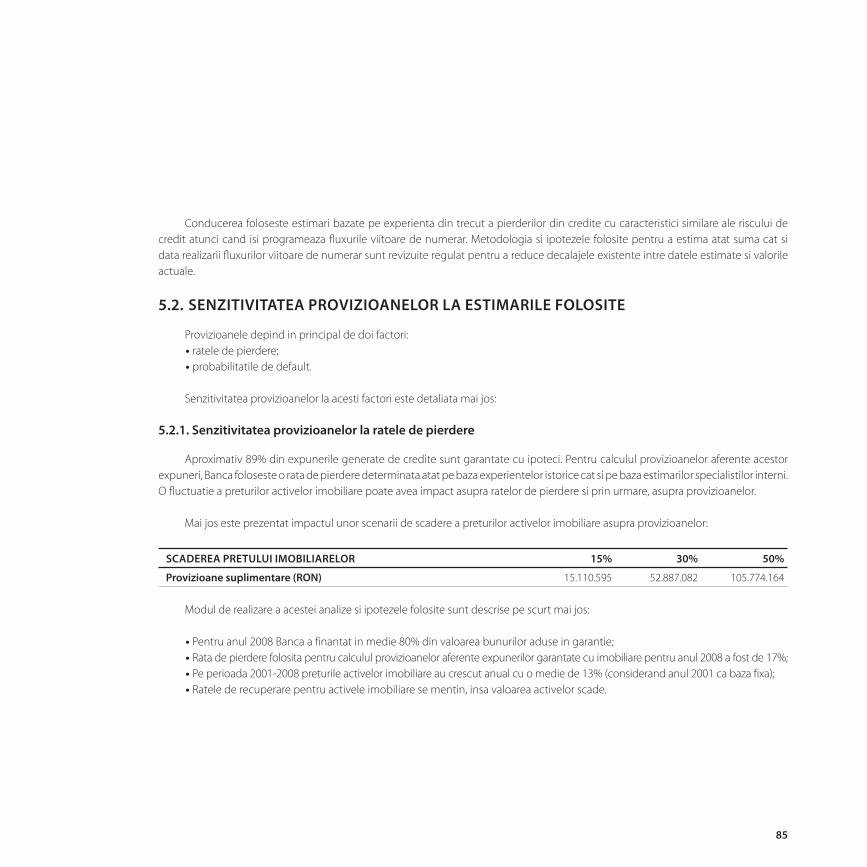

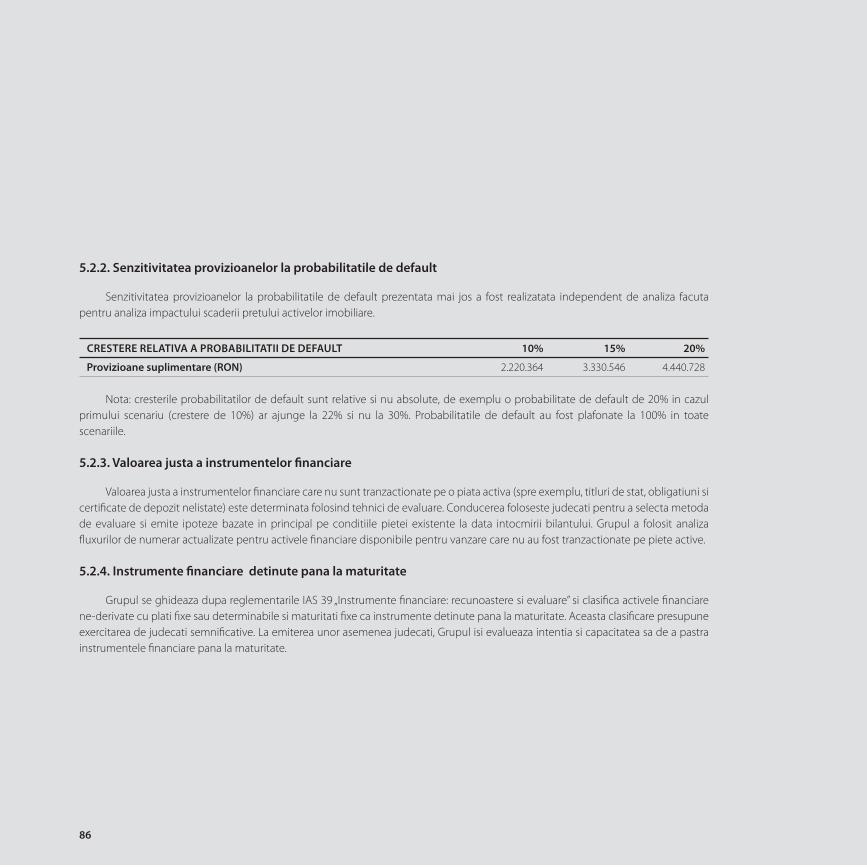

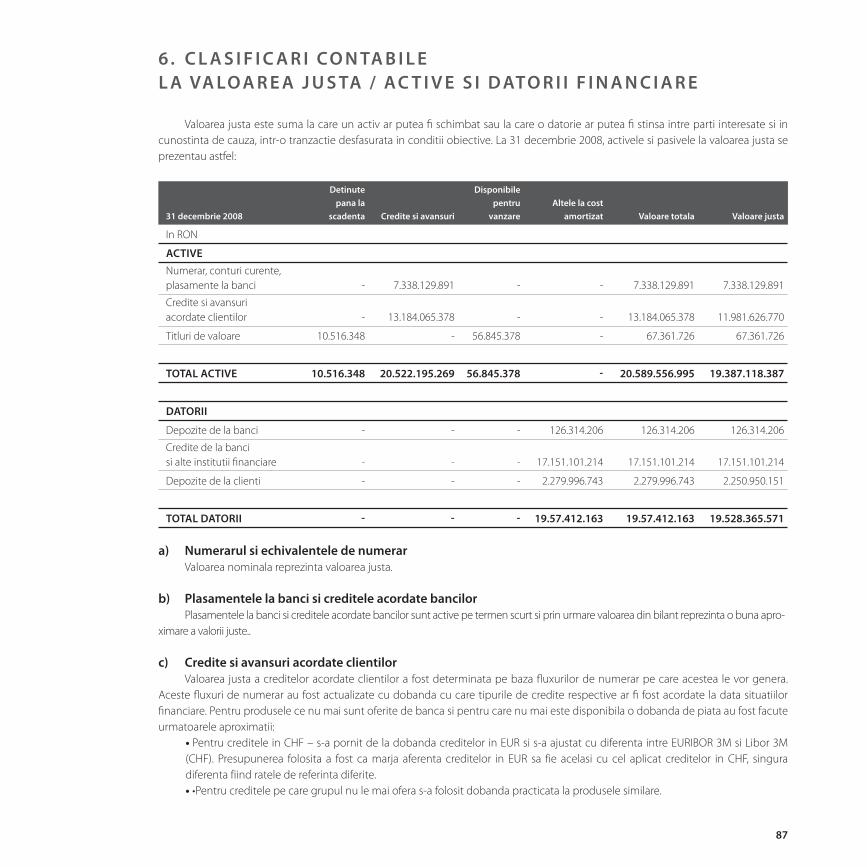

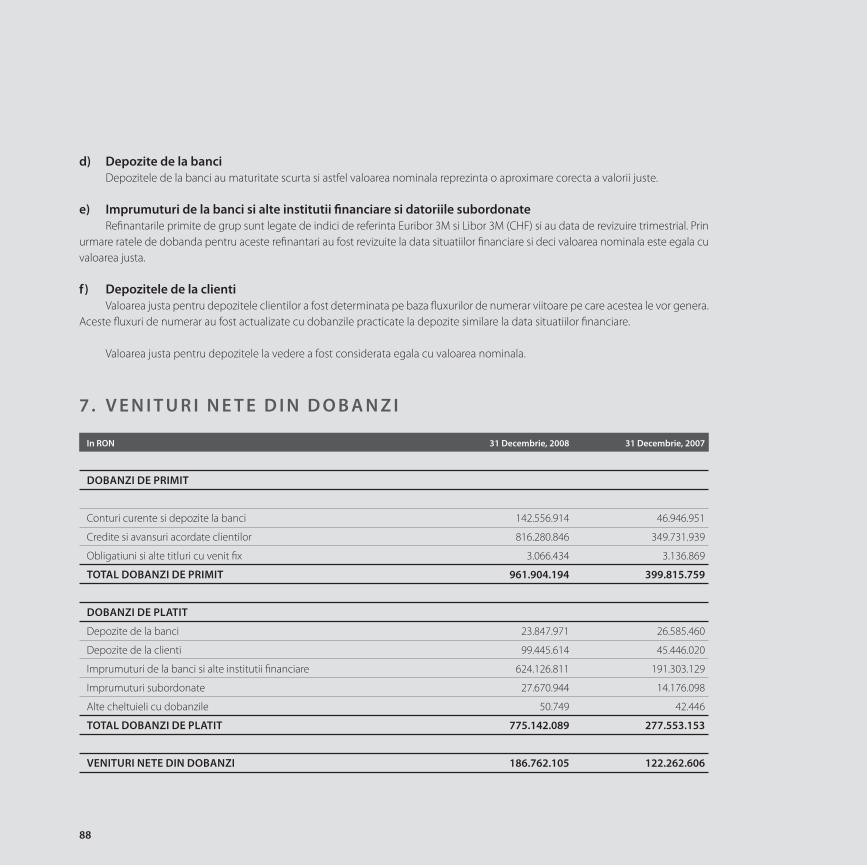

Mai mult decât cifre -...

252

Mai mult decât cifre Raport Anual 2008 Annual Report 2008 Austria Bosnia-Hertegovina Croatia Republica Ceha Slovenia Ungaria ROMÂNIA Serbia Slovacia Ucraina

Transcript of Mai mult decât cifre -...

Mai mult decât cifre

Raport Anual 2008Annual Report 2008

Austria

Bosnia-Hertegovina

Croatia

Republica Ceha

Slovenia

Ungaria

R O M Â N I ASerbia

Slovacia

Ucraina

2

Austria

Bosnia-Hertegovina

Croatia

Republica Ceha

Slovenia

Ungaria

R O M Â N I ASerbia

Slovacia

Ucraina

3

C U P R I N S

M E S A J U L CO M I T E T U LU I D I R E C TO R 4

B A N C A I N C I F R E ( 2 0 0 4 – 2 0 0 8 ) 6

R E T E AUA I N T E R N AT I O N A L A 7

CO N D U C E R E A B A N C I I 8

C L I M AT U L M A C R O E CO N O M I C 9

R E TA I L 1 6

D I V I Z I A CO R P O R AT E 1 8

A C T I V I TAT E A D E T R E ZO R E R I E 2 0

R E Z U LTAT E L E D I R E C T I E I O P E R AT I U N I 2 2

D I V I Z I A CO N T R O L R I S C 2 3

R A P O R T U L CO N S I L I U LU I D E A D M I N I S T R AT I E 2 4

S I T UAT I I F I N A N C I A R E CO N S O L I DAT E 2 5

Raportul auditorilor independenti 27

Contul de profit si pierdere consolidat 30

Bilantul contabil consolidat 32

Situatia consolidata a modificarilor capitalurilor proprii in 2008 34

Situatia consolidata a fluxurilor de numerar in 2008 35

N OT E E X P L I C AT I V E L A D E C L A R AT I I L E F I N A N C I A R E CO N S O L I DAT E 3 9

R E T E AUA N OA S T R A 1 1 7

4

M E S A J U L C O M I T E T U LU I D I R E C TO R

Anul 2008 este pentru Volksbank Romania un an de referinta, banca reusind ca in numai un an sa ajunga de pe pozitia 8 pe pozitia 3 in topul bancilor din Romania, dupa cele mai mari doua banci de retea.

Astfel, la sfarsitul anului 2008 banca inregistra o crestere a activelor bilantiere cu peste 68%, de la 12,64 miliarde ron inregistrate la sfarsitul anului 2007, la 21,34 miliarde ron la sfarsitul lui 2008.

Cresterea semnifi cativa a activelor bilantiere s-a refl ectat si in profi tul inainte de impozitare, care a crescut de peste 6 ori comparativ cu profi tul inregistrat la sfarsitul anului precedent ajungand la suma de 144,4 milioane ron. Cota de piata dupa active a inregistrat si ea o crestere semnifi cativa, ajungand la 6,7% cu cca. 1,7% puncte procentuale crestere fata de sfarsitul lui 2007.

Rezultatele deosebite obtinute de banca in ciuda conditiilor difi cile prin care a trecut sistemul fi nanciar-bancar international in contextul crizei economice mondiale au fost recunoscute si de catre presa, Volksbank Romania fi ind desemnata de catre grupul de presa Finmedia ca fi ind BANCA ANULUI 2008.

Toate aceste rezultate demonstreaza înca o dată faptul ca Volksbank Romania este unul dintre cei mai dinamici jucatori de pe piata, succesul înregistrat de banca avand la baza efortul sustinut al tinerei echipe Volksbank, extinderea canalelor de distributie si nu in ultimul rand de atentia sporita acordată procesului de identifi care si satisfacere a nevoilor clientilor nostri.

Valentin Vancea Herwig BurgstallerGerald SchreinerSimona Fatu(de la stanga la dreapta)

5

Pe langa obtinerea unor bune rezultate fi nanciare, eforturile noastre s-au concentrat si asupra perfectionarii managementului riscului.

Volksbank Romania a indeplinit cu succes cerintele de raportare corespunzatoare abordarilor standard Basel II incepand cu martie 2008, in acelasi timp facandu-se demersurile necesare pentru pregatirea trecerii la abordarea bazata pe ratinguri interne pe riscul de credit. In acest sens au fost luate masuri pentru: monitorizarea calitatii datelor, testarea si imbunatatirea sistemelor de rating, revizuirea procedurilor si proceselor legate de riscul de piata, riscul de credit si riscul de lichiditate.

Herwig Burgstaller

Vicepresedinte

Simona Fatu

Vicepresedinte

Valentin Vancea

Vicepresedinte

Gerald Schreiner

Presedinte

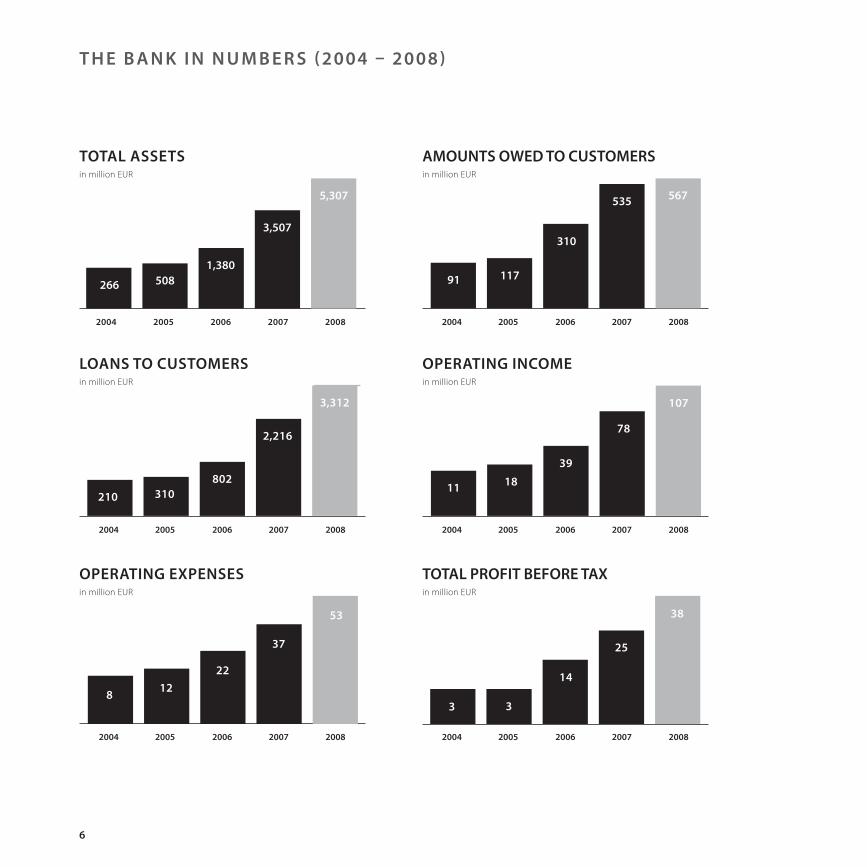

6

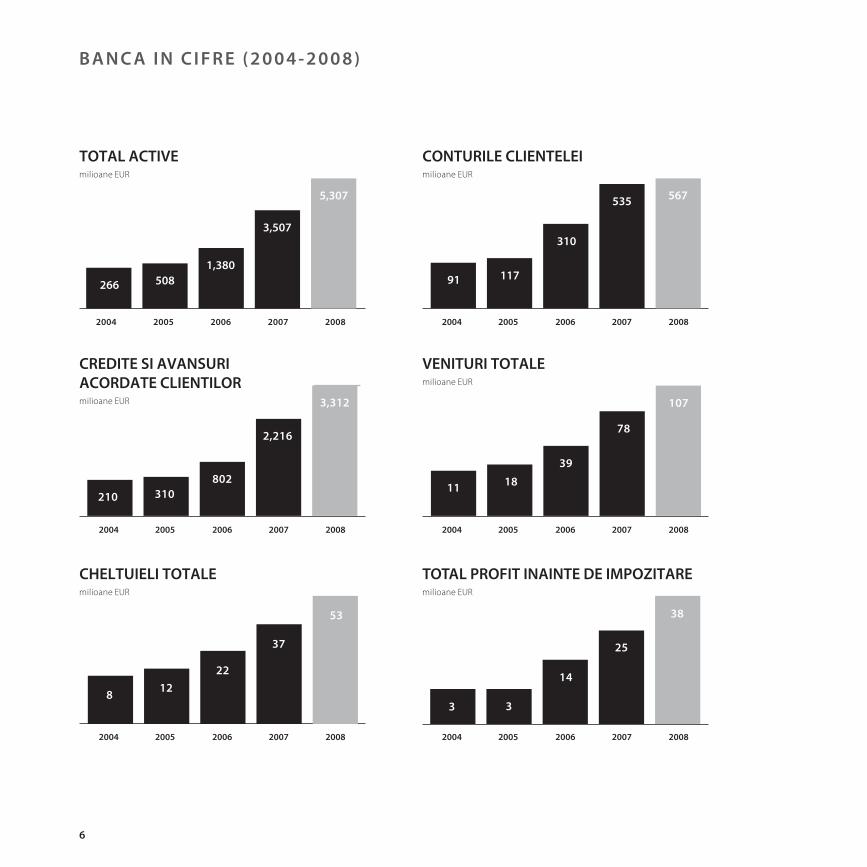

TOTAL ACTIVE milioane EUR

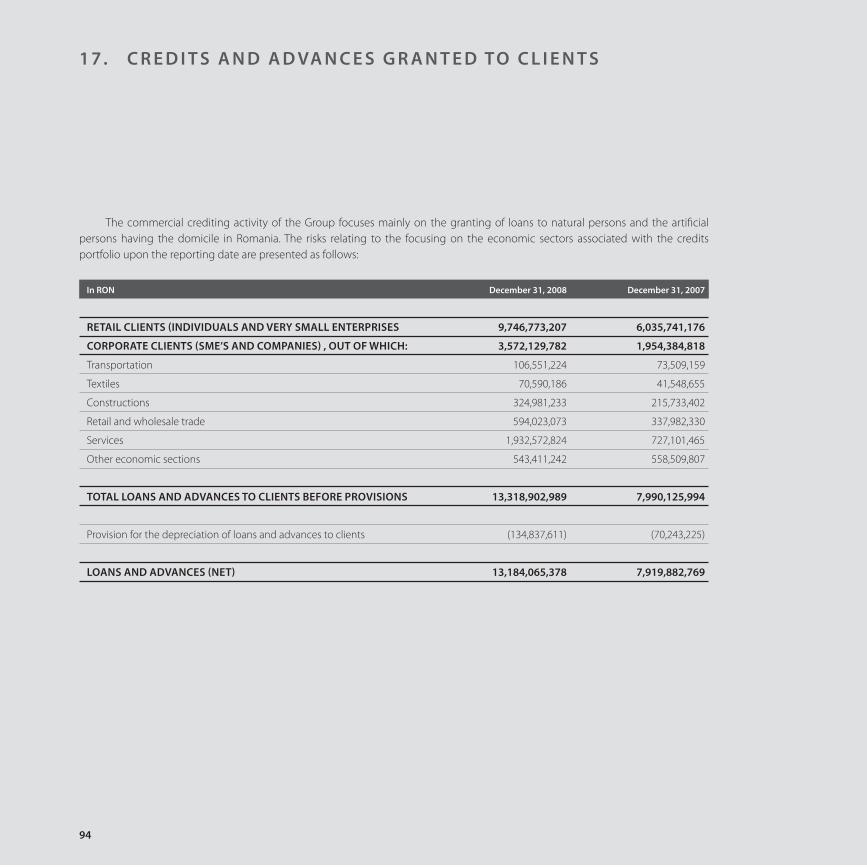

CREDITE SI AVANSURI ACORDATE CLIENTILOR

milioane EUR

CHELTUIELI TOTALE milioane EUR

TOTAL PROFIT INAINTE DE IMPOZITARE milioane EUR

VENITURI TOTALE milioane EUR

CONTURILE CLIENTELEI milioane EUR

2004 2005 2006 2007 2008

266 5081,380

3,507

5,307

91 117

310

535 567

210 310802

2,216

3,312

11 18

39

78

107

8 1222

37

53

33

38

14

25

2004 2005 2006 2007 2008

2004 2005 2006 2007 2008

2004 2005 2006 2007 2008

2004 2005 2006 2007 2008

2004 2005 2006 2007 2008

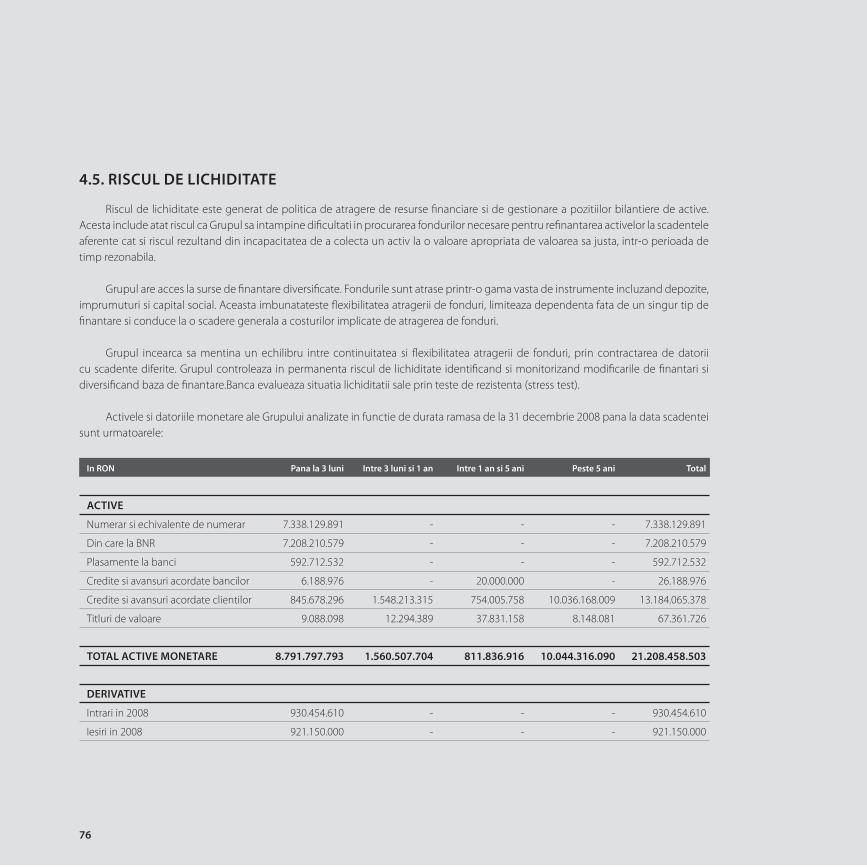

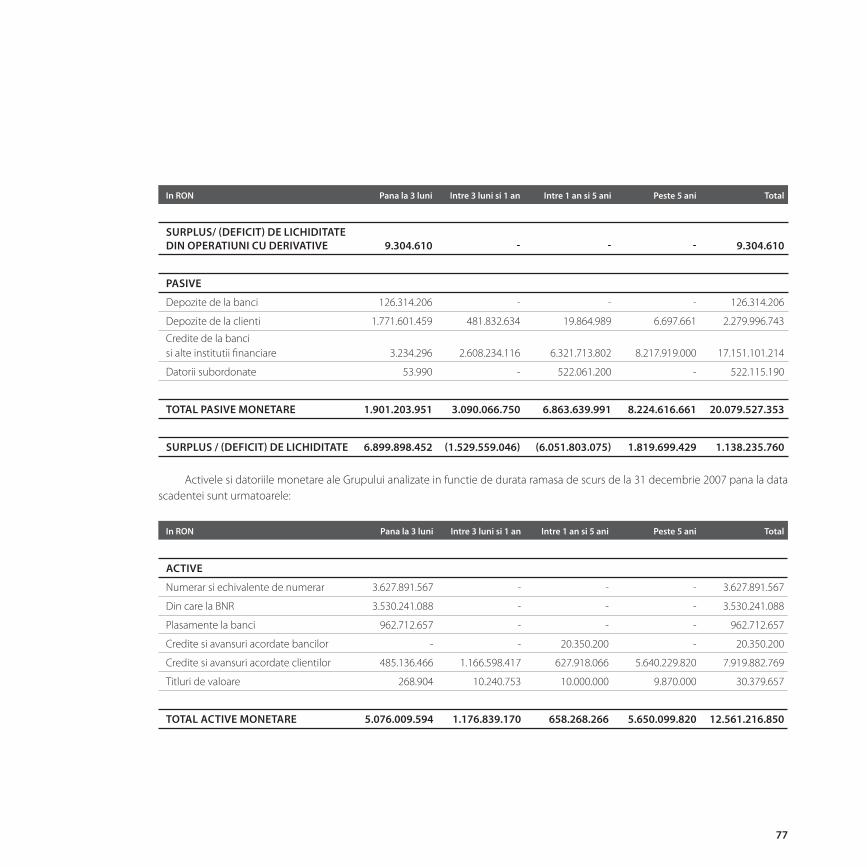

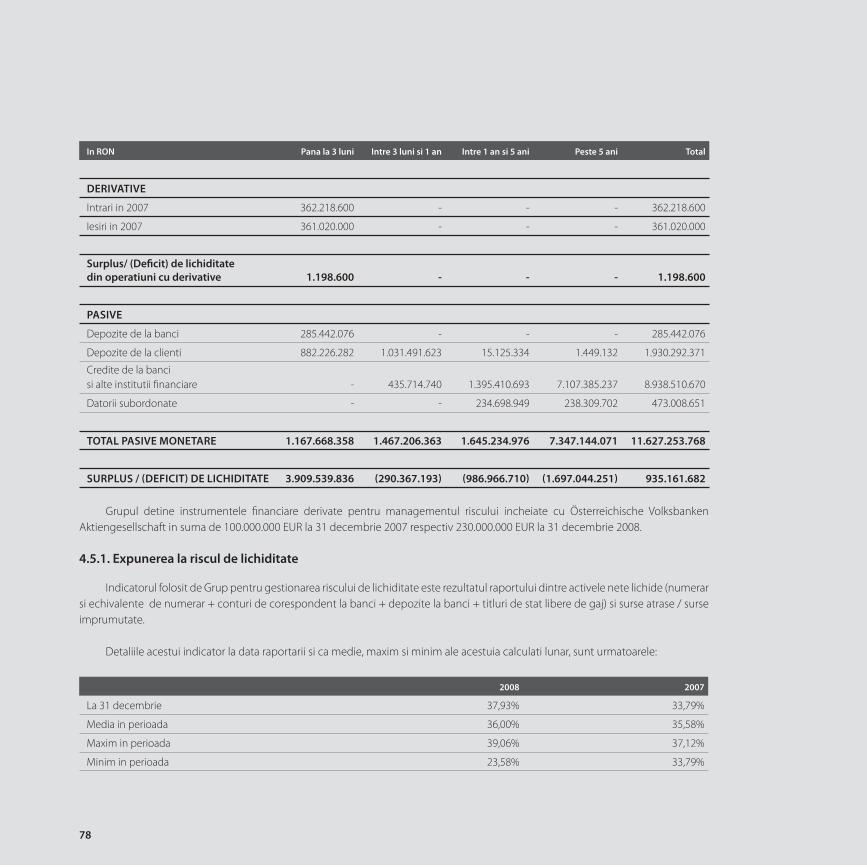

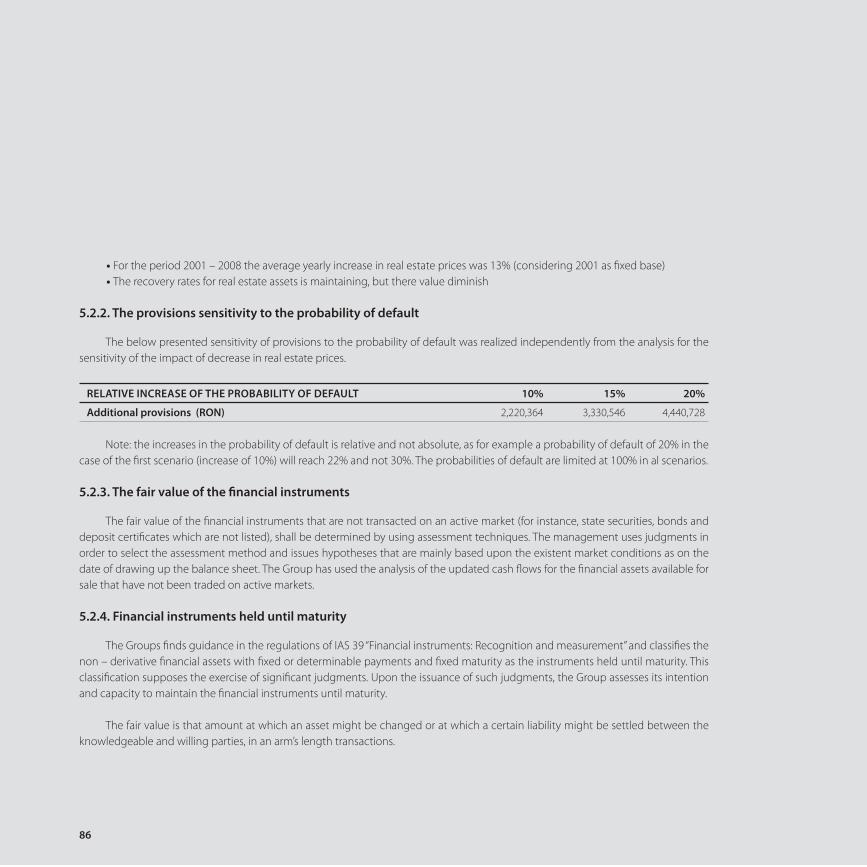

B A N C A I N C I F R E ( 2 0 0 4 - 2 0 0 8 )

