slab de cunoștințe se observă că persoanele care cunosc foarte bine limba spaniolă nu au intenția să revină în România, lucru care era de așteptat având în vedere că acestea au depășit foarte ușor barajul lingvistic. Rezultatele nu sunt semnifi cativ diferite nici în cazul grupei de vârstă 19-50 de ani, chiar eșationul celor care doresc să revină este relativ mai mare decât în cazul grupei de vârstă 18-65 de ani. Intenția de revenire este un subiect de actualitate mai ales privind efectele crizei economice în țările dezvoltate. În România migrația este încă un subiect la început de drum, în mod special migrația de revenire, pentru care trebuie constituite baze de date de natură să surprindă efectele migrației și schimbârilor economice de-a lungul timpului.

Acknowledgment „Această lucrare a fost cofi nanţată din Fondul Social European, prin Programul Operaţional Sectorial Dezvoltarea Resurselor Umane 2007-2013, proiect numărul POSDRU/159/1.5/S/138907„Excelenţă în Cercetarea Ştiinţifi că, Interdisciplinară, Doctorală şi Postdoctorală, în Domeniile Economic, Social şi Medical - EXCELIS”, coordonator Academia de Studii Economice din Bucureşti”

Referințe

- Andrei, T., Bourbonnais, R., 2008. Econometrie. Ed Economică, Bucharest, pp. - Cassarino, Jean-Pierre, “Theorising Return Migration: The Conceptual Approach to

Return Migrants Revisited.” International Journal on Multicultural Societies, 6, no. 2 (2004), UNESCO, Paris, p. 253-279 available on: http://unesdoc.unesco.org/images/0013/001385/138592E.pdf#page=60

- Dustmann, C.; Weiss, Y. (2007): “Return Migration: Theory and Empirical Evidence from UK”, British Journal of Industrial Relations, vol. 45, n. 2, pp.236-256.

- Greene, William H., Marginal Effects in the Bivariate Probit Model (June 1996). NYU Working Paper No. EC-96-11. Available at SSRN: http://ssrn.com/abstract=1293106

- Herm, A, Recent migration trends: citizens of EU-27 Member States become ever more mobile while EU remains attractive to non-EU citizens (Eurostat, 2008).

- Hurd, M. D., Rohwedder, S.,”Effects of the Financial Crisis and Great Recession on American Households” NBER Working Paper No. 16407 September 2010 JEL No. D12,D31,D84,D91,J64 available on: http://www.nber.org/papers/w16407.pdf

Romanian Statistical Review - Supplement nr. 5 / 201530

- Iglicka (scientifi c advisor), Barcevičius, Repečkaitė, Žvalionytė Labour mobility within the EU: The impact of return migration, Public Policy and Management Institute (PPMI), (Lithuania, 2012)

- Lidgard, J., Gilson, C., ”Population Association of New Zealand Return Migration of New Zealanders: Shuttle and Circular Migrants” New Zealand Population Review 28(1), 99-128. 2002 available on: http://www.waikato.ac.nz/__data/assets/pdf_fi le/0010/76555/nzpr02-28-lidgard.pdf

- Sandu Dumitru, coordonator, ”Comunități românești în Spania”, Fundația Soros, Februarie 2009.

- Pecican, E. Ş., Econometrie pentru .. economiști. , Ed. Economică, (Bucharest, 2007).

- Predosanu, Zamfi r, Militaru, Mocanu, Vasile ”Econometric modeling of return migration intention”(2007) Available on: http://www.wseas.us/e-library/conferences/2011/Corfu/ASM/ASM-34.pdf

- Raúl Ramos, Alessia Matano, Remittances, education and return migration. Evidence for immigrants in Spain, WP3/11 SEARCH WORKING PAPERApril 2013. Available on: http://www.ub.edu/searchproject/wp-content/uploads/2013/05/WP_3.11.pdf

- Roman, M, Zizi, G, Return migration in an economic crisis context. A survey on Romanian healthcare professionals, Tome 39, Issue 2(48), Romanian Journal of Economics, 2014, p. 100-120

- Roman, M, Zizi, G, Romanian Immigrants Worldwide: What makes them Return Home? Journal of Identity and Migration Studies Volume 6, number 2, 2012 p.2-17

- Soon, A., ”Change of Heart? A bivariate Probit Model of International Students’ Change of Return Intention International Journal of Business and Economics”, 2010, Vol 9, No.2, pg115-129