7

AUSTRIA

SLOVENIA

CZECH REPUBLIC

SLOVAKIA

CROATIA

BOSNIHERZEGOVINA

SERBIA

UKRAINE

HUNGARY

ROMANIA

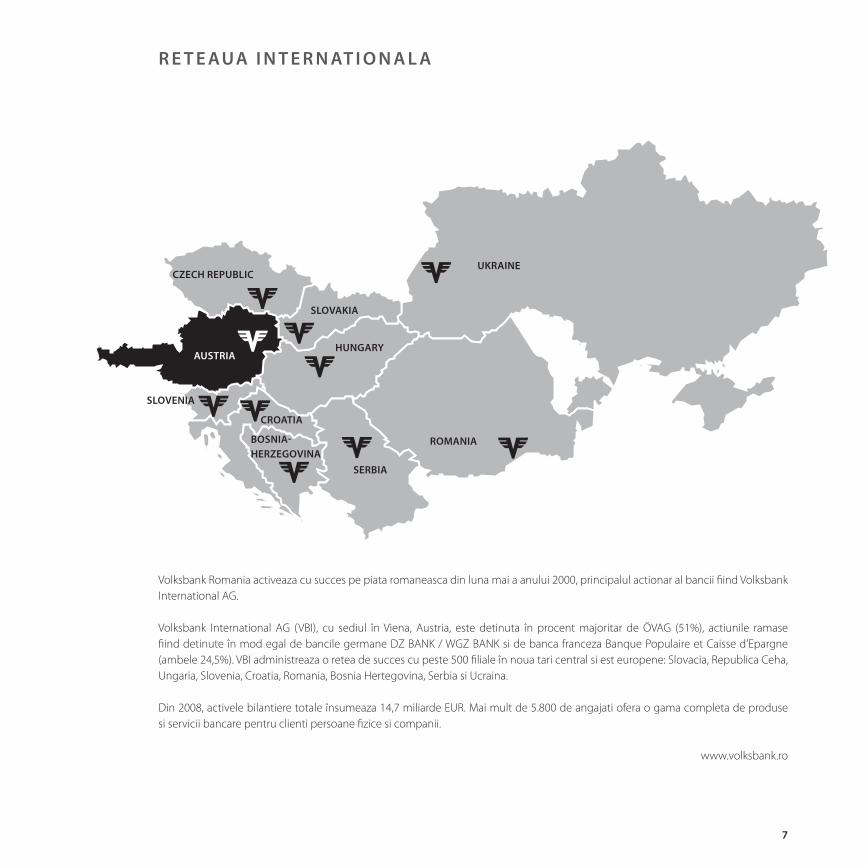

Volksbank Romania activeaza cu succes pe piata romaneasca din luna mai a anului 2000, principalul actionar al bancii fi ind Volksbank International AG.

Volksbank International AG (VBI), cu sediul în Viena, Austria, este detinuta în procent majoritar de ÖVAG (51%), actiunile ramase fi ind detinute în mod egal de bancile germane DZ BANK / WGZ BANK si de banca franceza Banque Populaire et Caisse d’Epargne (ambele 24,5%). VBI administreaza o retea de succes cu peste 500 fi liale în noua tari central si est europene: Slovacia, Republica Ceha, Ungaria, Slovenia, Croatia, Romania, Bosnia Hertegovina, Serbia si Ucraina.

Din 2008, activele bilantiere totale însumeaza 14,7 miliarde EUR. Mai mult de 5.800 de angajati ofera o gama completa de produse si servicii bancare pentru clienti persoane fi zice si companii.

www.volksbank.ro

R E T E AUA I N T E R N AT I O N A L A

8

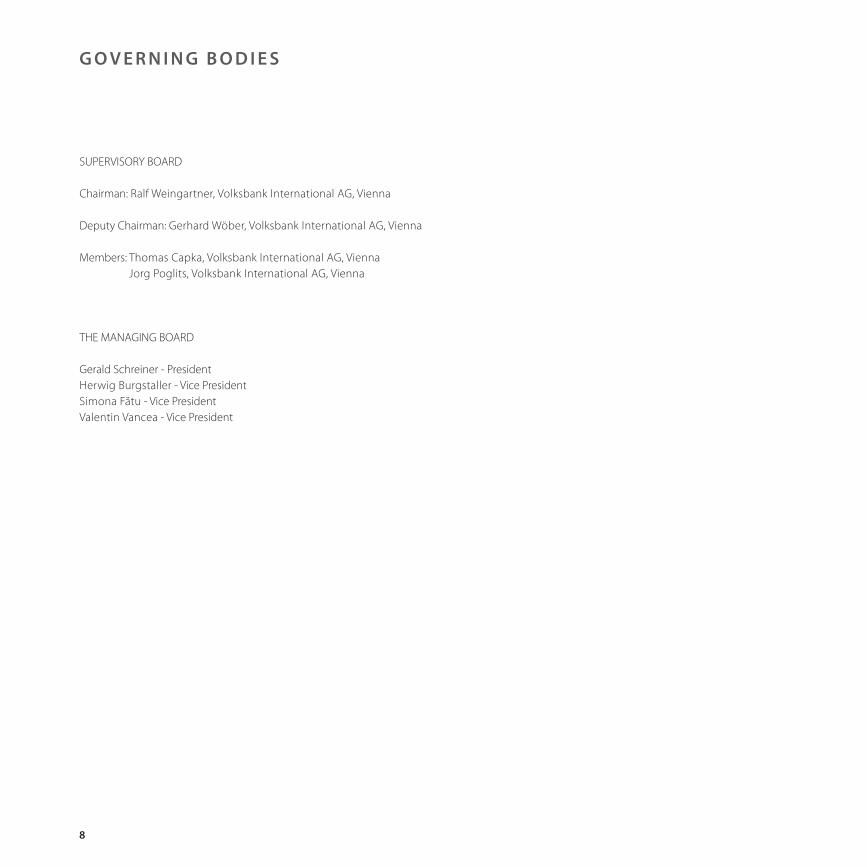

CONSILIUL DE SUPRAVEGHERE

Presedinte: Ralf Weingartner, Volksbank International AG, Viena

Vicepresedinte: Gerhard Wöber, Volksbank International AG, Viena

Membri: Thomas Capka, Volksbank International AG, VienaJorg Poglits, Volksbank International AG, Viena

DIRECTORAT

Gerald Schreiner - Presedinte Herwig Burgstaller - VicepresedinteSimona Fătu - Vicepresedinte Valentin Vancea - Vicepresedinte

C O N D U C E R E A B A N C I I

9

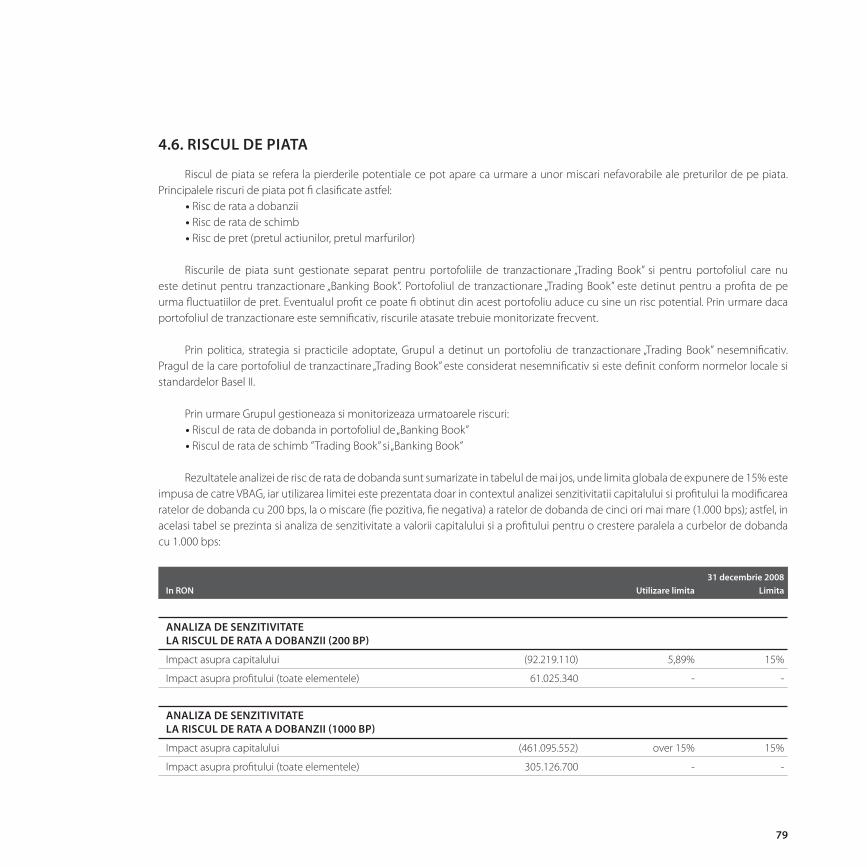

C L I M AT U L M A C R O E C O N O M I C

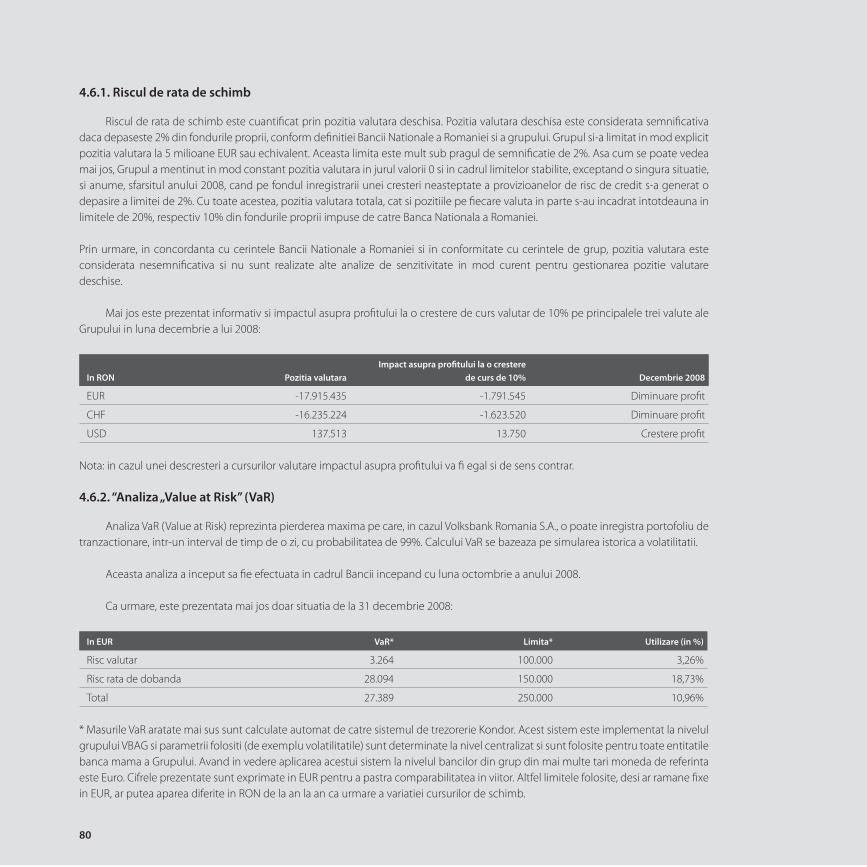

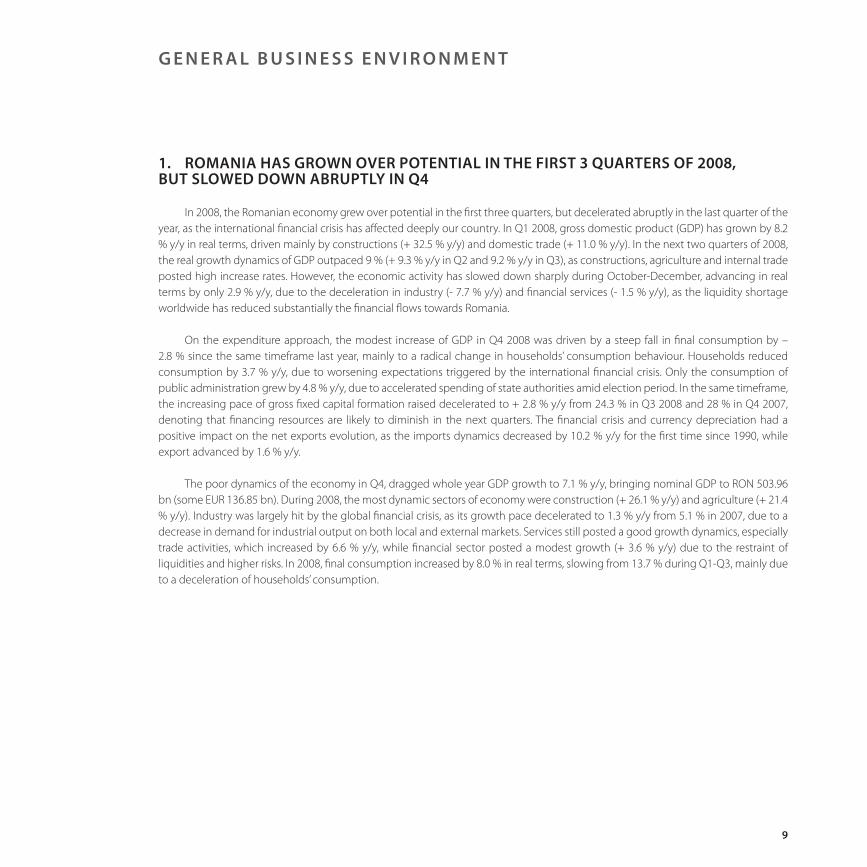

1. ROMANIA A AVUT O CRESTERE ECONOMICA PESTE NIVELUL POTENTIAL IN PRIMELE 3 TRIMESTRE ALE ANULUI 2008, DAR S-A CONFRUNTAT CU O INCETINIRE BRUSCA IN TRIMESTRUL IV

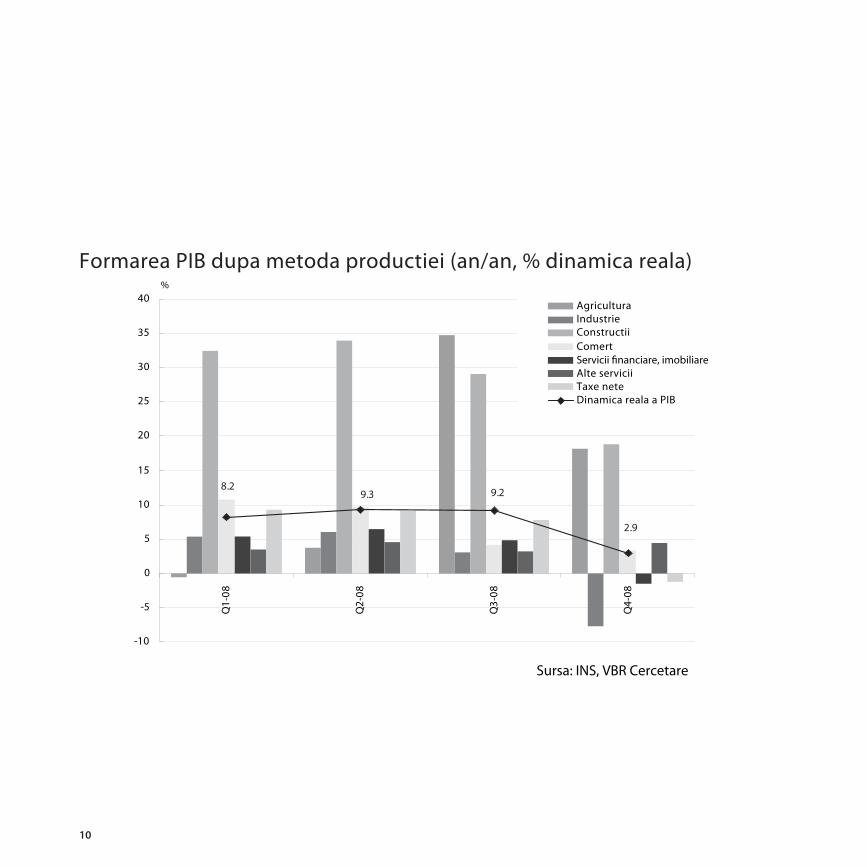

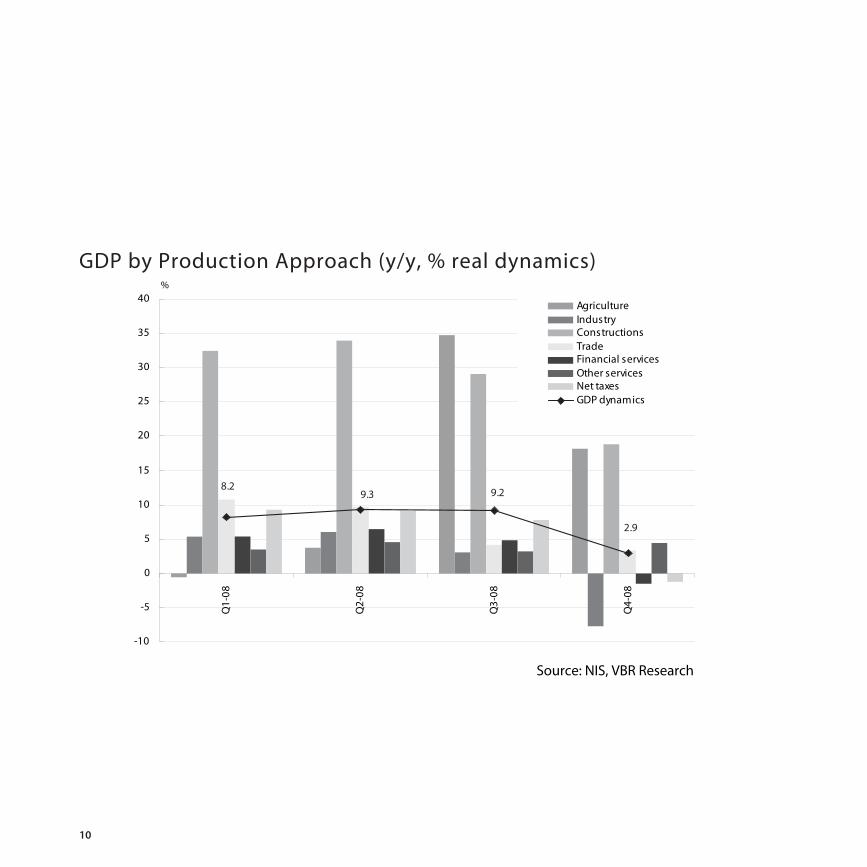

In 2008, economia Romaniei a crescut peste nivelul potential in primele trei trimestre, dar a incetinit brusc in ultimul trimestru al anului, datorita crizei fi nanciare globale care a afectat sever tara noastra. Pe primul trimestru al anului 2008, PIB-ul real a crescut cu 8,2 % an/an, in principal datorita constructiilor (+32,5 % an/an) si comertului intern (+11 % an/an) . In urmatoarele 2 trimestre, PIB-ul real a avut cresteri anuale de peste 9 % ( +9,3 % an/an in semestrul II si +9,2 % an/an in semestrul III) datorita cresterilor semnifi cative din constructii, agricultura si comert intern. In perioada octombrie-decembrie s-a produs o incetinire semnifi cativa a activitatii economice, PIB-ul crescand in termini reali doar cu 2,9 % an/an, pe fondul scaderii activitatii din industrie (-7,7 % an/an) si servicii fi nanciare ( -1,5 % an/an), in conditiile in care criza de lichiditati globala a redus substantial fl uxurile fi nanciare catre Romania.

Utilizand metoda cheltuielilor, cresterea modesta a PIB-ului in trimestrul patru 2008 se explica in special datorita scaderii consumului fi nal cu 2,8 % fata de aceeasi perioada a anului precedent, datorita unei schimbari radicale in comportamentul gospodariilor. Gospodariile si-au redus consumul cu 3,7 % an/an, pe fondul inrautatirii asteptarilor in conditiile crizei fi nanciare internationale. Doar consumul adiministratiei publice a consemnat o crestere de 4,8 % an/an datorita cresterii cheltuielilor autoritatilor statului in contextul alegerilor. Formarea bruta de capital fi x si-a redus rata de crestere de la 24,3 % an/an in trimestrul III al anului 2008 si 28 % an/an in trimestrul IV al anului 2007 la 2,8 % an/an in ultimul trimestru al anului 2008, aratand faptul ca resursele fi nanciare se pot dimininua in urmatoarele trimestre. Criza fi nanciara si deprecierea monedei nationale au avut un eff ect pozitiv in evolutia exporturilor nete, importurile scazand cu 10,2 % an/an pentru prima data dupa 1990 in timp ce exporturile au crescut cu 1,6 % an/an.

Evolutiile slabe din economie in trimestrul IV, au generat o cresterea a PIB-ului per total in 2008 de 7,1 %, valoarea nominala a acestuia fi iind de 503,96 miliarde lei ( 136,85 miliarde euro). In anul 2008, cele mai dinamice sectoare sectoare ale economiei au fost: constructiile (+ 26,1 % an/an) si agricultura ( +21,4 % an/an). Industria a fost sectorul cel mai afectat de criza fi nanciara globala, inregistrand o crestere modesta de 1,3 % an/an in 2008 fata de 5,1 % an/an in 2007, datorita scaderii cererii de produse industriale atat pe piata interna cat si pe cea externa. Seviciile inca au avut o evolutie pozitiva, in special cele legate de comert, care au crescut cu 6,6 % an/an, in timp ce sectorul fi nanciar a avut o crestere modesta de 3,6 % an/an datorita reducerii lichiditatilor si existentei unor riscuri mai mari. In 2008, consumul fi nal a crescut cu 8 % in termeni reali, incetinindu-si ritmul de crestere de la 13,7 % in primele trei trimestre datorita scaderii consumului gospodariilor.

10

8.29.3 9.2

2.9

-10

-5

0

5

10

15

20

25

30

35

40

Q1-

08

Q2-

08

Q3-

08

Q4-

08

%

Sursa: INS, VBR Cercetare

Formarea PIB dupa metoda productiei (an/an, % dinamica reala)

AgriculturaIndustrieConstructiiComertServicii financiare, imobiliareAlte serviciiTaxe neteDinamica reala a PIB

11

Sursa: INS, VBR Cercetare

Q1-

08

Q2-

08

Q3-

08

Q4-

08

Formarea PIB dupa metoda cheltuielilor (an/an, % dinamica reala)

PopulatieAdministratia publicaFormarea bruta de capital fixExporturiImporturiDinamica reala a PIB

12

INFLATIA ANUALIZATA A COBORAT LA 6,3 % LA SFARSITUL ANULUI 2008, PESTE TINTA DE INFLATIE A BNR

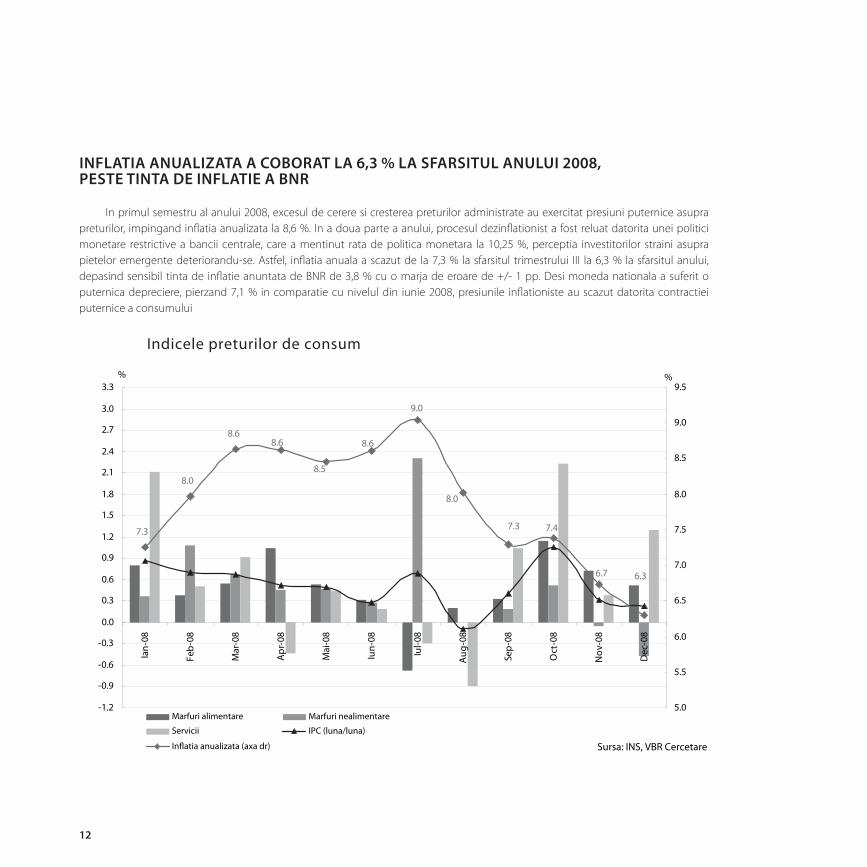

In primul semestru al anului 2008, excesul de cerere si cresterea preturilor administrate au exercitat presiuni puternice asupra preturilor, impingand infl atia anualizata la 8,6 %. In a doua parte a anului, procesul dezinfl ationist a fost reluat datorita unei politici monetare restrictive a bancii centrale, care a mentinut rata de politica monetara la 10,25 %, perceptia investitorilor straini asupra pietelor emergente deteriorandu-se. Astfel, infl atia anuala a scazut de la 7,3 % la sfarsitul trimestrului III la 6,3 % la sfarsitul anului, depasind sensibil tinta de infl atie anuntata de BNR de 3,8 % cu o marja de eroare de +/- 1 pp. Desi moneda nationala a suferit o puternica depreciere, pierzand 7,1 % in comparatie cu nivelul din iunie 2008, presiunile infl ationiste au scazut datorita contractiei puternice a consumului

Indicele preturilor de consum

Sursa: INS, VBR Cercetare

7.3

8.0

8.6

8.5

8.6

9.0

8.0

7.3 7.4

6.7 6.3

8.6

-1.2

-0.9

-0.6

-0.3

0.0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

2.7

3.0

3.3

Ian-

08

Feb-

08

Mar

-08

Apr

-08

Mai

-08

Iun-

08

Iul-0

8

Aug

-08

Sep-

08

Oct

-08

Nov

-08

Dec

-08

%

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5%

Marfuri alimentare Marfuri nealimentare

Servicii IPC (luna/luna)

Inflatia anualizata (axa dr)

13

IN 2008, DEFICITUL FISCAL A CRESCUT LA 4,9 % FATA DE NIVELUL DE 2,3 % INREGISTRAT IN 2007

In 2008, defi citul bugetului general consolidat a urcat la 4,9 % din produsul intern brut (503,96 miliarde lei, aproximativ 136,85 miliarde euro), conform standardelor locale si 5,3 % din PIB conform standardelor ESA 95. In 2008, veniturile totale au reprezentat RON 164,47 mld ( aproximativ RON 44,66 mld), reprezentand 32,6 % din PIB. Veniturile din taxe, au cea mai mare pondere in veniturile totale au ajuns la 94,04 md RON, crescand cu 23,1 % an/an datorita cresterii economice pueternice pe fondul mentinerii nivelului actual al impozitelor. Anul trecut, cheltuielile totale au reprezentat 37,5 % din PIB, avansand cu 38,5 % an/an, astfel ca au ajuns la RON 189,1 mld RON (EUR 51,4 mld). Cheltuielile curente au avut cea mai mare pondere in cheltuielile totale, crescand cu 36,2 % in comparatie cu 2007

DEFICITUL DE CONT CURRENT S-A REDUS LA 12,3 % DIN PIB IN 2008 FATA DE 13,7 % IN 2007

In 2008, defi citul de cont curent al Romaniei a ajuns la EUR 16.877 mio, avand o crestere de 1,2 % fata de nivelul din 2007. Defi citul de cont curent s-a redus la 12,3 % din PIB in 2008 fata de 13,7 % in 2007. Defi citul de cont curent se datoreaza in mare parte dezechilibrului balantei comerciale care reprezinta EUR 18.199 mio, mai mare cu 2,1 % fata de nivelul din 2007, desi dinamica exporturilor a devansat-o pe cea a importurilor cu 4,4 pp. In 2008, balanta veniturilor a avut un defi cit de EUR 5.530 mio, mai mare cu 33 % an/an, datorita repatrierii veniturilor companiilor straine. In aceeasi perioada, transferurile curente au ajuns la RON 6.016 mio, crescand cu 25 % in comparatie cu 2007, ceea ce demonstreaza inca o data ca romanii nu s-au intors acasa in ciuda inrautatirii situatiei pe piata muncii in toata lumea. Investitiile straine directe (ISD) ale nerezidentilor au acoperit doar 53,5 % din defi citul de cont curent, crescand cu 10 % fata de 2007. In 2008, Romania a reusit sa atraga ISD in valoare de EUR 9.024 mio in comparatie cu EUR 7,251 mio in 2007. Investitiile de portofoliu si profi turile reinvestite au reprezentat 50,1 % din totalul investitiilor straine, in timp ce diferenta a fost reprezentata de imprumuturile intra-group.

La sfarsitul anului 2008, imprumuturile externe pe termen mediu si lung au totalizat EUR 51.221 mio, cu 33 % mai mult fata de sfarsitul anului 2007. Pe 31 decembrie 2008, datoria externa public garantata era de EUR 10.733 mio, reprezentand 21 % din datoria externa totala pe termen mediu si lung, in comparatie cu nivelul de 26,5 % la sfarsitul lunii decembrie 2007. In aceeasi perioada, datoria externa privata a fost de EUR 35.021 mio, avand o crestere de 39,5 % fata de 31 decembrie 2007.

14

Sursa: BNR, VBR Cercetare

Balanta de cont curent (12 M basis)

-25

-23

-21

-19

-17

-15

-13

-11

-9

-7

-5

-3

-1

1

3

5

7

9

Ian-08

Feb-08

Mar-08

Apr-08

Mai-08

Iun-08

Iul-0

8

Aug

-08

Sep-08

Oct-08

Nov

-08

Dec-08

mld. EUR

ServiciiTransferuri curente

BunuriVenituriBalanta de cont curent

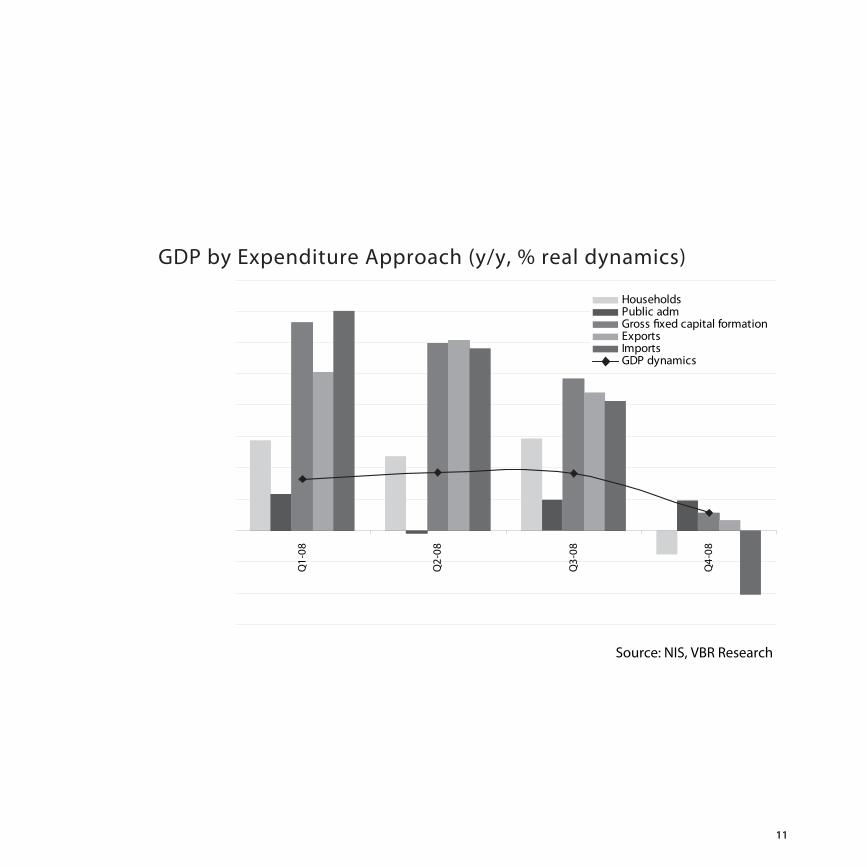

In 2008, rata serviciului datoriei externe pe termen mediu si lung a fost de 29,3 %, majorandu-se cu 6,1 % fata de nivelul din 2007. La sfarsitul lunii decembrie 2008, gradul de acoperire a fost de 5,7 luni de importuri de bunuri si servicii fata de 6,1 luni la sfarsitul anului 2007. In decembrie 2008, datoria pe termen scurt a ajuns la EUR 22.200.4 mio, avand o crestere de 12 % an/an. Datoria totala a Romaniei a atins EUR 73.421 mio in 2008, mai mare cu 25,8 % fata de sfarsitul anului 2007, in timp ce ponderea datoriei pe termen scurt in datoria totala s-a diminuat la 30,2% fata de 34 % in 2007.

15

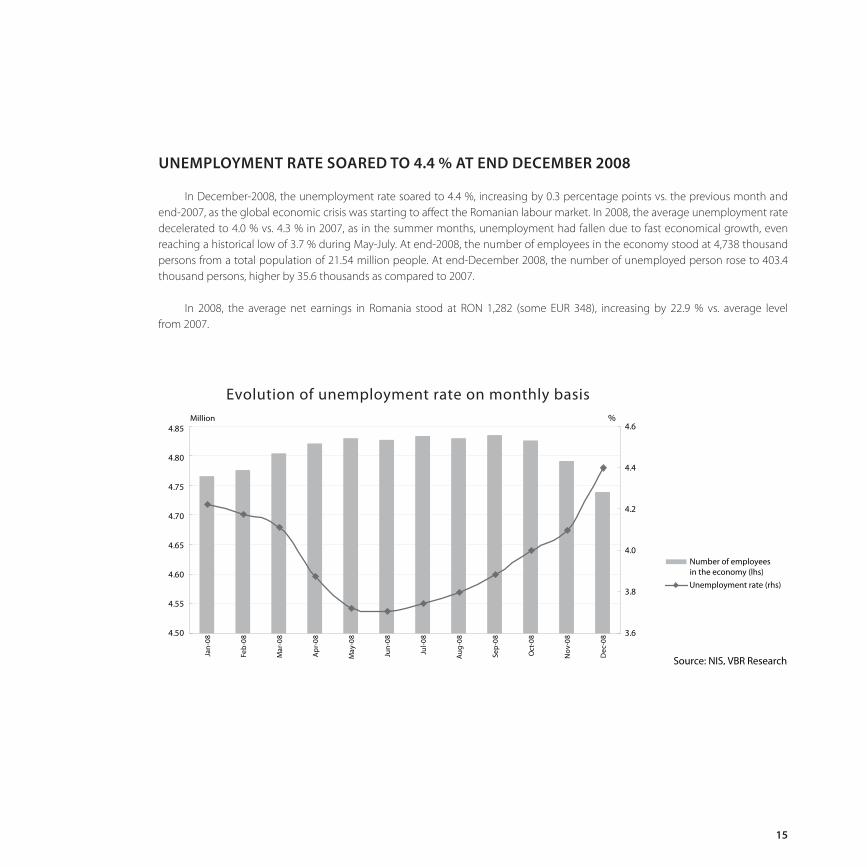

Evolutia ratei somajului pe baze lunare

4.50

4.55

4.60

4.65

4.70

4.75

4.80

4.85Milioane

3.6

3.8

4.0

4.2

4.4

4.6%

Numarul angajatilor din economie (axa stg)Rata somajului (axa dr)

Ian-

08

Feb-

08

Mar

-08

Apr

-08

Mai

-08

Iun-

08

Iul-0

8

Aug

-08

Sep-

08

Oct

-08

Nov

-08

Dec

-08

Sursa: ANOFM, INS, VBR Cercetare

RATA SOMAJULUI A CRESCUT LA 4,4 % LA SFARSITUL LUNII DECEMBRIE 2008

In decembrie 2008, rata somajului a crescut la 4,4 %, majorandu-se cu 0,3 pp fata de luna precedenta, precum si fata de sfarsitul anului 2007, datorita crizei economice globale care incepea sa afecteze piata muncii din Romania. In 2008, rata medie a somajului s-a diminuat la 4.0 % in comparatie cu 4,3 % in 2007, deoarece in lunile de vara, rata somajului a scazut datorita cresterii economice, ajungand la un nivel istoric de 3,7 % in perioada mai-iulie. La sfarsitul anului 2008, numarul de angajati din economie era de 4,74 milioane de persoane dintr-o populatie totala de 21,54 milioane. La sfarsitul lunii decembrie 2008, numarul somerilor a crescut la 403.4 mii persoane, cu 35,6 % mai mult in comparatie cu 2007.

In 2008, salariul mediu net din Romania a fost de RON 1.282 (aproximativ EUR 348), crescand cu 22,9 % fata de aceeasi perioada din 2007.

16

R E TA I L

Incepand cu anul 2008, Volksbank Romania si-a imbunatatit si dezvoltat treptat strategia de vanzari, prin implementarea unei noi viziuni si anume: trasformarea relatiei cu clientii, intr-un parteneriat pe termen lung, concretizat in derularea prin VBR a intregii activitati bancare curente atat pe plan familial, cat si pe lan profesional, sau de afaceri, pe baza accesarii unui numar cat mai mare si mai variat de produse si servicii oferite de banca.

Dispunand de un portofoliul de retail ce cuprindea, la nivelul anului 2008, un numar de aproximativ 150.000 clienti (persoane fi zice si microcompanii), dintre care, peste 80.000 cu facilitati de credit in derulare, Volksbank Romania a extins paleta de produse si servicii oferite clientilor sai, venind in intampinarea dorintelor si necesitatilor lor, prin aplicarea acestei noi abordari, ce a continuat si in prima parte a anului 2009 si va continua si in urmatorii 2 ani.

Astfel, in vara anului 2008 au fost lansate pachetele de produse si servicii, ce contin, in functie de posibilitatile fi nanciare ale fi ecarui client, o serie de facilitati si discounturi, aplicate produselor si serviciilor incluse (conturi curente, carduri de debit, produse de credit, serviciul de internet banking gratuit), dar si operatiunilor bancare efectuate de clienti in cadrul acestor pachete (plati gratuite, retrageri gratuite etc).

Tot in vara anului 2008 a fost lansat noul serviciu de internet banking – VB Direct, unul dintre cele mai competitive din sistemul bancar romanesc, care ofera nu numai o utilizarea foarte usoara si efi cienta, fi ind un serviciu extrem de „prietenos” cu clientul, ci ofera in acelasi timp si posibilitatea efectuarii oricaror tipuri de operatiuni bancare (deschidere de noi conturi, constituire depozite, plati, transferuri, plata utilitati, efectuare schimburi valutare, verifi care solduri existente, verifi care extrase de cont, verifi care grafi ce de rambursare aferente creditelor contractate etc).

Urmare a implementarii acestui serviciu performant de internet banking, Volksbank Romania a continuat sa se preopcupa de cerintele si nevoile clientilor sai, venind in intampinarea acestora cu o noua paleta de produse, orientate de acesta data spre economisire: conturile curente speciale: „Junior”, „Student”, „Bunici”, „Dinamic”.

Prin aceste produse noi banca s-a adresat atat segmentelor existente de clientela (prin contul Dinamic – oferit atat persoanelor fi zice, cat si microcompaniilor), cat si unor segmente noi, cum sunt copiii, studentii, pensionarii, oferind pentru fi ecare categorie tinta, conturi curente cu dobanzi atractive, ce au incluse produse, operatiuni si servicii gratuite sau cu discount-uri avantajoase. Lansarea acestor produse de cont curent acopera in ansamblu toate ariile de interes ale persoanelor fi zice, de la conturile dedicate incasarii/virarii salariilor si a altor tipuri de venituri, la conturile dedicate copiilor si parintilor pentru incasarea si gestionarea economica si efi cienta a sumelor provenite din alocatiile de stat pentru copii si a alte drepturi de prestatii sociale, la conturile dedicate studentilor pentru incasarea si economisirea burselor scolare si a altor drepturi banesti si pana la conturile dedicate pensionarilor pentru incasarea pensiilor si altor drepturi banesti si chiar pentru economisirea resurselor disponibile.

Ca o continuare a acestui proces, la fi nele anului trecut a fost lansat un nou concept pe piata romaneasca: pachetul special de produse si servicii – VB Direct Bank – produs ce se adreseaza clientilor persoane fi zice cu resurse de timp limitate si care urmaresc derularea tuturor operatiunilor bancare intr-o maniera rapida, efi cienta si economica.

17

In plus, acest concept nou urmareste pe de-o parte revolutionarea si inovarea operatiunilor bancare clasice, derulate la ghiseele bancii, iar pe de alta parte, indrumarea persoanelor fi zice catre o forma mult mai confortabila si mai efi cienta de utilizare si accesare a produselor si serviciilor bancare - prin internet, in orice moment si in orice loc: acasa, la servici, in concediu etc.Prin pachetul special VB Direct Bank, Volksbank le ofera clientilor sai, existenti si noi, posibilitatea:

• Economisirii si gestionarii efi ciente a timpului alocat tranzactiilor si operatiunilor bancare;• Economisirii si gestionarii efi ciente a veniturilor si resurselor banesti – atat prin oferirea unor dobanzi extrem de atractive la conturile curente incluse in acest produs, cat si prin aplicarea unor costuri extrem de reduse produselor, serviciilor incluse si operatiunilor efectuate in cadrul acestui pachet (include servciul de internet banking gratuit, card debit gratuit si discount-uri de pana la 75% la operatiuni pe cont sau card);• Realizarii tuturor tranzactiilor bancare in timp extrem de scurt: prin accesarea servciului de internet banking inclus in pachet din orice loc si in orice moment.

Totodata, in cursul anului 2008, Volksbank Romania si-a extins gama de produse si servicii destinate IMM-urilor fi ind lansate pachete de produse si servicii dedicate acestora, cu costuri atractive si incluzand o serie de facilitati si discounturi, atat la produsele si serviciile incluse, cat si la o serie de operatiuni uzuale.In ceea ce priveste produsele de fi nantare oferite microcompaniilor, acestea au fost imbunatatite si diversifi cate, fi ind dezvoltate produse speciale pentru microcompanii sau entitati ce activeaza in diferite profesii liberale: medici, notari, avocati, etc.

In consecinta, la fi nele anului 2008, strategia Volksbank Romania de a diversifi ca si extinde tipurile de produse oferite, precum si de a atrage segmente noi de clientela a condus la ocuparea celei de-a treia pozitii in topul bancilor din sistemul bancar romanesc, pozitie datorata in mare masura dinamicii si dezvoltarii activitatii de retail.

18

D I V I Z I A C O R P O R AT E

Este un fapt bine stiut ca afacerea de baza a segmentului corporat din cadrul VBR a fost reprezentata de fi nantarea SME si de fi nantarea imobiliara. Finantarea SME ramane un segment tinta, pe tot parcursul anului 2008; fi nantarea imobiliara atingea nivelul Q3 in 2008, cand, datorita crizei internationale, strategia de grup a tarilor din cadrul Comunitatii Economice Europene a schimbat aborda-rea pentru acest segment. In consecinta, conducerea VBR a decis sa opreasca fi nantarea imobiliara din Q4 2008 si a pornit o procedura de restructurare si reprogramare pentru acest segment. Acestea fi ind spuse, activitatea din segmentul corporat pe parcursul anului 2008 a fost defi nita de dinamism, portofoliul de imprumut crescand cu cca. 36% fata de anul trecut.

In ceea ce priveste segmentul corporat si cel referitor la SME, evolutia anului 2008, transpusa in cifre, arata ca volumul de credit corporat a crescut cu 85% din decembrie 2007, in acelasi timp mentinand un portofoliu de imprumut de inalta calitate – rata implicita fi ind de 0,1%.

In zona tranzactiilor, trebuie mentionata lansarea VB Direct (Q2 2008) ca o platform integrata de e-banking, care a contribuit la imbunatatirea tranzactiilor corporate, alaturi de implementarea solutiei de scanare la nivel de sucursala pentru ordine de plata pe hartie. Aceste progrese au infl uentat in mod pozitiv calitatea si viteza procesarii platilor, determinand o migratie din sectorul platilor pe hartie catre cel electronic.

Abordarea pentru anul 2009 va continua sa consolideze pozitia pe segmentul de afaceri referitor la SME (companii cu o cifra de afaceri intre 1 milioane EUR si 50 milioane EUR) si se va adresa unei noi nise de piata reprezentata de fi nantarea proiectelor municipa-litatii si a acelora de infrastructura. Aceasta turnura in strategie, de inlocuire a fi nantarii imobiliare cu cea a proiectelor municipalitatii (risc suveran) este determinata de schimbarile din climatul economic si de noua abordare a riscului din partea VBR/VBI.

In vederea obtinerii succesului in cadrul liniei de afaceri propuse de strategia corporata pentru 2009, accentul va cadea pe urmatoarele directii majore:

Imbunatatirea continua a calitatii produselor si a serviciilor oferite clientilor-corporatii sau SME; Lansarea unor produse corporate standard dedicate atat administrarii numerarului, cat si a cerintelor fi nanciare ale

clientilor; Marirea profi tabilitatii in sectorul corporat si SME prin implementarea sistemului CRM, capabil sa masoare profi tabilitatea

per client si per manager de relatii; Sporirea veniturilor provenite din activitati de cross selling, avand in vedere caracteristicile acestui segement de afaceri.

19

Biroul pentru Clienti Internationali va urmari strategia de piata a VBR de a se adresa clientilor pe baza specifi cului activitatii lor.

Astfel, Biroul pentru Clienti Internationali isi doreste sa ofere o consultanta completa si de specialitate investitorilor austrieci, germani, italieni sau francezi, dar si investitorilor romani cu actiuni in strainatate.

Divizia este structurata pe 3 birouri internationale, in functie de originea clientului (Austria, Germania, Italia sau Franta etc.) si aduna o serie de specialisti care sa poata aborda clientul in limba sa materna.

Mai mult, departamentele dedicate acestui tip de clienti-corporatii activeaza ca centre coordonatoare si se adreseaza princi-palelor sucursale din Romania ale companiilor austriece, germane, italiene sau franceze.

Biroul pentru Clienti Internationali administreaza un portofoliu de cca. 1000 de clienti, din care 211 aveau facilitati de credit active cu un volum total de creditare in jurul a 120 milioane EUR la sfarsitul anului 2008 - cu 30% mai mult decat la fi nele lunii decembrie 2007.

Principalul scop pentru anul 2009 este mentinerea si cresterea bazei de date a clientilor prin crearea unei relatii de calitate si prin croirea de solutii fi nanciare care sa se potriveasca cat mai bine mentalitatii bancare occidentale a acestei tipologii de clienti.

20

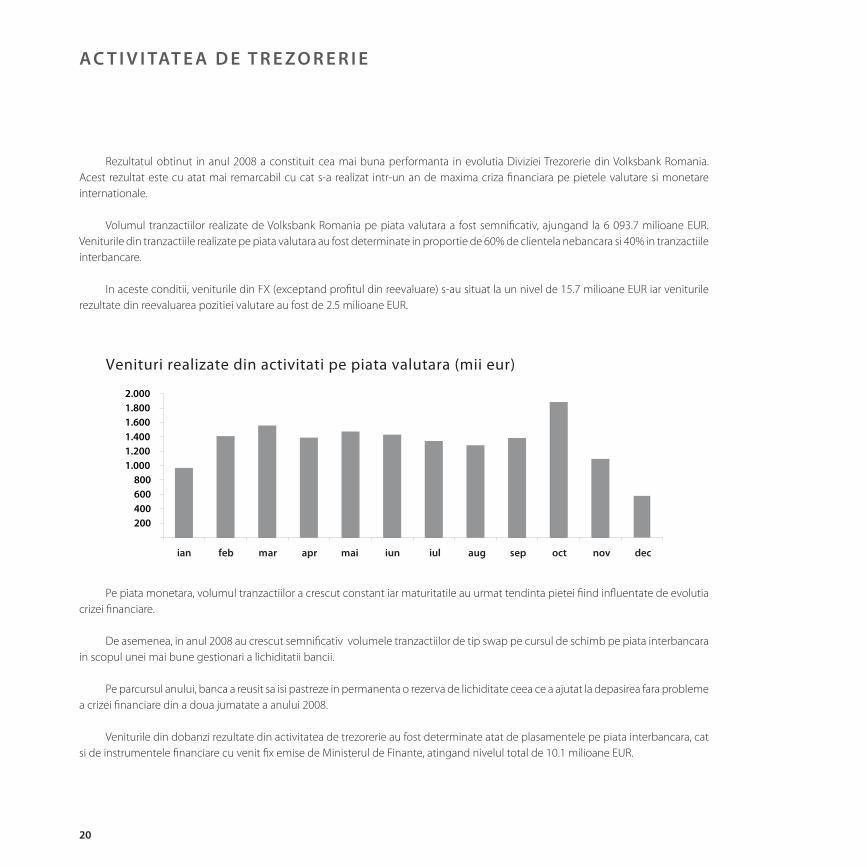

A C T I V I TAT E A D E T R E Z O R E R I E

Rezultatul obtinut in anul 2008 a constituit cea mai buna performanta in evolutia Diviziei Trezorerie din Volksbank Romania.Acest rezultat este cu atat mai remarcabil cu cat s-a realizat intr-un an de maxima criza fi nanciara pe pietele valutare si monetare internationale.

Volumul tranzactiilor realizate de Volksbank Romania pe piata valutara a fost semnifi cativ, ajungand la 6 093.7 milioane EUR. Veniturile din tranzactiile realizate pe piata valutara au fost determinate in proportie de 60% de clientela nebancara si 40% in tranzactiile interbancare.

In aceste conditii, veniturile din FX (exceptand profi tul din reevaluare) s-au situat la un nivel de 15.7 milioane EUR iar veniturile rezultate din reevaluarea pozitiei valutare au fost de 2.5 milioane EUR.