- Ötker-Robe, I, Podpiera, A. M., ”The Social Impact of Financial Crises Evidence from the Global Financial Crisis” The World Bank Development Economics Offi ce of the Senior Vice President and Chief Economist November 2013 available on: http://www-wds.worldbank.org/external/default/WDSContentServer/IW3P/IB/2013/11/14/000158349_20131114113429/Rendered/PDF/WPS6703.pdf

- Vlase, I., ”Migrația de întoarcere a românilor din Italia. Studiu de caz în Vulturu, Vrancea” CALITATEA VIEŢII, XXII, nr. 2, 2011, p. 155–176

Revista Română de Statistică - Supliment nr. 5 / 2015 31

AN INVESTIGATION OF ROMANIANS’ RETURN INTENTIONS FROM SPAIN

Elena-Maria PRADA Bucharest Academy of Economic Studies

Abstract Migration is the phenomenon that has always been along humans, people searching for better places to live. Reasons of migration have been evolved along the greatest discoveries of man. Nowadays, the concept of migration is just different in terms of the factors which determinate it, but the basic reason of migration is welfare. We employed a Probit model to estimate which factors are determining Romanians to return from Spain using the Spanish Survey ”Encuesta Nacional de Inmigrantes” 2007. Our results showed that before the fi nancial crisis began the intentions to return were so noticeable, although if the person remits to the home country or has a suffi cient experience in Spain also they express their intentions to return, this confi rms the fact that migration was a temporary one and as the purpose of migration was fulfi lled the migrant intends to return. Keywords: returnee, migration, probit, logit, Romania. JEL Classifi cation codes: C01,C30, O15

Introduction

Migration is the phenomenon that has always been along the human being, people searching for better places to live. Reasons of migration have been evolved along the greatest discoveries of the human being. Nowadays, the concept of migration is just different in terms of the factors which determinate it, but the basic reason of migration is welfare. Return migration has been an important topic to discuss after the fi nancial crisis, mainly because the effects of the crisis as rising prices or loss of the job. While for emigration is shown that is driven by better conditions in the host countries (as the macroeconomic welfare factors are the main push factors), return migration requires information also at micro-level, as it is a decision of the individual depending of the socio-economical context. Many authors places the debut of fi nancial crisis at the end of 2007 when the house and stock prices began to decline and by the end of 2008 the unemployment rate raised to unpredictable levels (Hurd and Rohwedder, 2010) (Ötker-Robe and Podpiera, 2013).

Romanian Statistical Review - Supplement nr. 5 / 201532

In Romania the studies regarding return migrations are just scratching the surface of this topic mainly due to the lack of consistent data. In this context the paper explores the survey from Spain in 2007 - “Encuesta Nacional de Inmigrantes”, to determinate the return migration intentions of Romanian emigrants. We began by providing the literature review related to return migration topic. The paper is structured as it follows: fi rst we followed the research methodology by providing the usage of binary models in analysing the return intention, secondly we describe the variables employed in the analyse of return intentions based on the data provided by “Encuesta Nacional de Inmigrantes - 2007”( ENI - 2007). And last we concluded the results based on the marginal effect of the Probit models. Finally, we built two Probit models to determine the return migration intentions regarding Romanian migrants in Spain. The article analysis the return intentions of the Romanian migrants in Spain before fi nancial crisis and provides an overview of the return intentions, moreover, we must take into consideration that the survey was collected before fi nancial crisis also noticeable from the small sample of the those who intended to return.

Literature review

The literature on migration is very rich, many studies have been made regarding the determinants of migration, the aspects and the repercussions on the macro economical and micro economical levels of both sending and receiving countries. Return migration though has not been an issue to debate until the fi nancial crisis began. Given the main theories of migration the returnee may be a failure migrant that has not accomplished its goals or the migrant that has successfully fulfi lled their goals but is strongly linked to their home country, even though some of them are not returning permanently (Cassarino, 2004). Return migration is important from the perspective of both countries: the sending countries and the receiving countries. The main reason of returning is the economic failure of the migrant, early fi ndings show that if a migrant is unable to fi nd a reasonable job is more likely to return (DaVanzo, 1980). Also, migrants may be bound to their homeland, the decision of returning to their home in case of the New Zeelanders is based on their strong attachment to family, friends and old places (Gilson and Lidgard, 2002). The actual socio-economic context has been affected by the fi nancial recession started in 2007 and has an impact on developed countries and this fact could determine the return migration. According to the studies provided