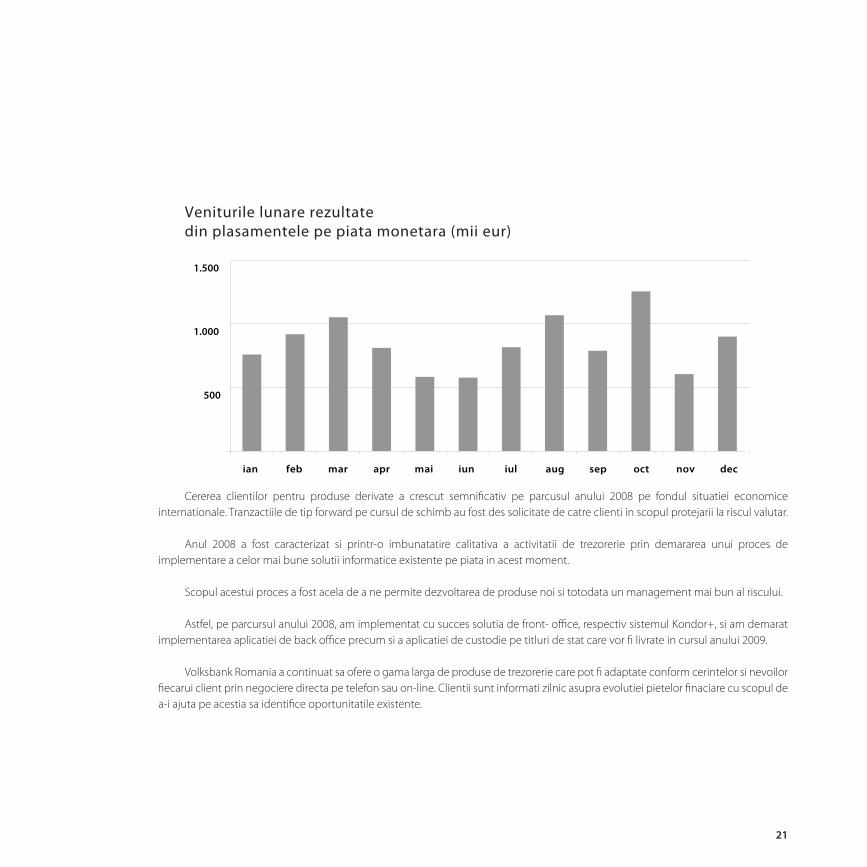

Pe piata monetara, volumul tranzactiilor a crescut constant iar maturitatile au urmat tendinta pietei fi ind infl uentate de evolutia crizei fi nanciare.

De asemenea, in anul 2008 au crescut semnifi cativ volumele tranzactiilor de tip swap pe cursul de schimb pe piata interbancara in scopul unei mai bune gestionari a lichiditatii bancii.

Pe parcursul anului, banca a reusit sa isi pastreze in permanenta o rezerva de lichiditate ceea ce a ajutat la depasirea fara probleme a crizei fi nanciare din a doua jumatate a anului 2008.

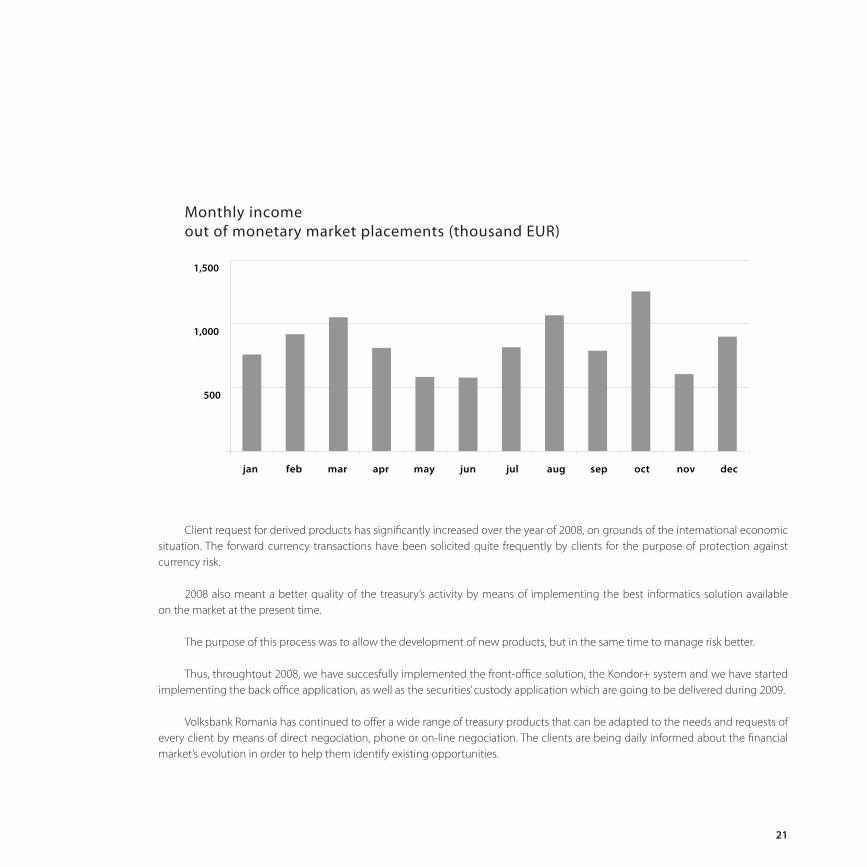

Veniturile din dobanzi rezultate din activitatea de trezorerie au fost determinate atat de plasamentele pe piata interbancara, cat si de instrumentele fi nanciare cu venit fi x emise de Ministerul de Finante, atingand nivelul total de 10.1 milioane EUR.

Venituri realizate din activitati pe piata valutara (mii eur)

200400600800

1.0001.2001.4001.6001.8002.000

ian feb mar apr mai iun iul aug sep oct nov dec

21

Cererea clientilor pentru produse derivate a crescut semnifi cativ pe parcusul anului 2008 pe fondul situatiei economice internationale. Tranzactiile de tip forward pe cursul de schimb au fost des solicitate de catre clienti in scopul protejarii la riscul valutar.

Anul 2008 a fost caracterizat si printr-o imbunatatire calitativa a activitatii de trezorerie prin demararea unui proces de implementare a celor mai bune solutii informatice existente pe piata in acest moment.

Scopul acestui proces a fost acela de a ne permite dezvoltarea de produse noi si totodata un management mai bun al riscului.

Astfel, pe parcursul anului 2008, am implementat cu succes solutia de front- offi ce, respectiv sistemul Kondor+, si am demarat implementarea aplicatiei de back offi ce precum si a aplicatiei de custodie pe titluri de stat care vor fi livrate in cursul anului 2009.

Volksbank Romania a continuat sa ofere o gama larga de produse de trezorerie care pot fi adaptate conform cerintelor si nevoilor fi ecarui client prin negociere directa pe telefon sau on-line. Clientii sunt informati zilnic asupra evolutiei pietelor fi naciare cu scopul de a-i ajuta pe acestia sa identifi ce oportunitatile existente.

Veniturile lunare rezultate din plasamentele pe piata monetara (mii eur)

500

1.000

1.500

ian feb mar apr mai iun iul aug sep oct nov dec

22

R E Z U LTAT E L E D I R E C T I E I O P E R AT I U N I

Activitatea Directiei Operatiuni acopera o mare parte a activitatii de Back offi ce. Alaturi de departamentele: Plati, Afaceri documentare si Corespondenti bancari, Back offi ce Carduri, Trezorerie - Back offi ce, in cursul anului 2008 au inceput sa functioneze si departamentele Cash Management, Custodie si Suport sucursale, acoperind segmente noi, in conformitate cu nevoile clientilor si ale organizarii interne.

In cursul anului 2008, principala realizare a Departamentului Plati a constat in implementarea unui soft de scanare, care a permis centralizarea procesarii platilor si a schimburilor valutare, ceea ce a permis efi cientizarea activitatii de Back offi ce, in sensul realizarii unei economii de personal de 36 FTE, aceste resurse fi ind realocate activitatii de business.

Urmare unor volume sporite de tranzactii, comisioanele realizate din procesarea platilor au fost de 3.5 milioane Eur.

Departamentul afaceri documentare a inregistrat si in anul 2008 o crestere a volumului de activitate, oferindu-le clientilor corporativi si de retail suportul necesar pentru derularea de acreditive, incasso si emitere de scrisori de garantie. Profesionalismul si asistenta de specialitate oferita clientilor a contribuit la realizarea unui volum de venituri de 0,6 milioane Eur.

Departamentul Trezorerie - Back offi ce a demarat in cursul anului 2008 implementarea unui soft dedicat, prima faza fi ind incheiata cu succes, urmand ca in anul 2009 aceasta implementare sa continue pentru produsele complexe pe care banca doreste sa le ofere clientilor sai, contribuind major la obtinerea unor venituri sporite.

Departamentul Custodie a fost creat cu scopul de a furniza servicii de custodie pentru pastrarea in siguranta atat a valorilor mobiliare, cat si a titlurilor de stat, decontarea si inregistrarea acestora, colectarea veniturilor, evaluarea portofoliilor, contribuind la diversifi carea produselor oferite clientilor si a veniturilor aferente.

Departamentul Cash Management, creat cu scopul de a efi cientiza activitatea de gestionare a numerarului, a urmarit si a realizat in primul rand reducerea costurilor de transport si de alimentare printr-o mai buna redistribuire intre unitati si in al doilea rand cresterea veniturilor ca urmare a plasarii optime a excedentului.

23

D I V I Z I A C O N T R O L R I S C

In anul 2008 activitatea Diviziei Control Risc s-a concentrat in principal pe implementarea cerintelor Basel II. Volksbank Romania a indeplinit cu succes cerintele de raportare corespunzatoare abordarilor standard Basel II incepand cu martie 2008. In acelasi timp s-au facut demersuri pentru pregatirea trecerii la abordarea bazata pe ratinguri interne pe riscul de credit. In acest sens au fost luate masuri pentru: monitorizarea calitatii datelor, testarea si imbunatatirea sistemelor de rating, revizuirea procedurilor si proceselor legate de riscul de piata, riscul de credit si riscul de lichiditate.

Divizia a contribuit la continuarea integrarii in activitatea zilnica a bancii a masurilor de risc precum RAROC, pierderi asteptate, PD si LGD.

In zona riscului de piata s-a inceput folosirea softului Kondor+ atat pentru monitorizarea zilnica a riscurilor cat si pentru raportari.

Avand in vedere situatia actuala, o atentie deosebita a fost acordata testelor de stress privind riscurile de rata de schimb, riscul de rata a dobanzii, lichiditate si pretul activelor imobiliare.

De asemenea, in a doua parte a anului cadrul de monitorizare si gestionare a lichiditatii a fost intarit considerabil atat prin cresterea frecventei de monitorizare cat si prin cooperarea mai stransa cu Diviziile Trezorerie si Financiar-Contabilitate.

24

R A P O R T U L C O N S I L I U LU I D E A D M I N I S T R AT I E

Anul 2008 a fost pentru Volksbank anul in care banca si-a consolidat pozitia pe piata de retail banking ajungand pe locul trei in topul bancilor din Romania.

Astfel, in numai un an, valoarea totala a activelor bilantiere ale bancii a crescut comparativ cu sfarsitul anului 2007 cu cca 68% pana la nivelul 21,34 miliarde ron banca reusind astfel sa ajunga la o cota de piata de 6,79% si sa obtina un profi t inainte de impozitare de 144,44 milioane ron.

Rezultatele din acest an ale Volksbank Romania au confi rmat toate asteptarile legate de potentialul pietei si au intarit increderea Consiliului de Administratie in strategia aplicata de managementul local:concentrarea atentiei catre segmentul reprezentat de persoanele fi zice pe de o parte si de cel reprezentat microintreprinderi sio societati mici si mijlocii pe de alta parte.

In ceea ce priveste indicatorii fi nanciari, registrele si situatiile contabile precum si celelalte rapoarte referitoare la activitatea bancii din 2007, au fost auditate de catre fi rma de audit KPMG Audit SRL nefi nd gasite motive de obiectie, conturile fi ind aprobate fara rezerve.

In fi nal, Consiliul de Administratie doreste sa multumeasca tuturor clientilor si colaboratorilor sai, Comitetului de Directie si intregului personal al bancii care s-au implicat activ in obtinerea rezultatelor pozitive inregistrate de Volksbank Romania in cei 8 ani de activitate.

Bucuresti, Apr. 2009

25

Situaţii Financiare Consolidate

VolksbankRomânia S.A.

26

27

R A P O R T U L AU D I TO R I LO R I N D E P E N D E N T I

RAPORT ASUPRA SITUATIILOR FINANCIARE CONSOLIDATE

Am auditat situatiile fi nanciare consolidate anexate ale societatii Volksbank Romania S.A. („Banca“) si fi lialei sale („Grupul“), care cuprind bilantul contabil consolidat la data de 31decembrie 2008, contul de profi t si pierdere consolidat, situatia consolidata a modifi carilor capitalului propriu si situatia consolidata a fl uxurilor de trezorerie pentru exercitiul incheiat la aceasta data si un sumar al politicilor contabile semnifi cative si alte note explicative.

RESPONSABILITATEA CONDUCERII PENTRU SITUATIILE FINANCIARE CONSOLIDATE

Conducerea Bancii este responsabila pentru intocmirea si prezentarea fi dela a acestor situatii fi nanciare consolidate in conformitate cu Standardele Internationale de Raportare Financiara adoptate de Uniunea Europeana. Aceasta responsabilitate include: proiectarea, implementarea si mentinerea sistemului de control intern asupra intocmirii si prezentarii fi dele a unor situatii fi nanciare consolidate care sa nu prezinte denaturari semnifi cative, datorate fi e fraudei, fi e erorii; selectarea si aplicarea politicilor contabile adecvate; elaborarea unor estimari contabile rezonabile in circumstantele date.

RESPONSABILITATEA AUDITORULUI

Responsabilitatea noastra este ca, pe baza auditului efectuat, sa exprimam o opinie asupra situatiilor fi nanciare consolidate ale Grupului. Noi am efectuat auditul conform standardelor de audit adoptate de Camera Auditorilor Financiari din Romania. Aceste standarde cer ca noi sa respectam cerintele etice, sa planifi cam si sa efectuam auditul in vederea obtinerii unei asigurari rezonabile ca situatiile fi nanciare consolidate nu cuprind denaturari semnifi cative.

Un audit consta in efectuarea de proceduri pentru obtinerea probelor de audit cu privire la sumele si informatiile prezentate in situatiile fi nanciare consolidate. Procedurile selectate depind de rationamentul profesional al auditorului, incluzand evaluarea riscurilor de denaturare semnifi cativa a situatiilor fi nanciare consolidate, datorate fraudei sau erorii. In evaluarea acestor riscuri, auditorul ia in considerare controlul intern relevant pentru intocmirea si prezentarea fi dela a situatiilor fi nanciare consolidate pentru a stabili procedurile de audit relevante in circumstantele date, dar nu si in scopul exprimarii unei opinii asupra efi cientei controlului intern al entitatilor din Grup. Un audit include, de asemenea, evaluarea gradului de adecvare a politicilor contabile folosite si rezonabilitatea estimarilor contabile elaborate de catre conducere, precum si evaluarea prezentarii situatiilor fi nanciare consolidate luate in ansamblul lor.

Consideram ca evidentele de audit pe care le-am obtinut sunt sufi ciente si adecvate pentru a constitui baza opiniilor noastre de audit.

28

OPINIA

In opinia noastra, situatiile fi nanciare consolidate anexate ale Grupului redau o imagine fi dela, in toate aspcetele semnifi cative, a pozitiei fi nanciare a Grupului la data de 31 decembrie 2008, precum si a rezultatului operatiunilor sale si a fl uxurilor de numerar pentru exercitiul incheiat la aceasta data in conformitate cu Standardele Internationale de Raportare Financiara adoptate de Uniunea Europeana.

EVIDENTIEREA UNOR ASPECTE

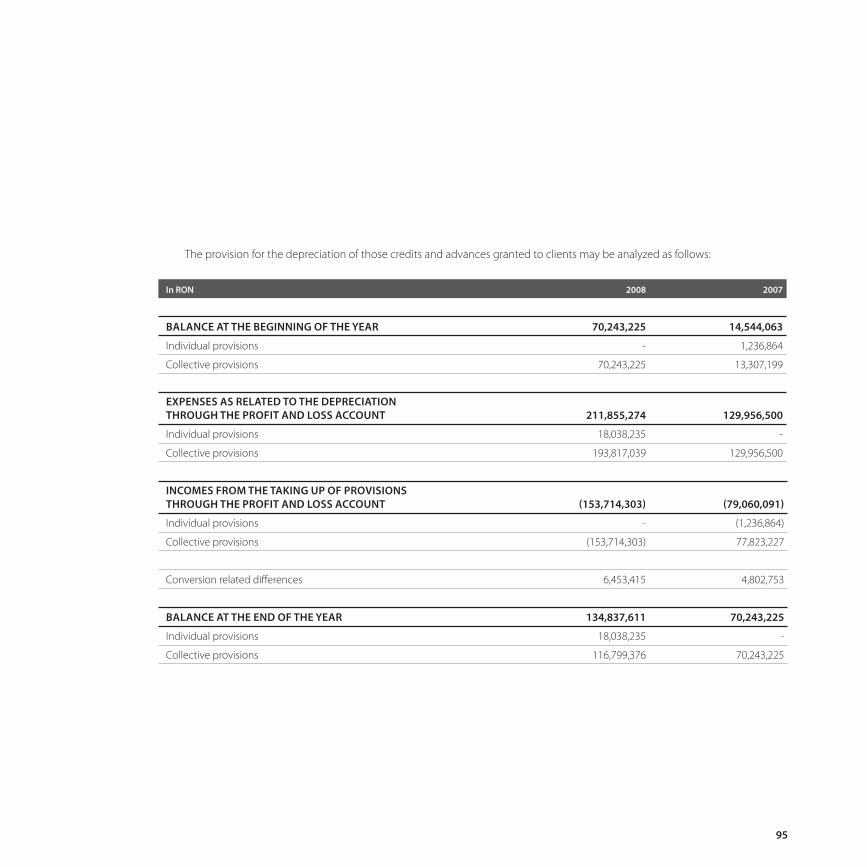

Fara a ne exprima opinia cu rezerve, atragem atentia asupra faptului ca Grupul a estimat provizionul pentru deprecierea valorii creditelor si avansurilor acordate clientilor in baza metodologiei dezvoltata intern si aplicata la 31 decembrie 2008, conform celor prezentate in Nota 3.9.1. - 7.). Datorita limitarilor prezentate in aeeasta nota cu privire la gestiunea informatica a unor aspecte importante ale metodologiei de estimare a fl uxurilor viitoare de numerar din credite si avansuri acordate clientilor, precum si a incertitudinii de pe pietele fi nanciare internationale si locale referitoare la evaluarea activelor mentionate in Nota 4h la situatiile fi nanciare consolidate, aceasta estimare ar putea fi revizuita in mod semnifi cativ ulterior datei la care au fost aprobate situatiile fi nanciare consolidate.

ALTE ASPECTE

Acest raport este adresat exclusiv actionarilor Bancii in ansamblu. Auditul nostru a fost efectuat pentru a putea raporta actionarilor Bancii acele aspecte pe care trebuie sa le raportam intr-un raport de audit fi nanciar, si nu in alte scopuri. In masura permisa de lege, nu acceptam si nu ne asumam responsabilitatea decat fata de Banca si de actionarii acesteia, in ansamblu, pentru auditul nostru, pentru acest raport sau pentru opinia formata.

RAPORT DE CONFORMITATE AL RAPORTULUI DIRECTORATULUI CU SITUATIILE FINANCIARE CONSOLIDATE

In concordanta cu Ordinul Guvernatorului Bancii Nationale a Romaniei nr. 5/2005, articolul 175, punctul 2, cu modifi carile si completarile ulterioare, noi am citit Raportul Directoratului atasat situatiilor fi nanciare consolidate ale Volksbank Romania S.A. si fi lialei sale („Grupul“) intocmite in conformitate cu Standardele Internationale de Raportare Financiara adoptate de Uniunea Europeana la si pentru exercitiul incheiat la 31 decembrie 2008. Raportul Directoratului prezentat si numerotat de la pagina 1 la pagina 18 nu face parte din situatiile fi nanciare consolidate ale Grupului. In Raportul Directoratului, noi nu am identifi cat informatii fi nanciare care sa fi e in mod semnifi cativ neconcordante cu informatiile prezentate in situatiile fi nanciare consolidate ale Grupului la 31 decembrie 2008.

Conform cu versiunea originala semnata in limba romana

29

Pentru si in numele KPMG Audit SRL:

Toader Serban-Cristian KPMG Audit SRL

Inregistrat la Camera Auditorilor Financiari Inregistrat la Camera Auditorilor Financiari din Romania cu numarul 1502/2003 din Romania cu numarul 9/2001

Bucuresti, 24 Martie 2009

30

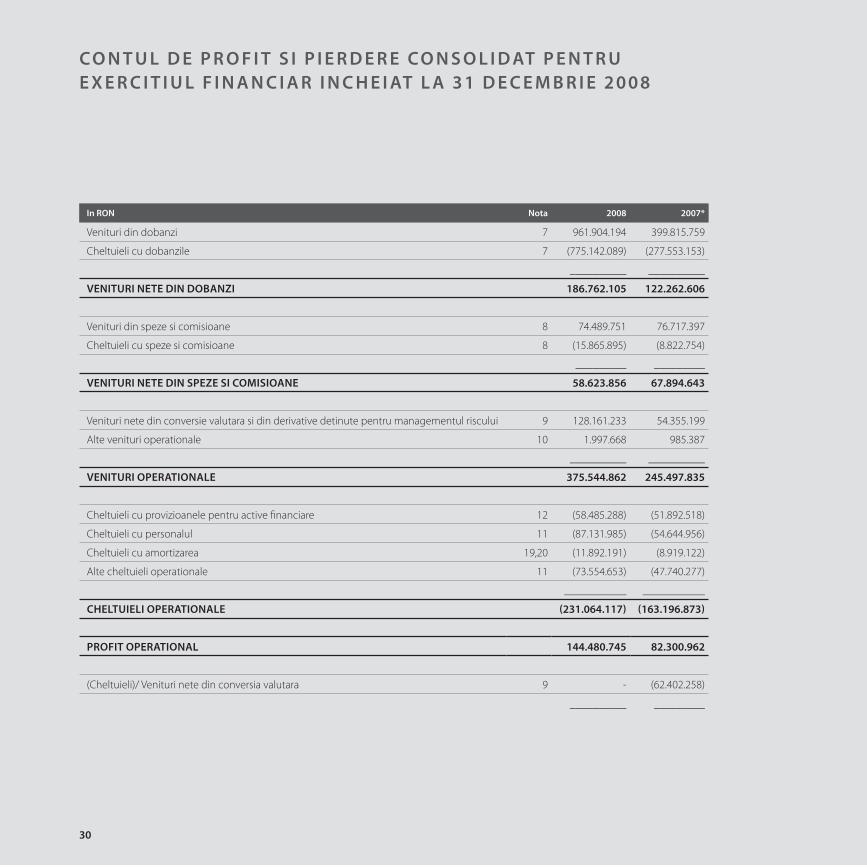

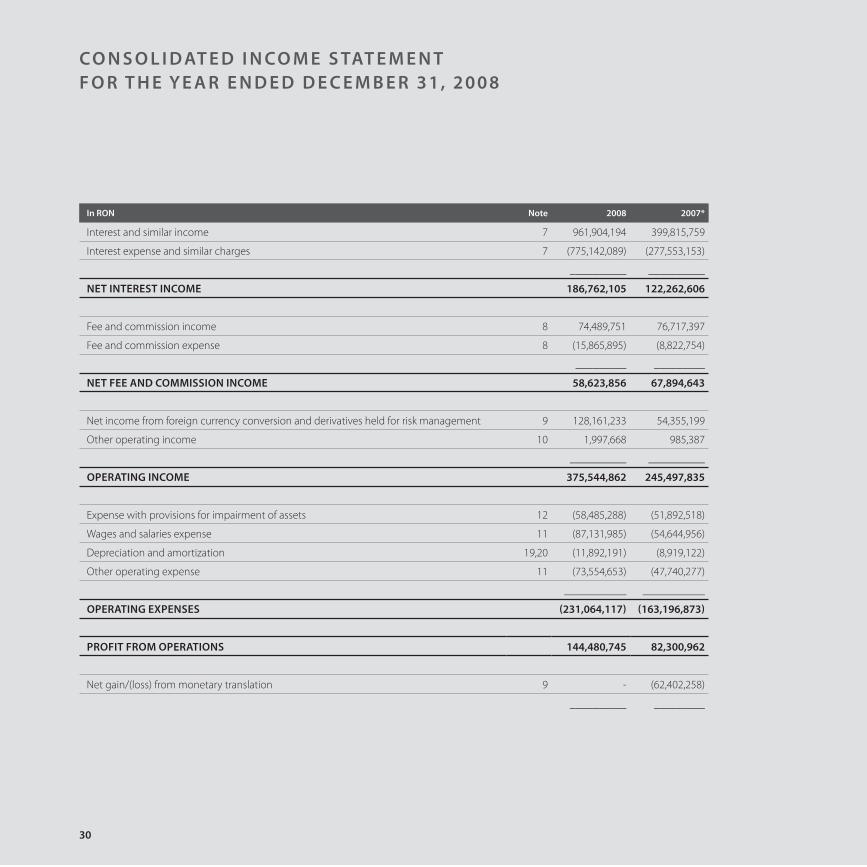

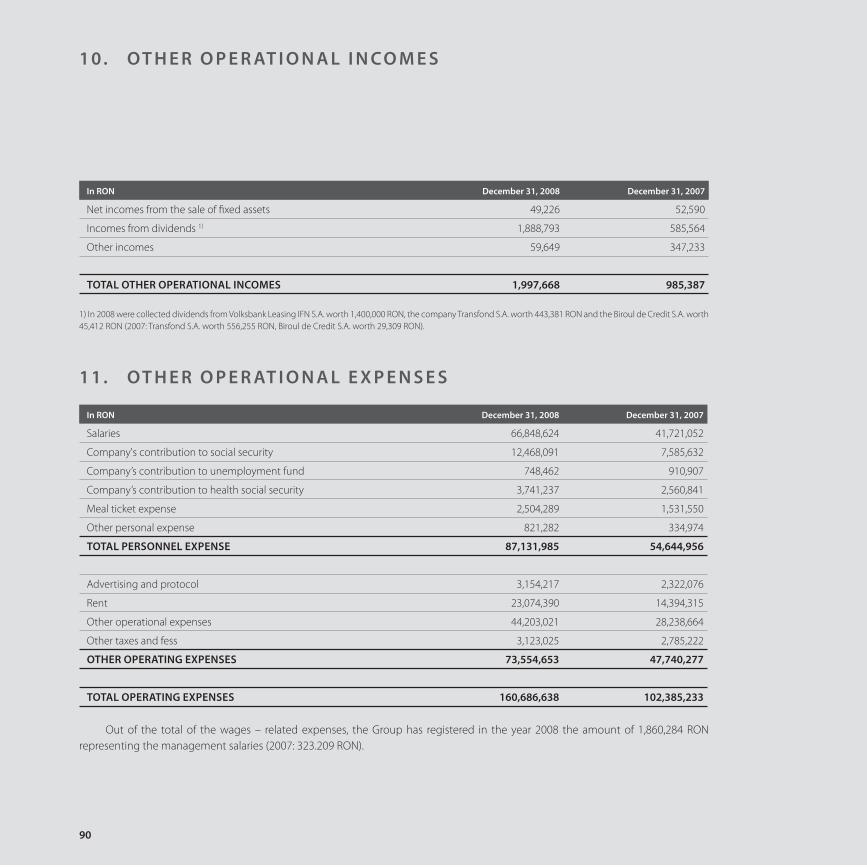

In RON Nota 2008 2007*

Venituri din dobanzi 7 961.904.194 399.815.759

Cheltuieli cu dobanzile 7 (775.142.089) (277.553.153)

__________ __________

VENITURI NETE DIN DOBANZI 186.762.105 122.262.606

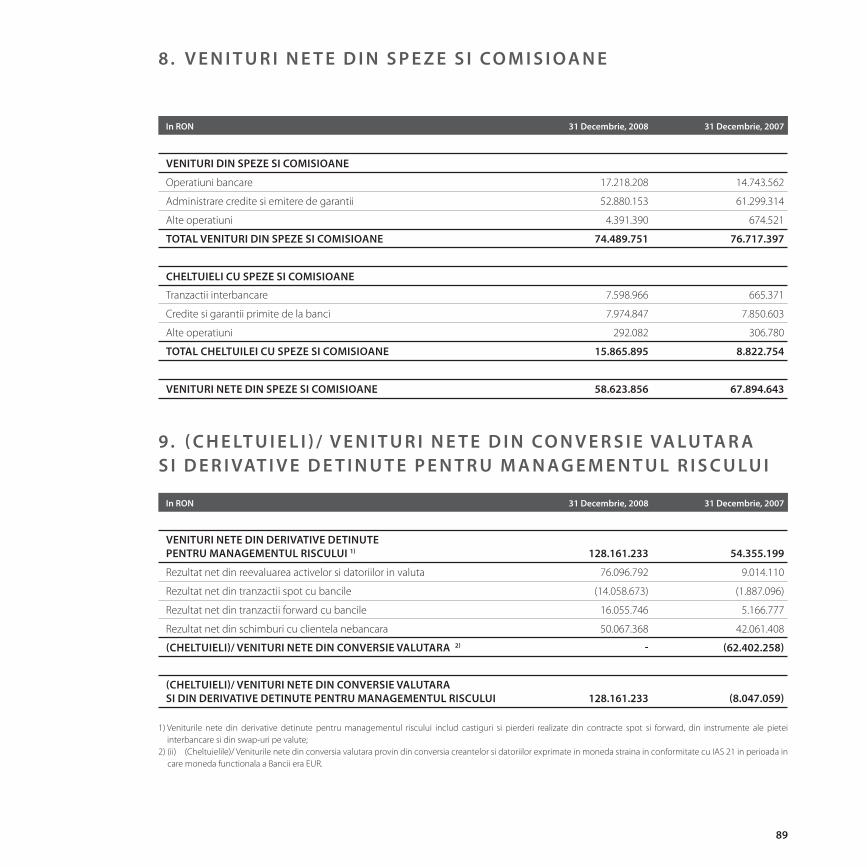

Venituri din speze si comisioane 8 74.489.751 76.717.397

Cheltuieli cu speze si comisioane 8 (15.865.895) (8.822.754)

_________ _________

VENITURI NETE DIN SPEZE SI COMISIOANE 58.623.856 67.894.643

Venituri nete din conversie valutara si din derivative detinute pentru managementul riscului 9 128.161.233 54.355.199

Alte venituri operationale 10 1.997.668 985.387

__________ __________

VENITURI OPERATIONALE 375.544.862 245.497.835

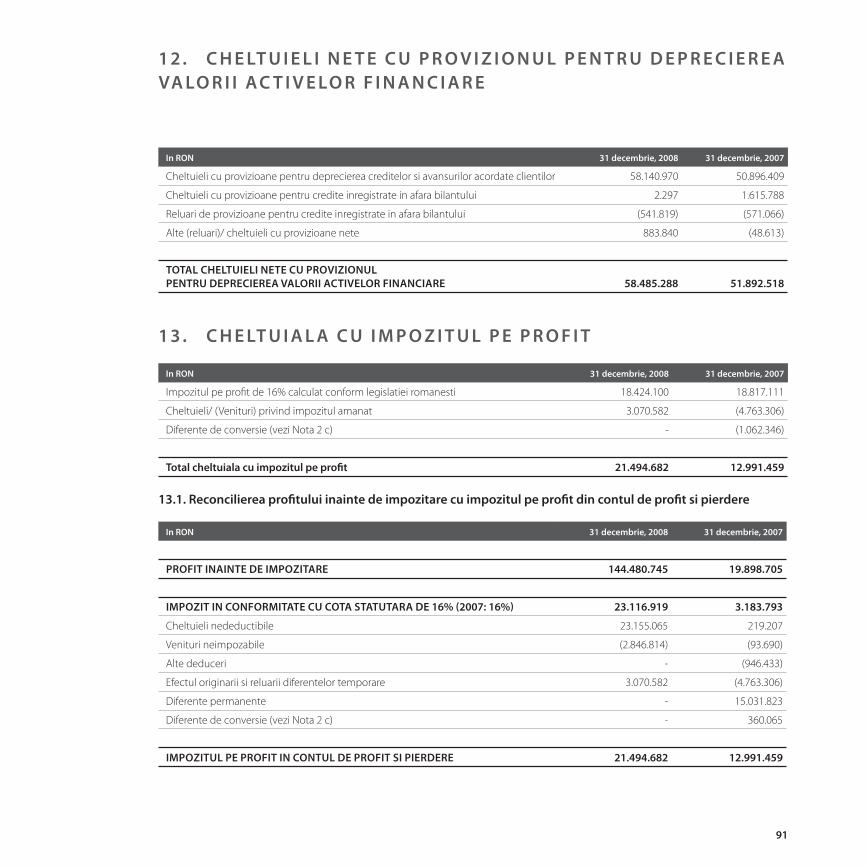

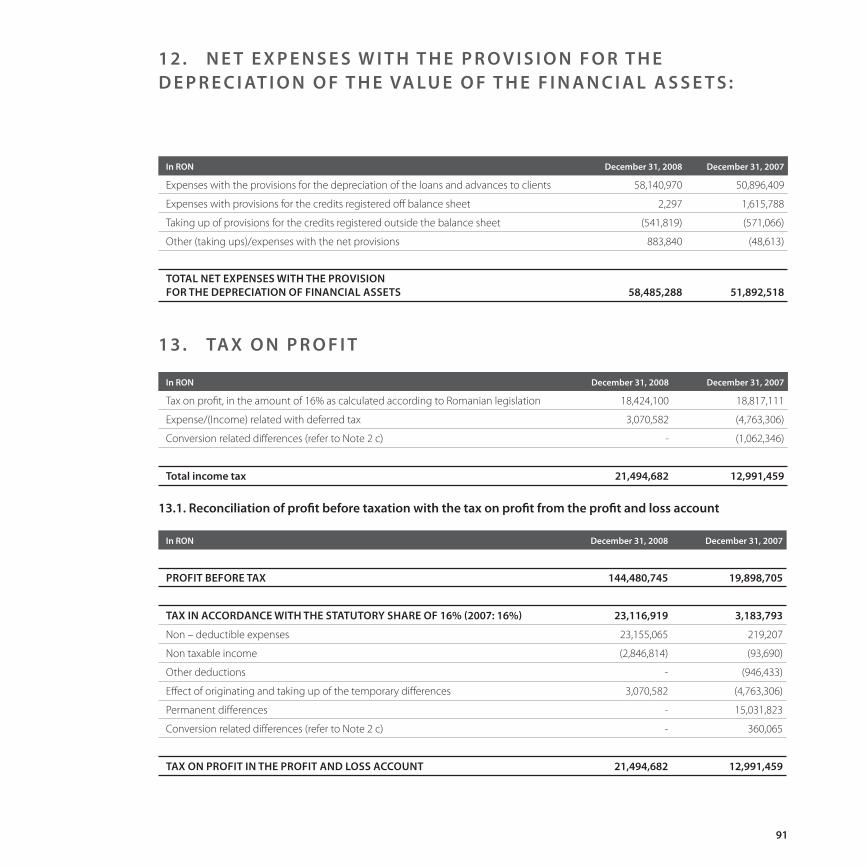

Cheltuieli cu provizioanele pentru active fi nanciare 12 (58.485.288) (51.892.518)

Cheltuieli cu personalul 11 (87.131.985) (54.644.956)

Cheltuieli cu amortizarea 19,20 (11.892.191) (8.919.122)

Alte cheltuieli operationale 11 (73.554.653) (47.740.277)

___________ ___________

CHELTUIELI OPERATIONALE (231.064.117) (163.196.873)

PROFIT OPERATIONAL 144.480.745 82.300.962

(Cheltuieli)/ Venituri nete din conversia valutara 9 - (62.402.258)

__________ _________

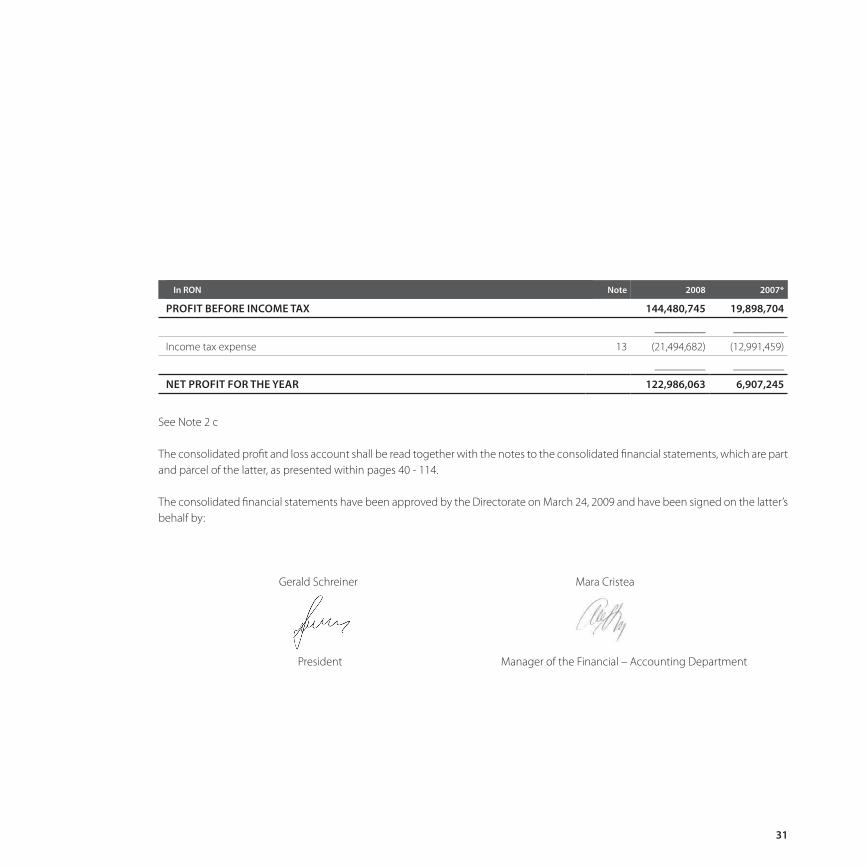

C O N T U L D E P R O F I T S I P I E R D E R E C O N S O L I D AT P E N T R U E X E R C I T I U L F I N A N C I A R I N C H E I AT L A 3 1 D E C E M B R I E 2 0 0 8

31

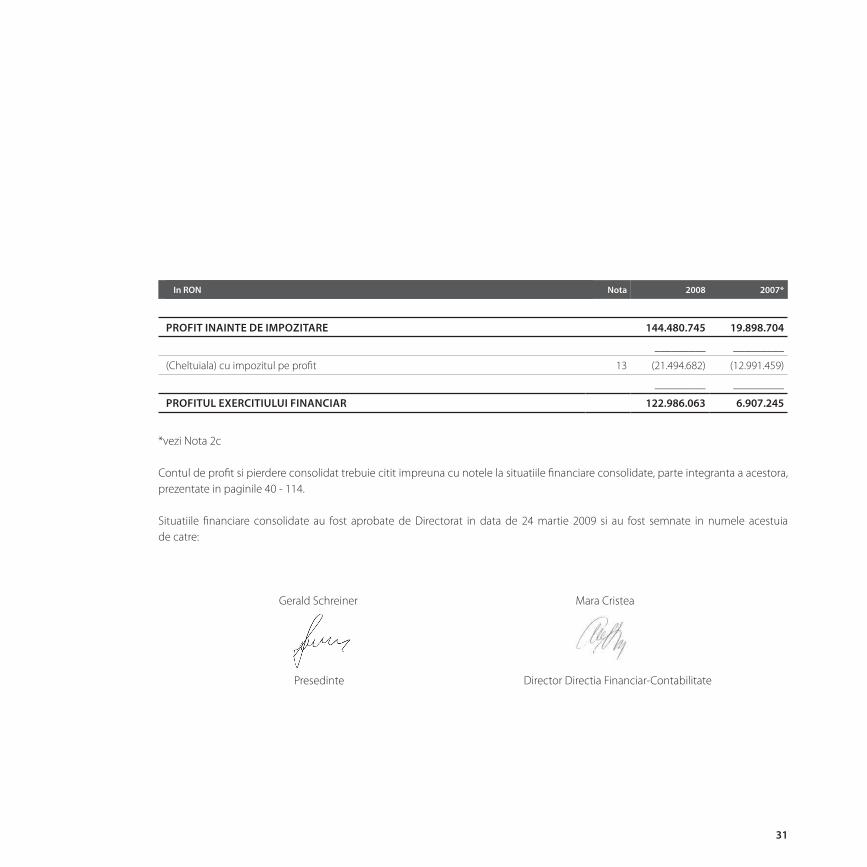

In RON Nota 2008 2007*

PROFIT INAINTE DE IMPOZITARE 144.480.745 19.898.704

_________ _________

(Cheltuiala) cu impozitul pe profi t 13 (21.494.682) (12.991.459)

_________ _________

PROFITUL EXERCITIULUI FINANCIAR 122.986.063 6.907.245

*vezi Nota 2c

Contul de profi t si pierdere consolidat trebuie citit impreuna cu notele la situatiile fi nanciare consolidate, parte integranta a acestora, prezentate in paginile 40 - 114.

Situatiile fi nanciare consolidate au fost aprobate de Directorat in data de 24 martie 2009 si au fost semnate in numele acestuia de catre:

Gerald Schreiner Mara Cristea

Presedinte Director Directia Financiar-Contabilitate

32

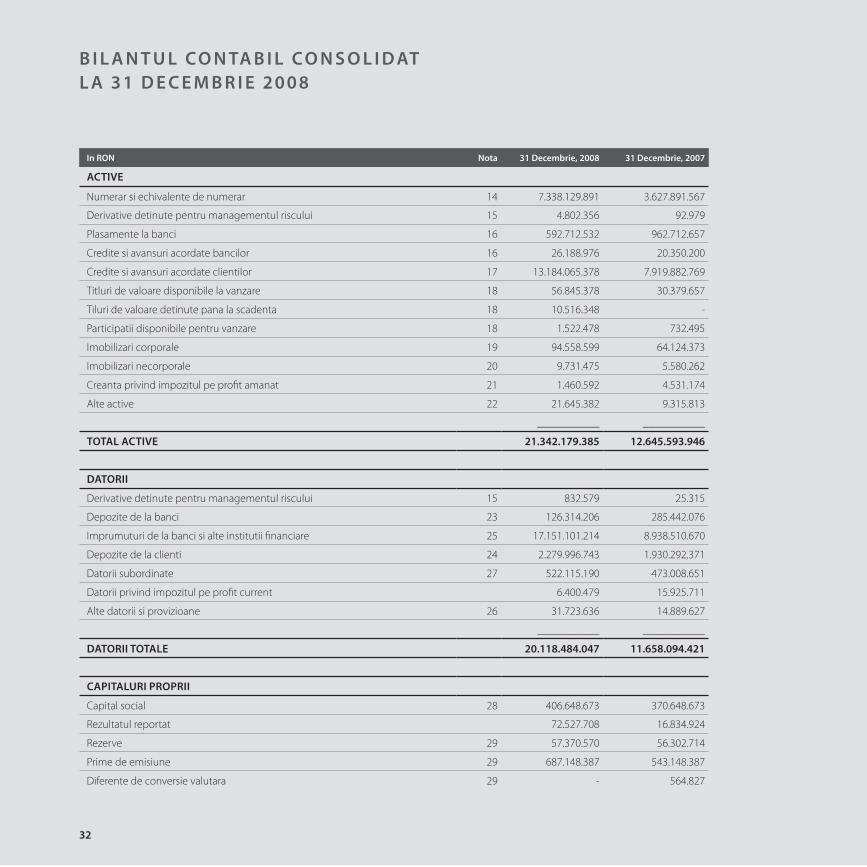

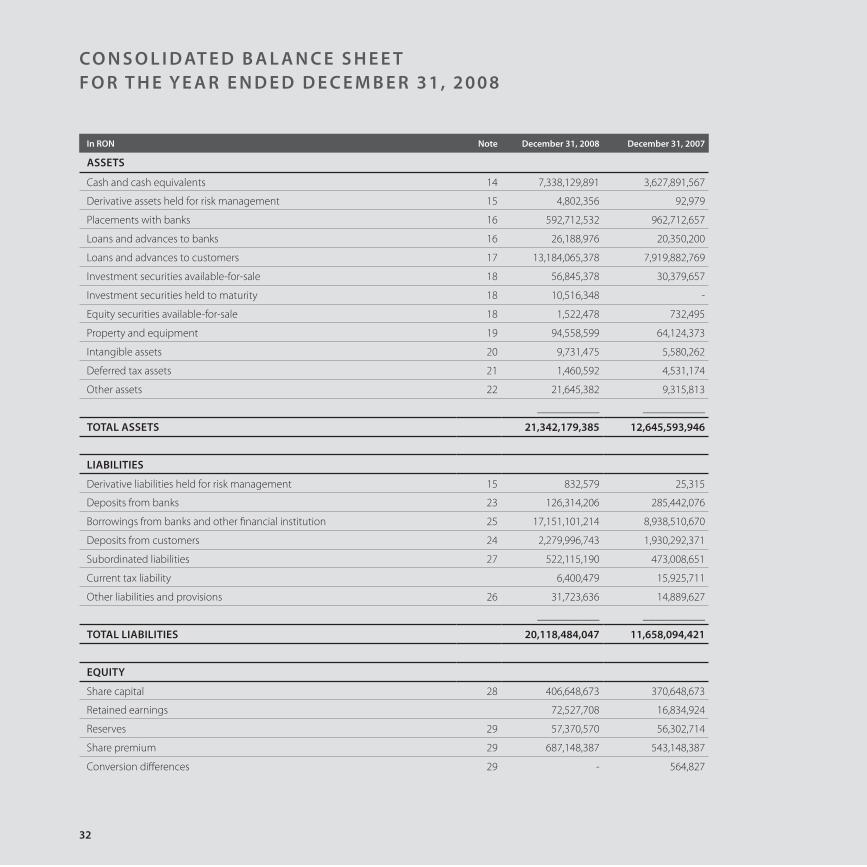

In RON Nota 31 Decembrie, 2008 31 Decembrie, 2007

ACTIVE

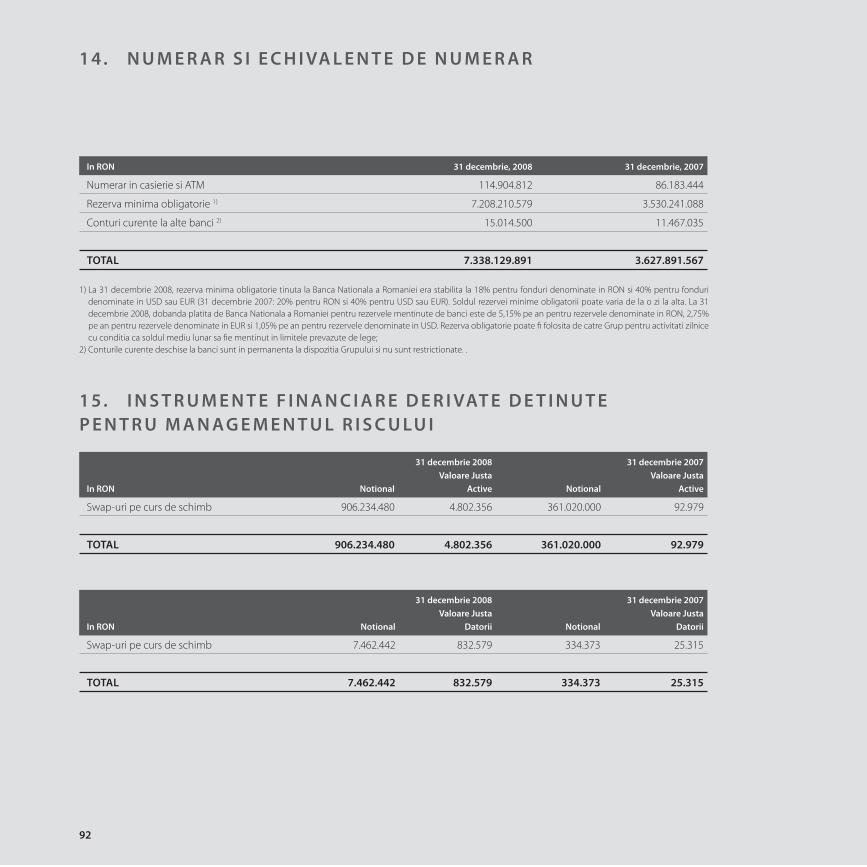

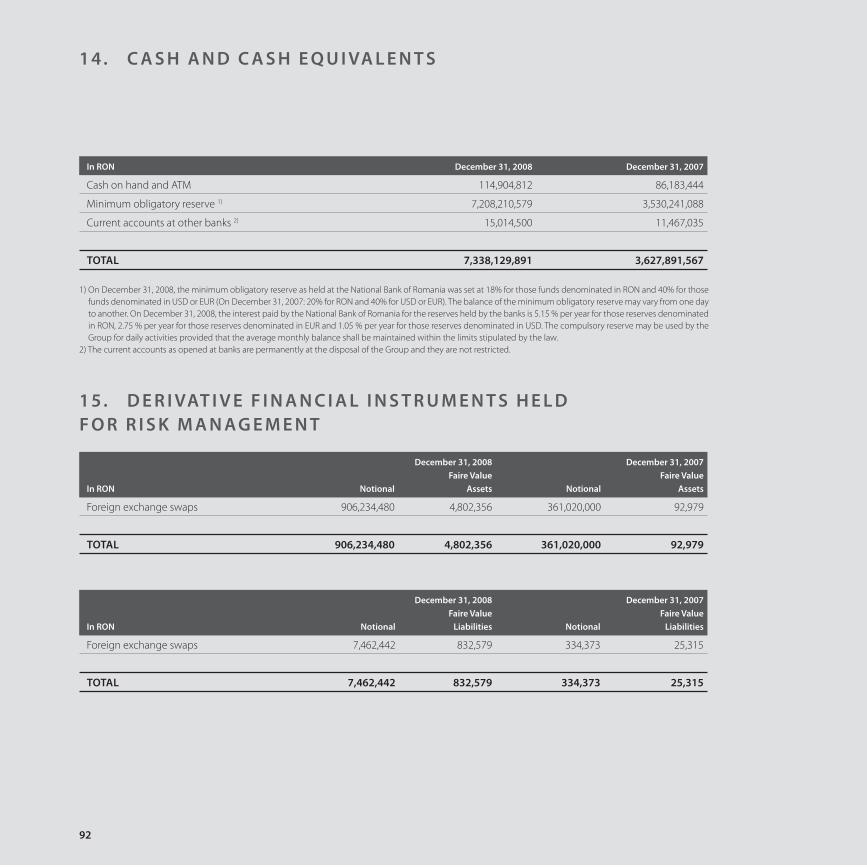

Numerar si echivalente de numerar 14 7.338.129.891 3.627.891.567

Derivative detinute pentru managementul riscului 15 4.802.356 92.979

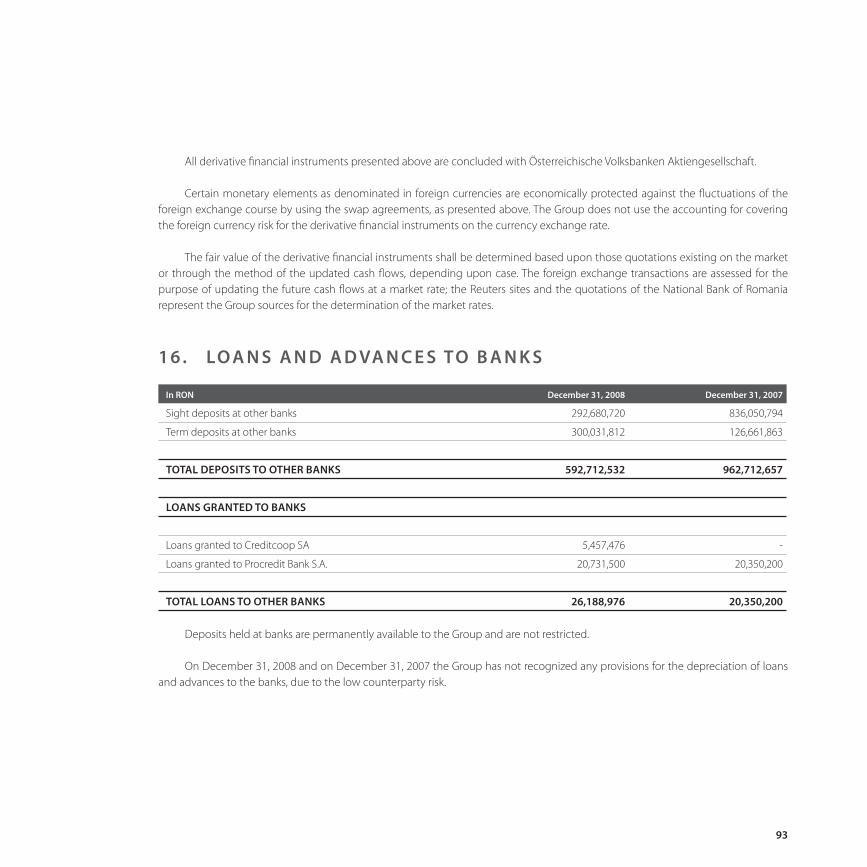

Plasamente la banci 16 592.712.532 962.712.657

Credite si avansuri acordate bancilor 16 26.188.976 20.350.200

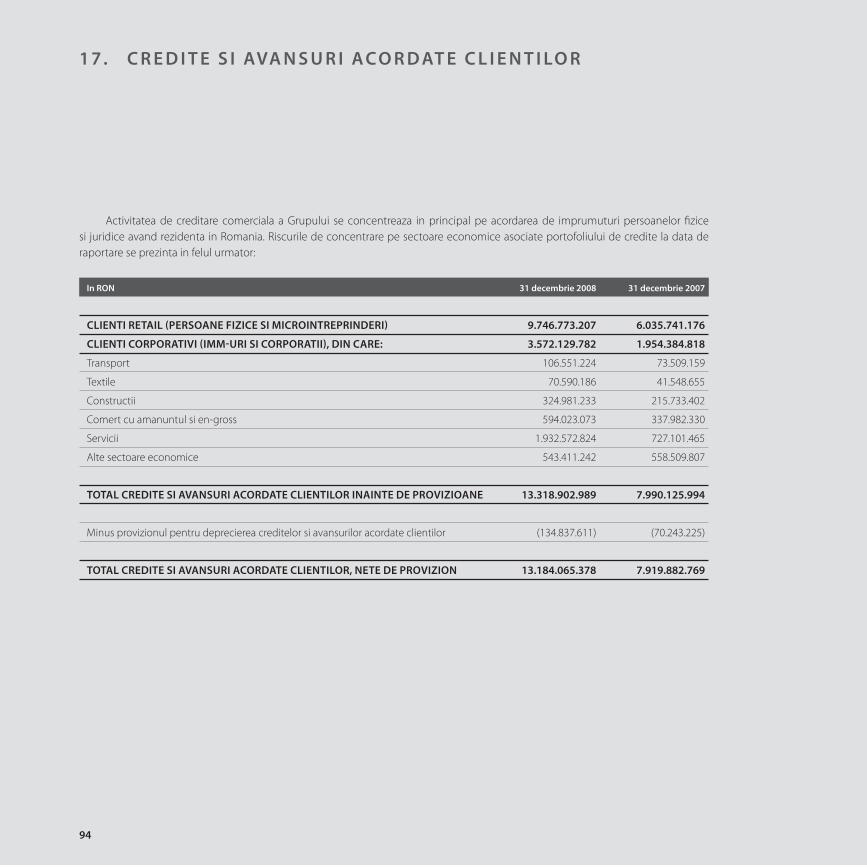

Credite si avansuri acordate clientilor 17 13.184.065.378 7.919.882.769

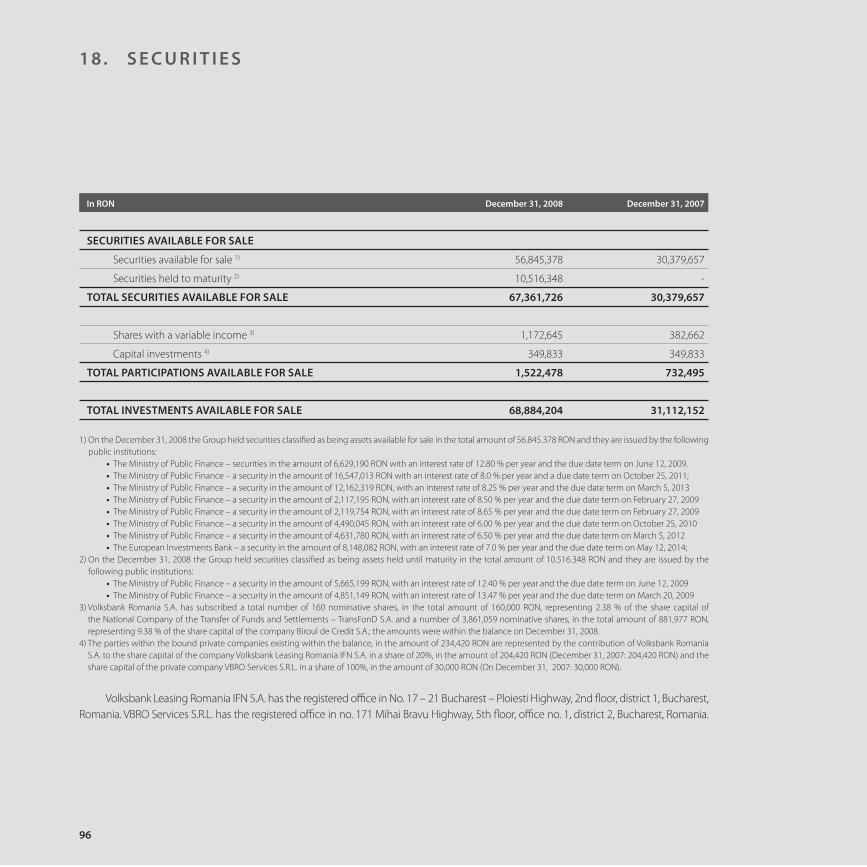

Titluri de valoare disponibile la vanzare 18 56.845.378 30.379.657

Tiluri de valoare detinute pana la scadenta 18 10.516.348 -

Participatii disponibile pentru vanzare 18 1.522.478 732.495

Imobilizari corporale 19 94.558.599 64.124.373

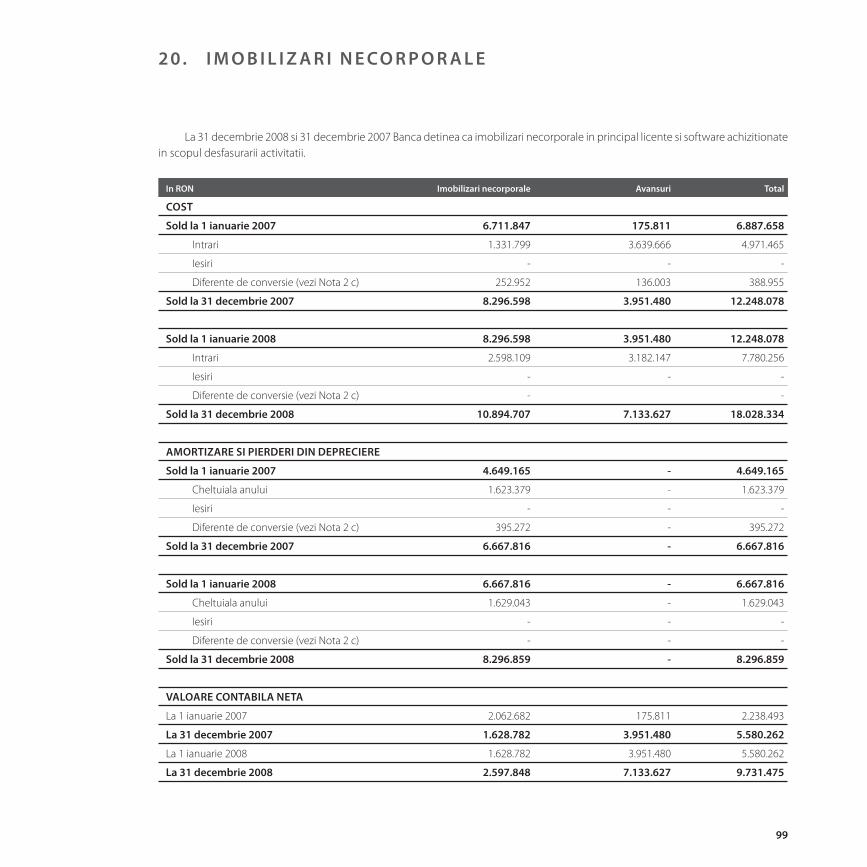

Imobilizari necorporale 20 9.731.475 5.580.262

Creanta privind impozitul pe profi t amanat 21 1.460.592 4.531.174

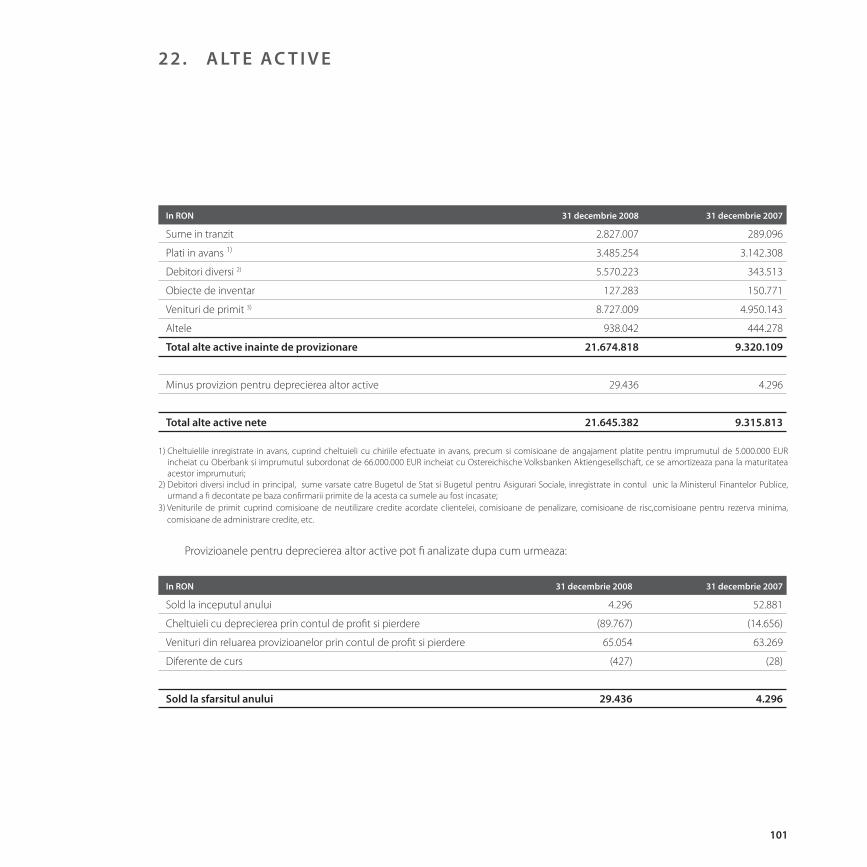

Alte active 22 21.645.382 9.315.813

___________ ___________

TOTAL ACTIVE 21.342.179.385 12.645.593.946

DATORII

Derivative detinute pentru managementul riscului 15 832.579 25.315

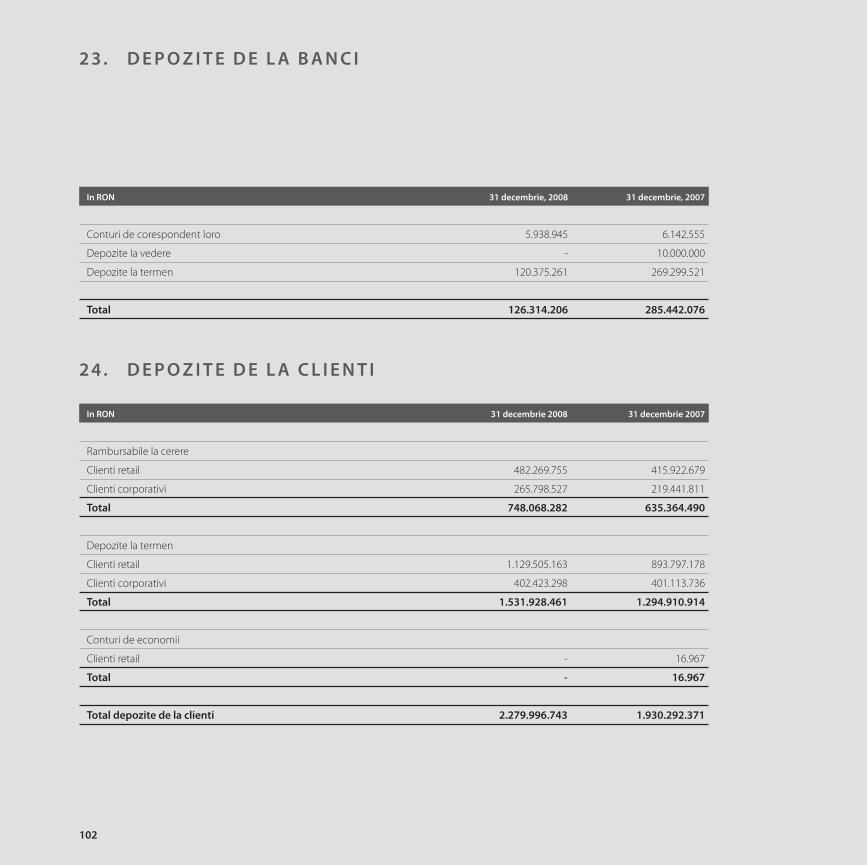

Depozite de la banci 23 126.314.206 285.442.076

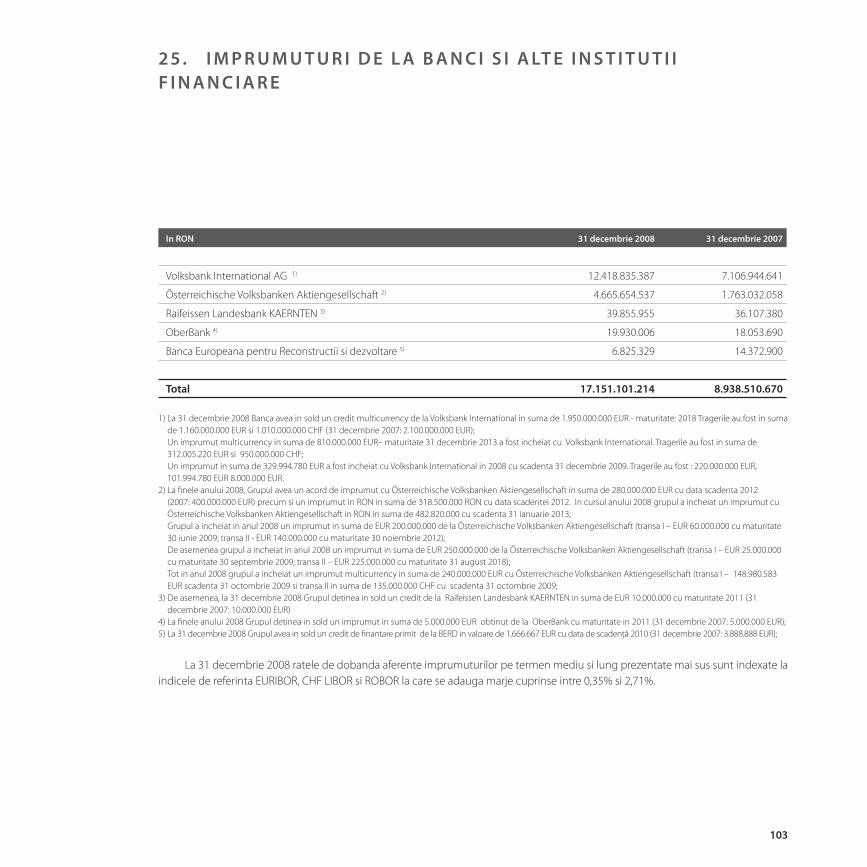

Imprumuturi de la banci si alte institutii fi nanciare 25 17.151.101.214 8.938.510.670

Depozite de la clienti 24 2.279.996.743 1.930.292.371

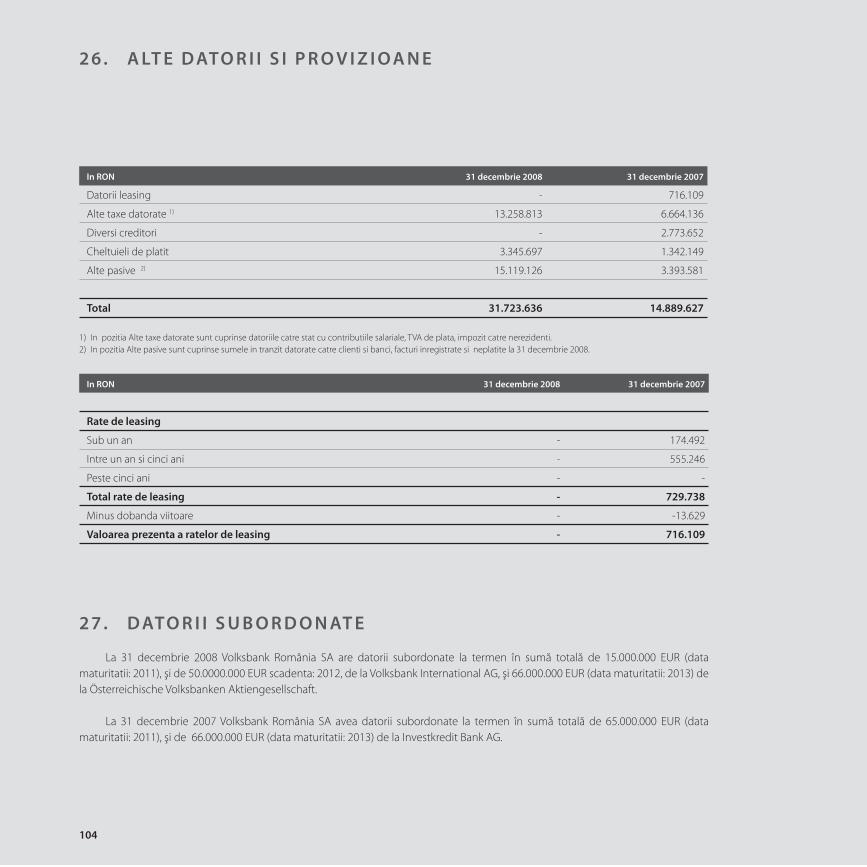

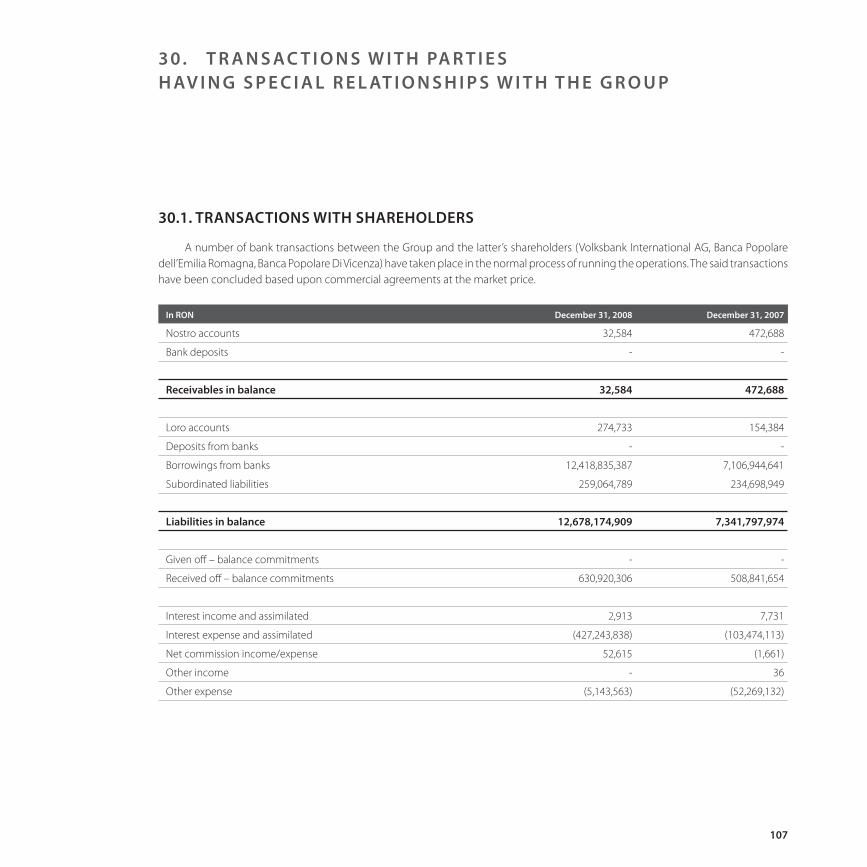

Datorii subordinate 27 522.115.190 473.008.651

Datorii privind impozitul pe profi t current 6.400.479 15.925.711

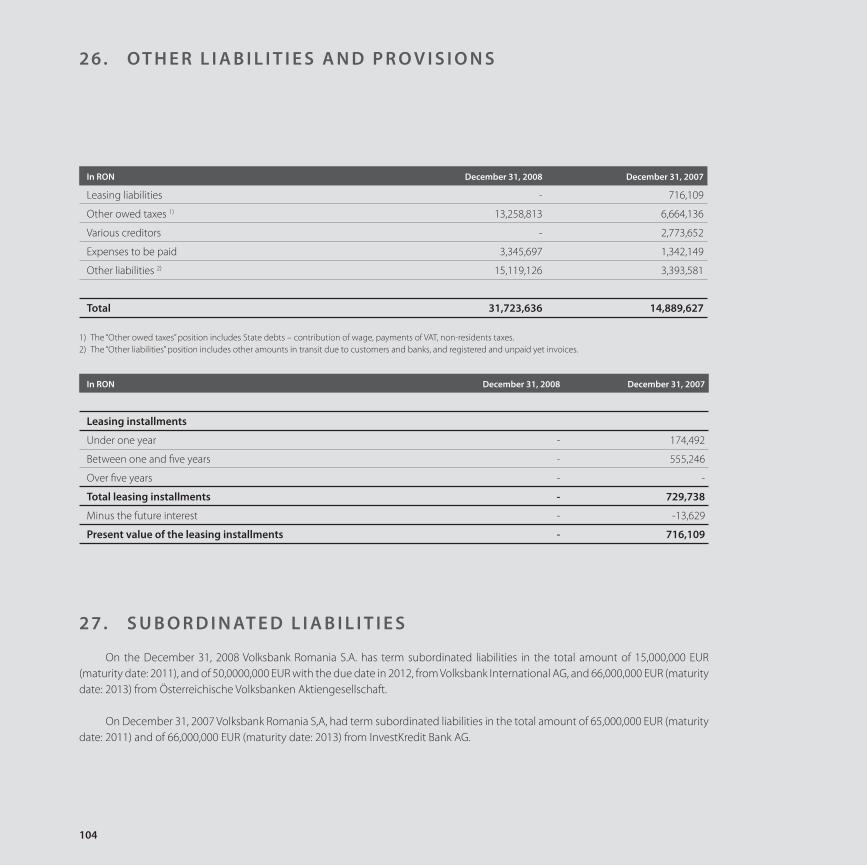

Alte datorii si provizioane 26 31.723.636 14.889.627

___________ ___________

DATORII TOTALE 20.118.484.047 11.658.094.421

CAPITALURI PROPRII

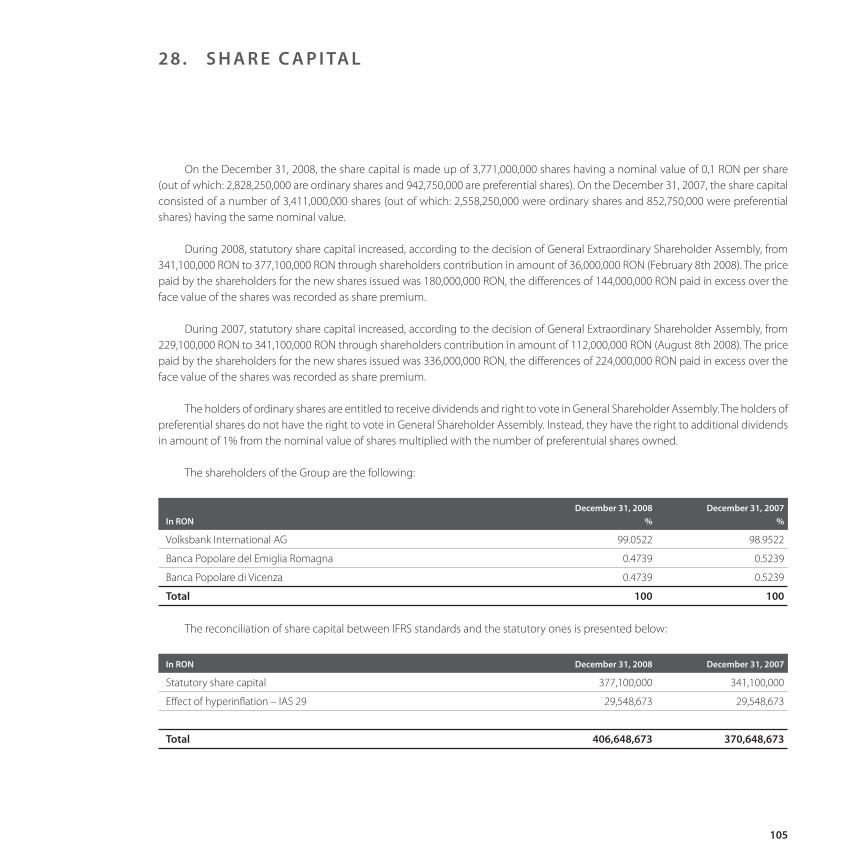

Capital social 28 406.648.673 370.648.673

Rezultatul reportat 72.527.708 16.834.924

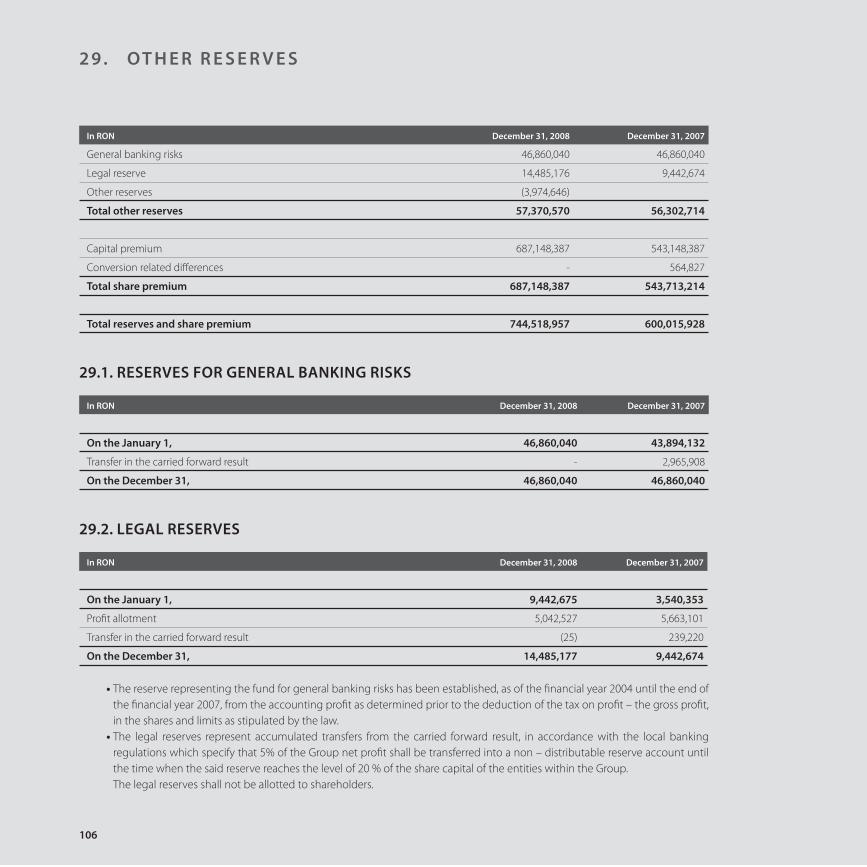

Rezerve 29 57.370.570 56.302.714

Prime de emisiune 29 687.148.387 543.148.387

Diferente de conversie valutara 29 - 564.827

B I L A N T U L C O N TA B I L C O N S O L I D AT L A 3 1 D E C E M B R I E 2 0 0 8

33

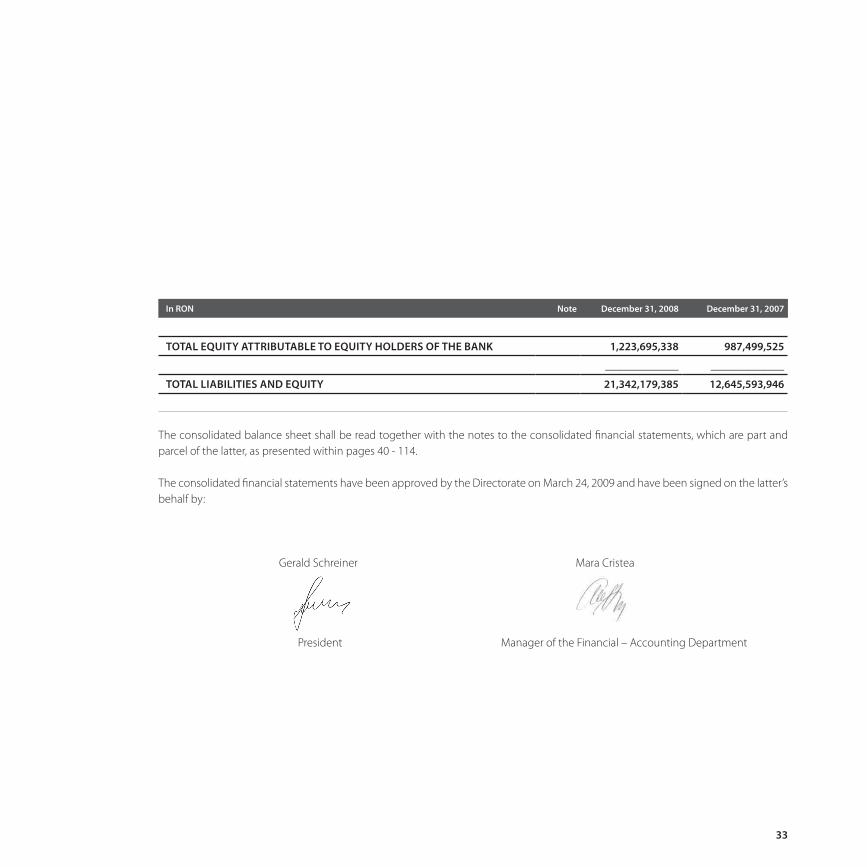

In RON Nota 31 Decembrie, 2008 31 Decembrie, 2007

TOTAL CAPITALURI PROPRII 1.223.695.338 987.499.525

_____________ _____________

TOTAL DATORII SI CAPITALURI PROPRII 21.342.179.385 12.645.593.946

*vezi Nota 2c

Bilantul contabil consolidat trebuie citit impreuna cu notele la situatiile fi nanciare consolidate, parte integranta a acestora, prezentate in paginile 40 - 114.