Revista Română de Statistică - Supliment nr. 5 / 2015 33

by Eurostat in the EU Member States, the median age of those who return to their home country was over 30 years in 2008 (Herm, 2008). In Hungary half of the migrants returned in 2008 until 2010 were aged between 30 and 45 years and only 20% of those over 45 have returned. The same trend is observed in Romania for the Romanians returning from Spain, only 15% of those aged over 45 years are coming back to their homes (Iglicka et al, 2012). As Dustmann (et al., 2007) stated, migration takes different forms regarding the reasons of migration, return migration is a form of temporary migration due to economic motives. Using data from British labour Force Survey Migration showed that the returning decision is a cause of benefi t-cost ratio, as people choose to migrate and decide a permanent migration if the benefi t is higher than the cost of migration, on the other side the decision of returning may occur if the costs exceed the benefi ts, generating return migration. Also, they showed that the return migration is more highlighted for the EU, America’s and Australia’s migrants compared with the immigrants from Indian Sub-Continent and Africa, and comparing white migrants with non-white migrants the results show that white migrants tend to return. Newer studies referred to Romanian migrants have used the “Encuesta Nacional de Inmigrantes - 2007”, Sandu (et. al., 2009) has conducted a survey in 2008 to establish if there are any differences from year 2007 regarding the return intentions of Romanian migrants in Spain. The results showed that Romanian were concerned about their jobs and stability, due to the consequences of fi nancial crisis, and almost half from Romanian in Madrid declared that they intend to return. Vlase (2011) showed that Romanians, community based Vulturu, intend to return from Italy if they remit to their homes. In case of Romanian migrants has been proven regarding the medical staff that the gender and the age are no feature that will make them return, logistic regression results showed that the number of children has statistical signifi cance, and as the migrants has at least one child the return intention increase. Also, if the experience as a migrant increases, the return intention increases towards. As well, if the migrants remit to their home country they intend to return, and the wages of the migrant have a negative impact on return intention, as the income increases the return intention decreases (Roman and Zizi, 2012) (Roman and Zizi, 2014).

Research methodology

Advanced econometric models most common on the analysis of opinion surveys are those models in which the dependent variable takes discrete values.

Romanian Statistical Review - Supplement nr. 5 / 201534

Depending on the type of the independent variable we can distinguish the following two types of discrete choice model (Andrei and Bourbonnais, 2008): the binary models, the dependent variable is binary (generally

accepted values that we take with this variable are 0 and 1). These models estimate the probability pi attempting characteristic binary value equal to 1. The most popular models for binary variables are probably Logit, Probit and logistic regression model.

models with multiple responses are those models in which the dependent variable has more than two discrete variables. In this case, the dependent variable can be nominal or ordinal type.

An econometric model using a binary Logit model intend to analyse the return to Romania of Romanian migrants with higher education, using the data collected by an on-line survey, shows that along with the increasing of the age the intention to return reduces. Also, having a job in the host country negatively affects the plans of returning to the origin country. On the other hand, situations such as national identity, that of being proud that he is Romanian, but the existence of a relative (husband / wife / child) in the country determine the return to their home country (Predosanu et al., 2007). Probit models are also used to analyse the return intention. Soon (2010) studied the return intention of foreign student in New Zeeland and showed that the perception of how the student can apply the skill in their home country can affect the return intention, also, in terms of the period stayed in New Zeeland, showed that the longer they stay the less they want to return to their origin country. The binary models are models for dichotomous dependent variables, the general form of Probit and Logit models are represented by the following equation: (1)

The only differences between those two models are regarding the error distribution. The Logit model error has a logistic distribution and is defi ned through the following equation:

(2)

The Probit model error distribution is a normal distribution, unlike standard Logit model whose partition function is the logistic type (Pecican, 2009). Under these conditions defi ne the probability pi = P (yi = 1) through the following equation (Andrei and Bourbonnais, 2008):

Revista Română de Statistică - Supliment nr. 5 / 2015 35

(3),

Where:

With:

otherwise

When the coeffi cients of a binary model, as Probit or Logit, are estimated, it also estimate the marginal effects of those. The marginal effects show how the probability of y=1 modifi es if the independent variabiles modify with one unit(Greene, 1996). In our analysis we have used the Probit model as in the literature there is no recomandation for a specifi c model to use, and as for the the results there is no signifi cant difference between Probit and Logit models.

Data and variables