Situatiile fi nanciare consolidate au fost aprobate de Directorat in data de 24 martie 2009 si au fost semnate in numele acestuia de catre:

Gerald Schreiner Mara Cristea

Presedinte Director Directia Financiar-Contabilitate

34

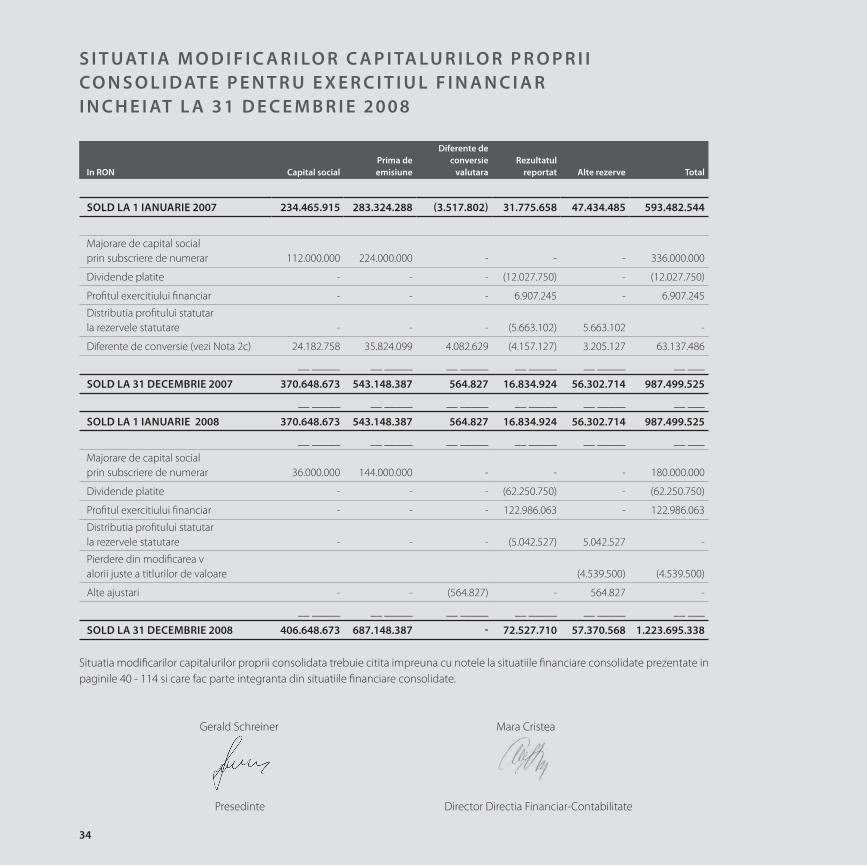

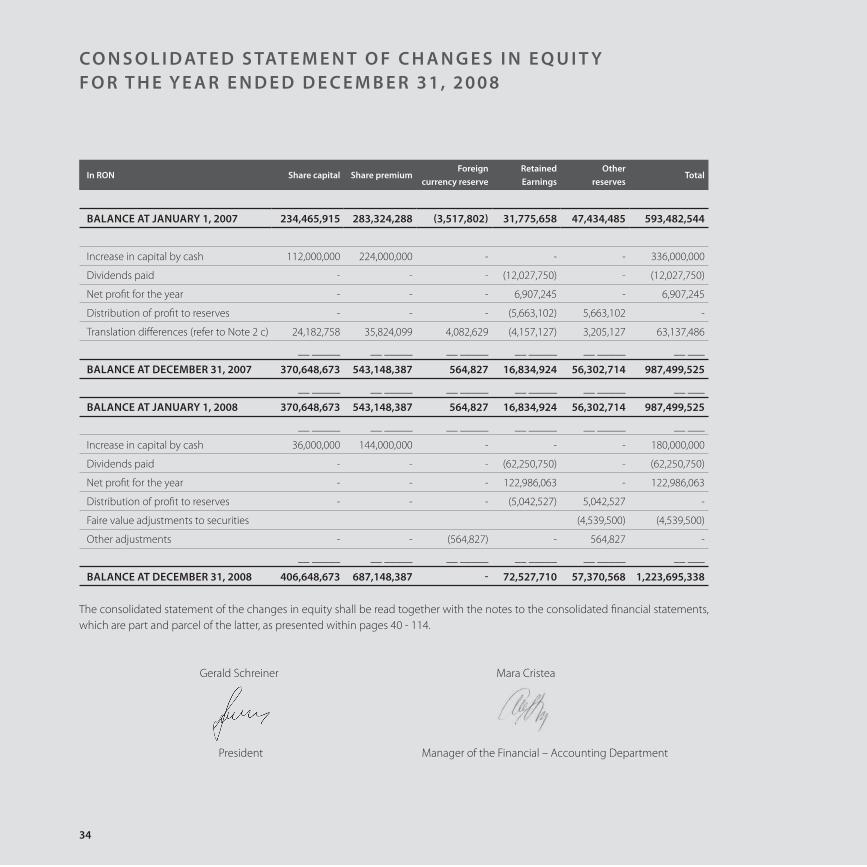

In RON Capital socialPrima de emisiune

Diferente de conversie

valutaraRezultatul

reportat Alte rezerve Total

SOLD LA 1 IANUARIE 2007 234.465.915 283.324.288 (3.517.802) 31.775.658 47.434.485 593.482.544

Majorare de capital social prin subscriere de numerar 112.000.000 224.000.000 - - - 336.000.000

Dividende platite - - - (12.027.750) - (12.027.750)

Profi tul exercitiului fi nanciar - - - 6.907.245 - 6.907.245

Distributia profi tului statutar la rezervele statutare - - - (5.663.102) 5.663.102 -

Diferente de conversie (vezi Nota 2c) 24.182.758 35.824.099 4.082.629 (4.157.127) 3.205.127 63.137.486

__ _____ __ _____ __ _____ __ _____ __ _____ __ ___

SOLD LA 31 DECEMBRIE 2007 370.648.673 543.148.387 564.827 16.834.924 56.302.714 987.499.525

__ _____ __ _____ __ _____ __ _____ __ _____ __ ___

SOLD LA 1 IANUARIE 2008 370.648.673 543.148.387 564.827 16.834.924 56.302.714 987.499.525

__ _____ __ _____ __ _____ __ _____ __ _____ __ ___

Majorare de capital social prin subscriere de numerar 36.000.000 144.000.000 - - - 180.000.000

Dividende platite - - - (62.250.750) - (62.250.750)

Profi tul exercitiului fi nanciar - - - 122.986.063 - 122.986.063

Distributia profi tului statutar la rezervele statutare - - - (5.042.527) 5.042.527 -

Pierdere din modifi carea valorii juste a titlurilor de valoare (4.539.500) (4.539.500)

Alte ajustari - - (564.827) - 564.827 -

__ _____ __ _____ __ _____ __ _____ __ _____ __ ___

SOLD LA 31 DECEMBRIE 2008 406.648.673 687.148.387 - 72.527.710 57.370.568 1.223.695.338

Situatia modifi carilor capitalurilor proprii consolidata trebuie citita impreuna cu notele la situatiile fi nanciare consolidate prezentate in paginile 40 - 114 si care fac parte integranta din situatiile fi nanciare consolidate.

Gerald Schreiner Mara Cristea

Presedinte Director Directia Financiar-Contabilitate

S I T UAT I A M O D I F I C A R I LO R C A P I TA LU R I LO R P R O P R I I C O N S O L I D AT E P E N T R U E X E R C I T I U L F I N A N C I A R I N C H E I AT L A 3 1 D E C E M B R I E 2 0 0 8

35

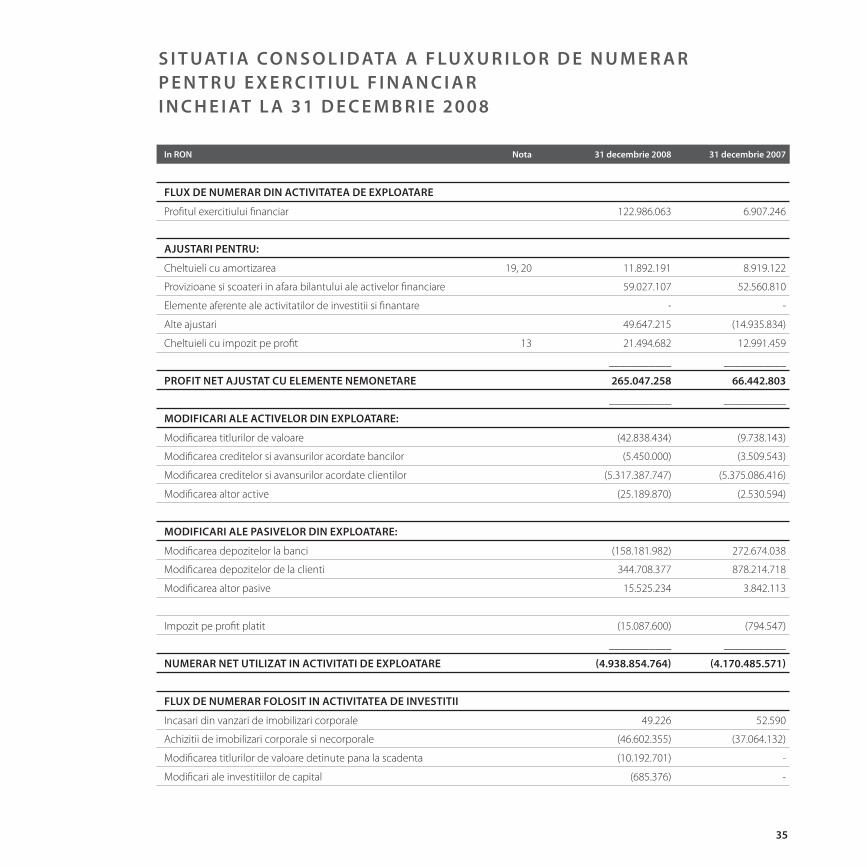

In RON Nota 31 decembrie 2008 31 decembrie 2007

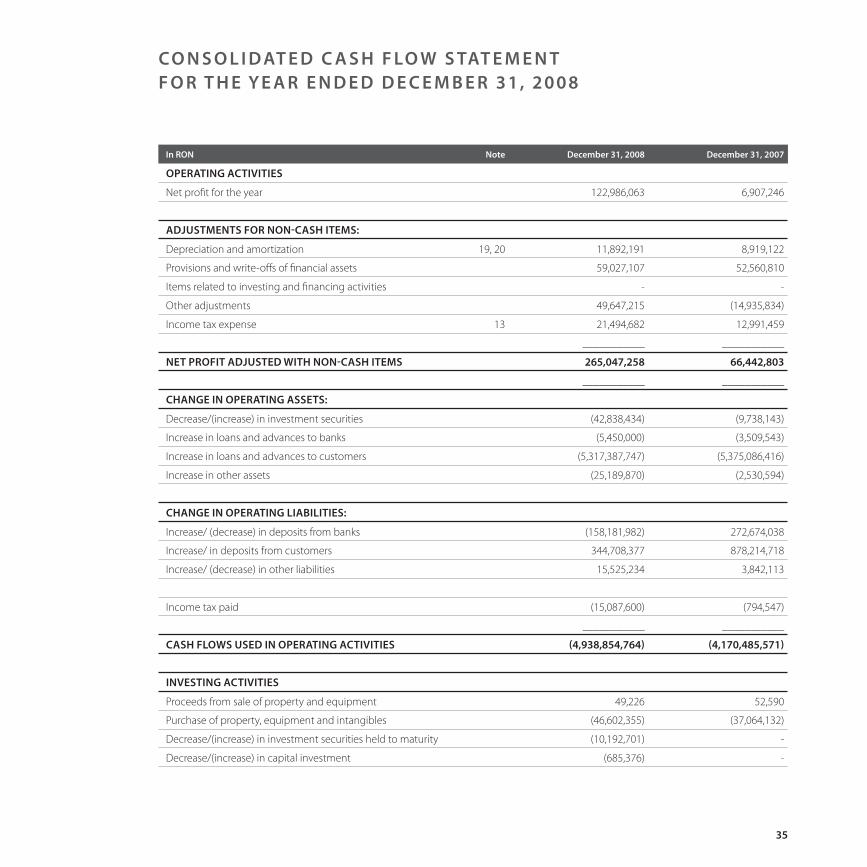

FLUX DE NUMERAR DIN ACTIVITATEA DE EXPLOATARE

Profi tul exercitiului fi nanciar 122.986.063 6.907.246

AJUSTARI PENTRU:

Cheltuieli cu amortizarea 19, 20 11.892.191 8.919.122

Provizioane si scoateri in afara bilantului ale activelor fi nanciare 59.027.107 52.560.810

Elemente aferente ale activitatilor de investitii si fi nantare - -

Alte ajustari 49.647.215 (14.935.834)

Cheltuieli cu impozit pe profi t 13 21.494.682 12.991.459

___________ ___________

PROFIT NET AJUSTAT CU ELEMENTE NEMONETARE 265.047.258 66.442.803

___________ ___________

MODIFICARI ALE ACTIVELOR DIN EXPLOATARE:

Modifi carea titlurilor de valoare (42.838.434) (9.738.143)

Modifi carea creditelor si avansurilor acordate bancilor (5.450.000) (3.509.543)

Modifi carea creditelor si avansurilor acordate clientilor (5.317.387.747) (5.375.086.416)

Modifi carea altor active (25.189.870) (2.530.594)

MODIFICARI ALE PASIVELOR DIN EXPLOATARE:

Modifi carea depozitelor la banci (158.181.982) 272.674.038

Modifi carea depozitelor de la clienti 344.708.377 878.214.718

Modifi carea altor pasive 15.525.234 3.842.113

Impozit pe profi t platit (15.087.600) (794.547)

___________ ___________

NUMERAR NET UTILIZAT IN ACTIVITATI DE EXPLOATARE (4.938.854.764) (4.170.485.571)

FLUX DE NUMERAR FOLOSIT IN ACTIVITATEA DE INVESTITII

Incasari din vanzari de imobilizari corporale 49.226 52.590

Achizitii de imobilizari corporale si necorporale (46.602.355) (37.064.132)

Modifi carea titlurilor de valoare detinute pana la scadenta (10.192.701) -

Modifi cari ale investitiilor de capital (685.376) -

S I T UAT I A C O N S O L I D ATA A F LU X U R I LO R D E N U M E R A RP E N T R U E X E R C I T I U L F I N A N C I A R I N C H E I AT L A 3 1 D E C E M B R I E 2 0 0 8

36

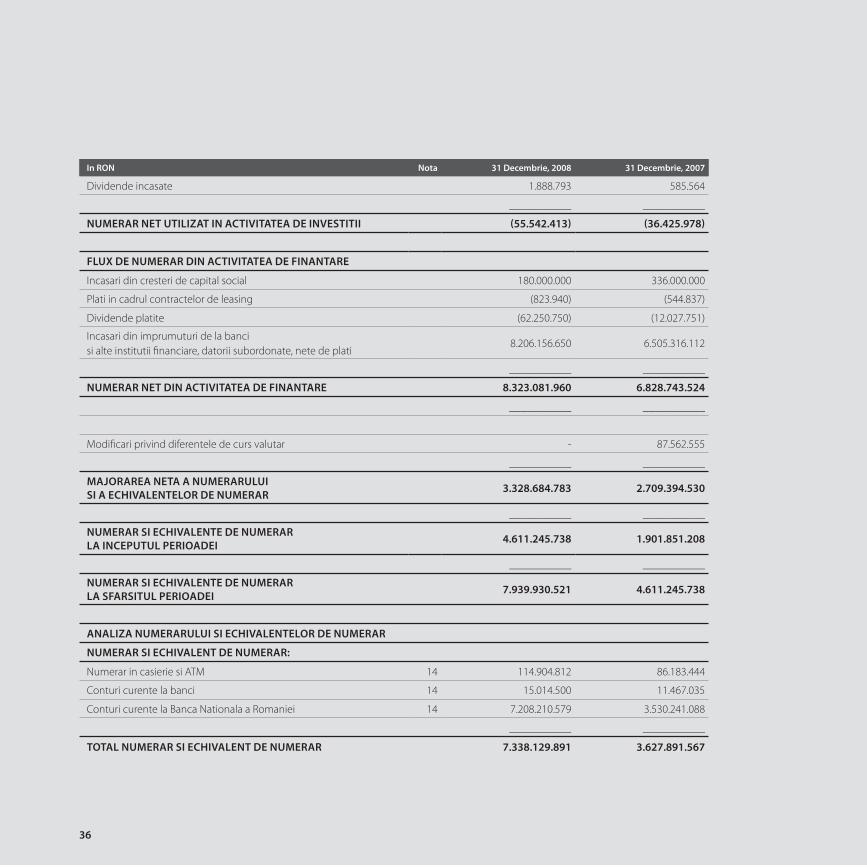

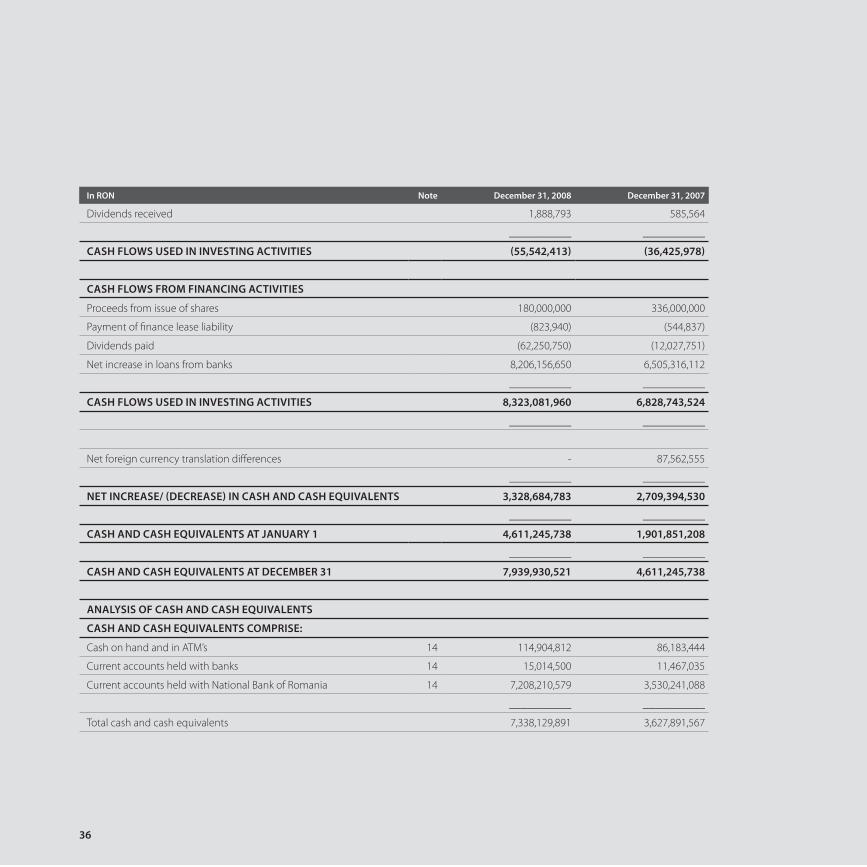

In RON Nota 31 Decembrie, 2008 31 Decembrie, 2007

Dividende incasate 1.888.793 585.564

___________ ___________

NUMERAR NET UTILIZAT IN ACTIVITATEA DE INVESTITII (55.542.413) (36.425.978)

FLUX DE NUMERAR DIN ACTIVITATEA DE FINANTARE

Incasari din cresteri de capital social 180.000.000 336.000.000

Plati in cadrul contractelor de leasing (823.940) (544.837)

Dividende platite (62.250.750) (12.027.751)

Incasari din imprumuturi de la banci si alte institutii fi nanciare, datorii subordonate, nete de plati

8.206.156.650 6.505.316.112

___________ ___________

NUMERAR NET DIN ACTIVITATEA DE FINANTARE 8.323.081.960 6.828.743.524

___________ ___________

Modifi cari privind diferentele de curs valutar - 87.562.555

___________ ___________

MAJORAREA NETA A NUMERARULUI SI A ECHIVALENTELOR DE NUMERAR 3.328.684.783 2.709.394.530

___________ ___________

NUMERAR SI ECHIVALENTE DE NUMERAR LA INCEPUTUL PERIOADEI 4.611.245.738 1.901.851.208

___________ ___________

NUMERAR SI ECHIVALENTE DE NUMERAR LA SFARSITUL PERIOADEI 7.939.930.521 4.611.245.738

ANALIZA NUMERARULUI SI ECHIVALENTELOR DE NUMERAR

NUMERAR SI ECHIVALENT DE NUMERAR:

Numerar in casierie si ATM 14 114.904.812 86.183.444

Conturi curente la banci 14 15.014.500 11.467.035

Conturi curente la Banca Nationala a Romaniei 14 7.208.210.579 3.530.241.088

___________ ___________

TOTAL NUMERAR SI ECHIVALENT DE NUMERAR 7.338.129.891 3.627.891.567

37

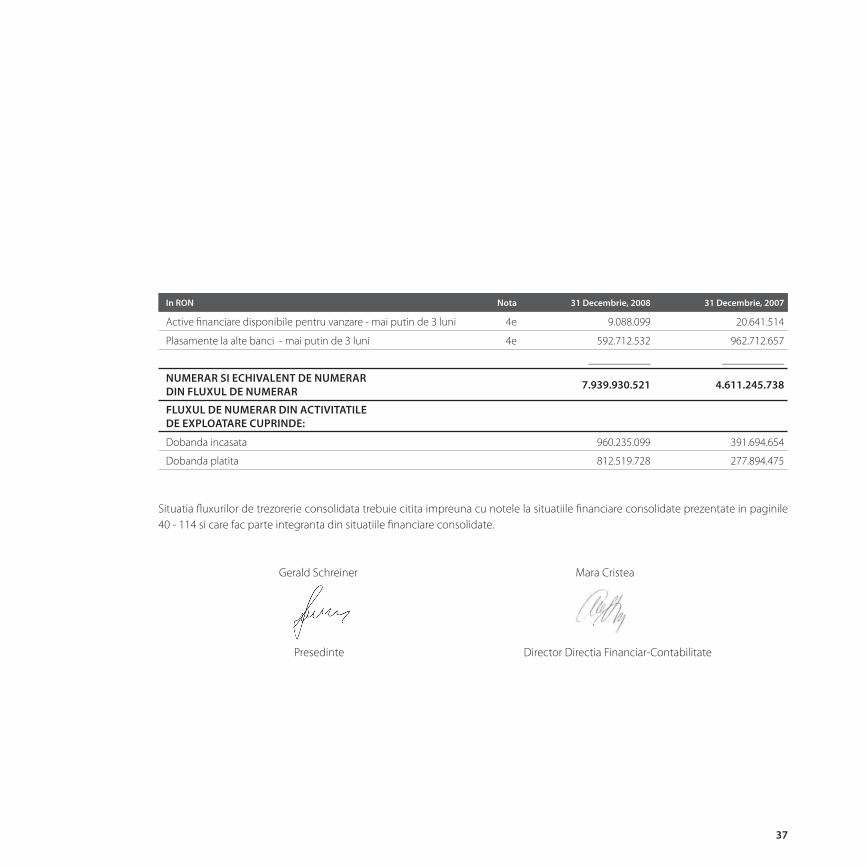

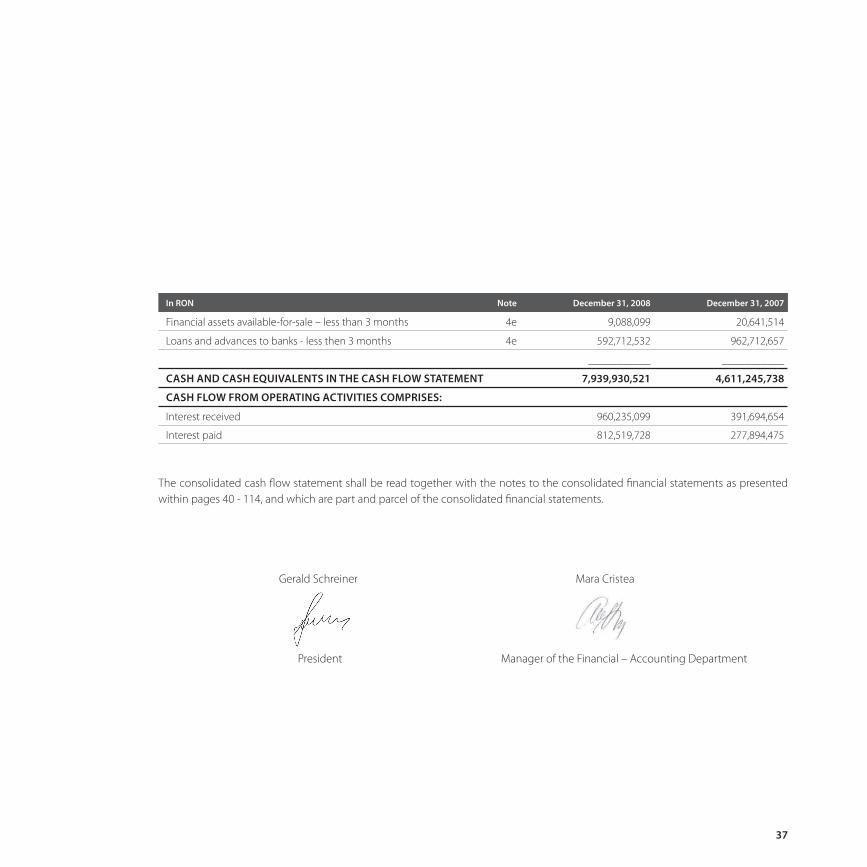

In RON Nota 31 Decembrie, 2008 31 Decembrie, 2007

Active fi nanciare disponibile pentru vanzare - mai putin de 3 luni 4e 9.088.099 20.641.514

Plasamente la alte banci - mai putin de 3 luni 4e 592.712.532 962.712.657

___________ ___________

NUMERAR SI ECHIVALENT DE NUMERAR DIN FLUXUL DE NUMERAR 7.939.930.521 4.611.245.738

FLUXUL DE NUMERAR DIN ACTIVITATILE DE EXPLOATARE CUPRINDE:

Dobanda incasata 960.235.099 391.694.654

Dobanda platita 812.519.728 277.894.475

Situatia fl uxurilor de trezorerie consolidata trebuie citita impreuna cu notele la situatiile fi nanciare consolidate prezentate in paginile 40 - 114 si care fac parte integranta din situatiile fi nanciare consolidate.

Gerald Schreiner Mara Cristea

Presedinte Director Directia Financiar-Contabilitate

38

39

VolksbankRomania S.A.

Note la situatiile financiare consolidate

40

Grupul Volksbank Romania („Grupul”) cuprinde banca-mama, Volksbank Romania S.A. („Banca”) si fi liala acesteia cu sediul in Romania. Situatiile fi nanciare consolidate ale Grupului pentru exercitiul fi nanciar incheiat la 31 decembrie 2008 sunt formate din situatiile fi nanciare ale Volksbank Romania S.A. si ale fi lialei sale VBRO Services S.R.L., care impreuna formeaza Grupul. Banca detine o participatie de 100% din capitalul social al VBRO Services S.R.L., care a fost dobandita in 2007 la infi intarea fi lialei. Grupul are urmatoarele domenii de activitate: bancar, care este desfasurat de catre Volksbank Romania S.A. si servicii auxiliare si procesare de date desfasurate de catre VBRO Services S.R.L.

1.1 VOLKSBANK ROMANIA S.A.

Volksbank Romania S.A. a fost infi intata in ianuarie 2000 ca persoana juridica romana si a fost autorizata de Banca Nationala a Romaniei sa desfasoare activitati in domeniul bancar. Banca si-a demarat activitatea in mai 2000 si activitatea desfasurata de aceasta de refera la operatiuni bancare cu persoane fi zice si juridice din Romania.

Activitatea principala a Bancii consta in furnizarea de servicii bancare destinate sectorului retail, intreprinderilor mici si mijlocii si marilor companii. Acestea includ: deschideri de conturi, atragere de depozite, fi nantari pentru activitatea curenta si pentru investitii, transferuri bancare interne si externe, operatiuni de schimb valutar, garantii bancare, credite documentare etc. Banca este detinuta in proportie de 99,0522% de Volksbank International AG (Austria), cu sediul social in 10 Leonard – Bernstein - Strabe 1220 Viena, Austria.

Sediul social al Bancii este: Soseaua Mihai Bravu nr. 171, Bucuresti, sector 2, Romania. Banca isi desfasoara activitatea prin intermediul sediului sau social localizat in Bucuresti si prin cele 173 de sucursale si agentii in toate judetele tarii (135 la data de 31 decembrie 2007), inclusiv 32 in Bucuresti (26 la data de 31 decembrie 2007) si printr-un numar de 73 de francize. Numarul angajatilor Bancii la 31 decembrie 2008 era de 1.477 angajati (fata de 1.170 la data de 31 decembrie 2007).Banca este administrata in sistemul dualist de un Consiliu de Supraveghere format din 4 membri si un Directorat format din 4 membri.

Membrii Consiliului de Supraveghere sunt: Ralf Weingartner – Presedinte Gerhard Wöber – Vicepresedinte Thomas Capka – Membru Jorg Poglits – Membru

Componenta Directoratului este urmatoarea: Gerald Schreiner – Presedinte Herwig Burgstaller – Vicepresedinte Simona Fatu – Vicepresedinte Valentin Vancea – Vicepresedinte

1.2 VBRO Services S.R.L.

VBRO Services S.R.L. a fost infi intata in anul 2007, ca o societate cu raspundere limitata, conform legislatiei din Romania. Societatea isi desfasoara activitatea prin intermediul sediului sau social localizat in Bucuresti. Societatea ofera servicii auxiliare serviciilor bancare, precum si servicii de brokeraj imobiliar. Societatea a inceput activitatea operationala din ianuarie 2008.

1 . E N T I TAT E A R A P O R TO A R E

41

2.1 DECLARATIE DE CONFORMITATE

Situatiile fi nanciare consolidate ale Grupului au fost intocmite in conformitate cu Standardele Internationale de Raportare Financiara („IFRS”) adoptate de Uniunea Europeana in vigoare la data de raportare anuala a Grupului, 31 decembrie 2008.

Pentru estimarea pierderilor din deprecierea valorii creditelor si avansurilor acordate si a investitiei nete de leasing, Grupul a aplicat metodologia interna prezentata in Nota 3.9.1. - 7.).

Diferente intre situatiile fi nanciare IFRS si situatiile fi nanciare statutareEvidentele contabile ale Bancii sunt mentinute in lei, in conformitate cu legislatia contabila din Romania precum si cu reglementarile bancare in vigoare emise de Banca Nationala a Romaniei. Filiala isi mentine evidentele contabile in conformitate cu legislatia contabila din Romania. Toate aceste evidente contabile ale Bancii si fi lialelor sale sunt denumite in continuare conturi statutare.

Aceste conturi au fost retratate pentru a refl ecta diferentele existente intre conturile statutare si IFRS. In mod corespunzator, conturile statutare au fost ajustate, in cazul in care a fost necesar, pentru a armoniza aceste situatii fi nanciare, in toate aspectele semnifi cative, cu IFRS.

Modifi carile cele mai importante aduse situatiilor fi nanciare statutare pentru a le alinia Standardelor Internationale de Raportare Financiara adoptate de Uniunea Europeana sunt:

• gruparea mai multor elemente detaliate in categorii mai cuprinzatoare;• ajustari ale elementelor de activ si pasiv, in conformitate cu IAS 29 („Raportarea financiara in economii hiperinflationiste”) datorita faptului ca economia romaneasca a fost o economie hiperinflationista pana la 31 decembrie 2003;• alegerea monedei RON ca moneda functionala incepand cu 1 ianuarie 2008;• ajustari la valoare justa si deprecierea valorii instrumentelor fi nanciare, in conformitate cu IAS 39 („Instrumente fi nanciare – recunoastere si evaluare”);• constituirea de provizioane pentru impozitul pe profi tul amanat; • prezentarea informatiilor necesare in conformitate cu IFRS.

2.2 BAZELE EVALUARII

Situatiile fi nanciare consolidate au fost intocmite luand in considerare valoarea justa a instrumentelor fi nanciare derivate, creantelor si datoriilor fi nanciare precum si a instrumentelor fi nanciare disponibile pentru vanzare prin contul de profi t si pierdere, cu exceptia acelora pentru care valoarea justa nu a putut fi stabilita in mod credibil. Alte creante si datorii fi nanciare precum si creantele si datoriile nefi nanciare sunt prezentate la cost amortizat, valoare reevaluata sau cost istoric.

Activele non-curente disponibile pentru vanzare sunt prezentate la valoarea cea mai mica dintre valoarea neta contabila si valoarea justa, mai putin costurile legate de vanzare.

2 . B A Z E L E I N TO C M I R I I

42

2.3 MONEDA FUNCTIONALA SI DE PREZENTARE

Conducerea Bancii a considerat ca moneda RON reprezinta moneda functionala incepand cu 01 ianuarie 2008. Schimbarea monedei functionale a fost aplicata prospectiv de catre Grup.

Elementele incluse in situatiile fi nanciare ale fi ecarei entitati din Grup sunt evaluate folosind moneda mediului economic principal in care entitatea opereaza („moneda functionala”). Situatiile fi nanciare consolidate ale Grupului sunt prezentate in RON, moneda pe care conducerea Bancii a ales-o ca moneda de prezentare.

Potrivit IAS 21, intrucat moneda functionala inainte de 1 ianuarie 2008 a fost EUR, pentru conversia sumelor din EUR in RON au fost respectate urmatoarele proceduri la data de 31 decembrie 2007:

• activele, pasivele si capitalurile proprii pentru toate elementele prezentate in bilant (inclusiv comparativele), au fost transformate la cursul de schimb valabil pentru data bilantului (31 decembrie 2007: 3,6102 RON/EUR);• elementele de natura veniturilor si cheltuielilor au fost convertite in cursul perioadei la cursul de schimb valabil la data efectuarii tranzactiilor la un curs de schimb care aproximeaza cursul de schimb actual (curs mediu in 2007: 3,3373 RON/EUR);• elementele de capitaluri proprii, altele decat rezultatul perioadei care este inclus in rezultatul reportat, au fost convertite la cursul de schimb valabil la data bilantului prezentat (31 decembrie 2007: 3,6102 RON/EUR).

2.4 UTILIZAREA ESTIMARILOR SI JUDECATILOR SEMNIFICATIVE

Pregatirea situatiilor fi nanciare in conformitate cu IFRS adoptate de Uniunea Europeana presupune din partea conducerii utilizarea unor estimari, judecati si presupuneri ce afecteaza aplicarea politicilor contabile, precum si valoarea raportata a activelor, datoriilor, veniturilor si cheltuielilor. Estimarile si judecatile aferente se bazeaza pe experienta si pe numerosi factori presupusi rezonabili in conditiile date, rezultatele acestora formand baza emiterii de judecati cu privire la valoarea contabila a activelor si datoriilor, valoare care nu poate fi dedusa din alte surse. Rezultatele actuale pot fi diferite de valorile estimate.

Estimarile si presupunerile sunt revizuite periodic. Revizuirile estimarilor contabile sunt recunoscute in perioada in care estimarea este revizuita, daca revizuirea afecteaza doar acea perioada, sau in perioada in care estimarea este revizuita si perioadele viitoare daca revizuirea afecteaza atat perioada curenta, cat si perioadele viitoare.

Informatiile legate de acele estimari folosite in aplicarea politicilor contabile care au un efect semnifi cativ asupra situatiilor fi nanciare, precum si estimarile ce implica un grad semnifi cativ de incertitudine, sunt prezentate in Notele 5 si 6.

43

Metodele si politicile contabile semnifi cative prezentate mai jos au fost aplicate in mod consecvent de catre entitatile din Grup de-a lungul exercitiilor fi nanciare prezentate in situatiile fi nanciare consolidate.

Pentru ca informatiile sa fi e comparabile, anumite elemente din situatiile fi nanciare la 31 decembrie 2007 au fost reclasifi cate

pentru a fi in conformitate cu prezentarea situatiilor fi nanciare curente.

3.1 A) BAZELE CONSOLIDARII

3.1.1 Filialele

Filialele sunt entitati afl ate sub controlul Bancii. Controlul exista atunci cand Banca are puterea de a conduce, in mod direct sau indirect, politicile fi nanciare si operationale ale unei entitati pentru a obtine benefi cii din activitatea acesteia. La momentul evaluarii controlului trebuie luate in calcul si drepturile de vot potentiale sau convertibile care pot fi exercitate si in prezent. Situatiile fi nanciare ale fi lialelor sunt incluse in situatiile fi nanciare consolidate din momentul in care incepe exercitarea controlului si pana in momentul incetarii lui.

Banca consolideaza situatiile fi nanciare ale fi lialei sale, VBRO Services S.R.L., in conformitate cu IAS 27 („Situatiile fi nanciare consolidate si individuale”).

3.1.2 Entitati asociate

Entitatile asociate sunt acele societati asupra carora Grupul poate exercita o infl uenta semnifi cativa, dar nu si control asupra politicilor fi nanciare si operationale. Situatiile fi nanciare consolidate includ cota parte a Grupului din rezultatele entitatilor asociate pe baza metodei punerii in echivalenta, de la data la care Grupul a inceput sa exercite infl uenta semnifi cativa si pana la data la care aceasta infl uenta inceteaza. In cazul in care cota parte a Grupului din pierderile entitatii asociate depaseste valoarea contabila a investitiei, valoarea contabila este redusa la zero iar pierderile ulterioare nu sunt recunoscute cu exceptia situatiei in care Grupul are obligatii legale sau constructive in numele entitatii asociate.

Banca detine 20% din capitalul social al societatii Volsbank Leasing IFN S.A., societate care ofera servicii de leasing persoanelor fi zice si juridice. Grupul nu exercita infl uenta semnifi cativa si nu detine control asupra politicilor fi nanciare si operationale ale Volksbank Leasing IFN S.A., prin urmare aceasta societate nu este inclusa in perimetrul de consolidare al Grupului, nefi ind o entitate asociata.

3.1.3 Tranzactiile eliminate la consolidare

Decontarile si tranzactiile in interiorul Grupului, ca si profi turile nerealizabile rezultate din tranzactii in cadrul Grupului, sunt eliminate in totalitate in situatiile fi nanciar contabile. Profi turile nerealizate rezultate din tranzactii cu entitati asociate sunt eliminate in contrapartida cu investitia in societatea asociata.

3 . M E TO D E S I P O L I T I C I C O N TA B I L E S E M N I F I C AT I V E

44

3.2 MONEDA STRAINA

3.2.1 Tranzactii in moneda straina

Operatiunile exprimate in moneda straina sunt convertite in moneda functionala la cursul ofi cial de schimb de la data decontarii tranzactiei. Activele si pasivele monetare inregistrate in devize la data intocmirii bilantului contabil sunt transformate in moneda functionala la cursul ofi cial de schimb valabil la data bilantului. Castigurile sau pierderile din decontare sunt recunoscute in contul de profi t si pierdere, cu exceptia cazurilor in care diferentele de curs provin din translatarea instrumentelor fi nanciare clasifi cate ca fi ind disponibile pentru vanzare care sunt incluse in rezerva provenind din modifi carea valorii juste a acestor instrumente fi nanciare.

Activele si datoriile nemonetare care sunt evaluate la cost istoric in moneda straina sunt convertite in moneda functionala la cursul de schimb de la data tranzactiei. Activele si pasivele nemonetare exprimate in moneda straina care sunt evaluate la valoarea justa sunt convertite in moneda functionala la cursul de schimb din data la care a fost determinata valoarea justa.

Diferentele de conversie sunt prezentate in contul de profi t si pierdere cu exceptia diferentelor rezultate din conversia instrumentelor fi nanciare clasifi cate ca fi ind disponibile pentru vanzare, care sunt incluse in rezerva provenind din modifi carea valorii juste a acestor instrumente fi nanciare.

Ratele de schimb ale principalelor valute la 31 decembrie 2008 si 2007 au fost:

Moneda 31 decembrie 2008 31 decembrie 2007 % Crestere/ (Descrestere)

Euro (EUR) 1: RON 3,9852 1: RON 3,6102 10,38%

Dolar American (USD) 1: RON 2,8342 1: RON 2,4564 15,38%

Franc Elvetian (CHF) 1: RON 2,6717 1: RON 2,1744 22,87%

3.3 VENITURI SI CHELTUIELI DIN DOBANZI

Veniturile si cheltuielile din dobanzi aferente instrumentelor fi nanciare sunt recunoscute in contul de profi t si pierdere la cost amortizat folosind metoda ratei de dobanda efective.

Metoda dobanzii efective este o metoda de calcul a costului amortizat al unui activ fi nanciar sau a unei datorii fi nanciare si de alocare a venitului sau a cheltuielii din dobanzi pe o perioada relevanta de timp. Rata dobanzii efective este rata exacta care actualizeaza estimarile de fl uxuri viitoare de numerar de platit sau de incasat pe perioada de viata a instrumentului fi nanciar, sau, cand e cazul, pe o perioada mai scurta, la valoarea neta raportata a activului sau datoriei fi nanciare. Pentru calculul ratei dobanzii efective, Grupul estimeaza fl uxurile viitoare de numerar luand in considerare toti termenii contractuali ai instrumentului fi nanciar (de exemplu, plati in avans, optiuni call si alte optiuni similare), dar nu tine cont de pierderile viitoare din credit.

45

Metoda de calcul include toate spezele si comisioanele platite sau primite intre partile contractuale care sunt parte integranta a dobanzii efective, costurile de tranzactionare, si alte prime si discounturi.

Metoda liniara reprezinta o metoda de calcul a costului amortizat al imprumuturilor acordate clientilor prin care comisioanele generate de acordarea unui credit, primite de la partile contractante precum si cheltuielile directe aferente trebuie sa fi e incluse in rata de dobanda efectiva si trebuie amortizare si recunoscute ca venit din dobanzi pe o perioada relevanta. Metoda de amortizare liniara folosita la determinarea costului amortizat pentru creditele acordate clientelei reprezinta estimarea cea mai buna a managementului iar efectul fi nanciar generat nu difera semnifi cativ de efectul care ar fi fost obtinut prin aplicarea metodei ratei de dobanda efective.

3.4 VENITURI SI CHELTUIELI DIN SPEZE SI COMISIOANE

Veniturile din speze si comisioane provin in principal din activitatea de creditare, comisioane din operatiuni cu carduri, din servicii de administrare a numerarului, servicii de brokeraj, comisioane pentru emiterea de scrisori de garantie si deschiderea de acreditive. Veniturile si cheltuielile din comisioane direct atribuibile activului sau datoriei fi nanciare la momentul initierii (atat venit cat si cheltuiala), sunt incluse in calculul ratei efective a dobanzii. Comisioanele aferente angajarii creditelor sunt amortizate impreuna cu celelalte costuri directe si recunoscute ca ajustare a ratei de dobanda efectiva a creditului. Alte venituri din comisioane si speze provenite din servicii fi nanciare prestate de catre Grup sunt recunoscute in contul de profi t si pierdere in momentul in care serviciul respectiv este prestat. Alte cheltuieli din speze si comisioane se refera in principal la comisioane de tranzactionare si servicii si care sunt recunoscute in contul de profi t si pierdere in momentul in care serviciul respectiv este prestat.

3.5 VENITURI DIN CONVERSIE VALUTARA SI DERIVATIVE DETINUTE PENTRU MANAGEMENTUL RISCULUI

Venitul net din tranzactionare este reprezentat de diferenta intre castigul si pierderea din activele si datoriile tranzactionabile si derivativele detinute pentru managementul riscului si include modifi carile de valoare justa realizate si nerealizate, precum si diferentele de curs valutar. Venitul net din diferente de curs valutar si derivative detinute pentru managementul riscului este prezentat in cadrul profi tului operational.

3.6 DIVIDENDE

Veniturile din dividende sunt recunoscute in contul de profi t si pierdere la data la care este stabilit dreptul de a primi aceste venituri. Veniturile din participatii si alte investitii fara venit fi x sunt recunoscute ca venituri din dividende atunci cand sunt angajate. Veniturile din dividende sunt refl ectate ca o componenta a veniturilor din operatiuni. Dividendele sunt tratate ca o distribuire a profi tului in perioada in care au fost declarate si aprobate de catre Adunarea Generala a Actionarilor. Singurul profi t disponibil pentru repartizare este profi tul anului inregistrat in conturile statutare romanesti si este diferit de profi tul refl ectat in aceste situatii fi nanciare, intocmite in conformitate cu IFRS adoptate de Uniunea Europeana, din cauza diferentelor intre reglementarile contabile aplicabile in Romania si cele adoptate de Uniunea Europeana.

46

3.7 PLATI DE LEASING

Platile de leasing operational sunt recunoscute in contul de profi t si pierdere pe baza metodei liniare pe durata contractului de leasing. Facilitatile de leasing primite sunt recunoscute ca parte integranta a cheltuielii totale de leasing, pe durata contractului de leasing. Cheltuielile cu leasingul operational sunt recunoscute ca o componenta a cheltuielilor operationale.

Platile minime de leasing in cadrul contractelor de leasing fi nanciar sunt impartite proportional intre cheltuiala cu dobanda de leasing si reducerea datoriei de leasing. Cheltuiala cu dobanda de leasing este alocata fi ecarei perioade de leasing in asa fel incat sa produca o rata de dobanda constanta pentru datoria de leasing ramasa. Platile de leasing contingente sunt recunoscute prin revizuirea platilor minime de leasing pentru perioada de leasing ramasa cand ajustarea de leasing este confi rmata.

3.8 IMPOZITUL PE PROFIT

Impozitul pe profi t aferent exercitiului cuprinde impozitul curent si impozitul amanat. Impozitul pe profi t este recunoscut in contul de profi t si pierdere, sau in capitaluri proprii daca impozitul este aferent elementelor de capital. Impozitul pe profi t curent este impozitul de platit aferent profi tului realizat in perioada curenta, determinat in baza procentelor aplicate la data bilantului si a tuturor ajustarilor aferente perioadelor precedente.

Impozitul pe profi t amanat este determinat folosind metoda bilantiera pentru acele diferente temporare ce apar intre baza fi scala de calcul a impozitului pentru active si datorii si valoarea contabila a acestora folosita pentru raportare in situatiile fi nanciare. Impozitul amanat nu se recunoaste pentru urmatoarele diferente temporare: recunoasterea initiala a fondului de comert, recunoasterea initiala a activelor si datoriilor provenite din tranzactii care nu sunt combinatii de afaceri si care nu afecteaza nici profi tul contabil nici pe cel fi scal si diferente provenind din investitii in subsidiare, cu conditia ca acestea sa nu fi e reversate in viitorul apropiat. Impozitul pe profi t amanat este calculat pe baza procentelor de impozitare care se asteapta sa fi e aplicabile diferentelor temporare la reluarea acestora,

in baza legislatiei in vigoare la data bilantului.

Creanta privind impozitul pe profi t amanat este recunoscuta numai in masura in care este probabil sa se obtina profi t impozabil in viitor dupa compensarea cu pierderea fi scala a anilor anteriori si cu impozitul pe profi t de recuperat. Creanta privind impozitul amanat este diminuata in masura in care benefi ciul fi scal aferent este improbabil sa se realizeze.

Cota de impozit pe profi t utilizata la calculul impozitului pe profi t curent si amanat este la 31 decembrie 2008 de 16% (31 decembrie 2007: 16%).

47

3.9 ACTIVE SI DATORII FINANCIARE

3.9.1 Clasifi care

Grupul clasifi ca activele si datoriile fi nanciare in urmatoarele categorii:

a) Active sau datorii fi nanciare la valoare justa prin contul de profi t si pierdere

Aceasta categorie are doua subcategorii: active fi nanciare sau datorii fi nanciare detinute pentru tranzactionare, si instrumente fi nanciare clasifi cate la valoare justa prin contul de profi t si pierdere la momentul recunoasterii initiale. Un instrument fi nanciar este clasifi cat in aceasta categorie daca a fost achizitionat in principal cu scopul de a se vinde sau daca a fost desemnat in aceasta categorie de catre conducerea entitatii. Instrumentele derivate sunt, de asemenea, incadrate ca fi ind detinute pentru tranzactionare daca nu reprezinta un instrument de acoperire. La 31 decembrie 2008 si 31 decembrie 2007 Grupul nu detinea in portofoliu active sau datorii fi nanciare la valoarea justa prin contul de profi t si pierderi.

b) Activele fi nanciare disponibile pentru vanzare

Activele fi nanciare disponibile pentru vanzare sunt acele active fi nanciare care sunt desemnate ca disponibile pentru vanzare sau care nu sunt clasifi cate drept credite si avansuri, investitii detinute pana la scadenta sau active fi nanciare la valoarea justa prin contul de profi t si pierdere. Instrumentele fi nanciare disponibile pentru vanzare includ titluri de plasament emise de catre stat, certifi cate de trezorerie ce pot fi revandute Bancii Centrale, titlurile de participare ale activitatii de portofoliu care nu sunt detinute pentru tranzactionare sau detinute pana la scadenta.

La data de 31 decembrie 2008 si 31 decembrie 2007 Grupul a inclus in aceasta categorie titlurile de trezorerie emise de Ministerul Finantelor Publice precum si participatiile.

c) Investitiile detinute pana la scadenta

Investitiile detinute pana la scadenta reprezinta acele active fi nanciare cu plati fi xe sau determinabile si scadenta fi xa pe care Grupul are intentia ferma si posibilitatea de a le pastra pana la scadenta. In conditiile in care Grupul procedeaza la vanzarea sau la reclasifi carea de valori semnifi cative de titluri de investitii, in decursul exercitiului fi nanciar curent sau a doua exercitii fi nanciare precedente, aceasta nu va putea clasifi ca niciun activ fi nanciar ca titlu de investitii (regula contaminarii). Aceasta interdictie nu se aplica in situatia in care respectiva vanzare sau reclasifi care:

• este atat de apropiata de scadenta activului financiar (de exemplu, cu mai putin de trei luni inainte de scadenta) incat modificarile ratei dobanzii de pe piata nu ar fi putut avea un efect semnificativ asupra valorii juste a activului financiar; • are loc dupa ce s-a recuperat in mod substantial valoarea principalului activului financiar, prin plati esalonate sau prin rambursari anticipate; sau• este atribuita unui eveniment izolat, nu este repetitiv si nu putea fi anticipat in mod rezonabil.

48

In situatia in care respectiva vanzare sau reclasifi care nu se incadreaza intr-unul din cazurile de mai sus, toate titlurile de investitii vor fi reclasifi cate in categoria titlurilor de plasament. La data de 31 decembrie 2008 Grupul avea in portofoliu titluri de stat detinute pana la scadenta. La data de 31 decembrie 2007, Grupul nu avea in portofoliu instrumente fi nanciare detinute pana la scadenta.

d) Creditele si avansurile

Creditele si avansurile sunt active fi nanciare nederivate cu plati fi xe sau determinabile care nu sunt cotate pe o piata activa, altele decat acelea pe care Grupul intentioneaza sa le vanda imediat sau in viitorul apropiat, acelea pe care Grupul, in momentul recunoasterii initiale, le clasifi ca ca fi ind active fi nanciare detinute pentru tranzactionare, acelea pe care Grupul, dupa recunoasterea initiala, le desemneaza ca fi ind disponibile pentru vanzare sau acelea pentru care detinatorul ar putea sa nu recupereze substantial toata investitia initiala, din alt motiv decat datorita deprecierii creditului. Creditele si creantele includ imprumuturile si avansurile acordate bancilor si clientilor.

3.9.2. Recunoastere

Activele fi nanciare si datoriile fi nanciare sunt evaluate initial la valoare justa plus, in cazul activelor fi nanciare si datoriilor fi nanciare altele decat cele la valoare justa prin contul de profi t si pierdere, costurile de tranzactionare direct atribuibile. Grupul recunoaste initial creditele si creantele, depozitele si datoriile subordonate la data la care sunt create. Toate celelalte active si pasive fi nanciare (inclusiv cele la valoare justa prin contul de profi t si pierdere) sunt recunoscute initial la data tranzactionarii la care Grupul a devenit parte la prevederile contractuale ale instrumentului fi nanciar.

3.9.3. Derecunoastere