Revista Amfiteatru Economic Academia de Studii Economice ... · Revista este indexat ă în baze de...

311

Revista Amfiteatru Economic Academia de Studii Economice din Bucureşti Facultatea de Comerţ Anul X ● Iulie 2008 ● Nr. 24 Apariţie semestrialã Revista Amfiteatru Economic este clasificată şi recunoscută de către Consiliul Naţional al Cercetării Ştiinţifice din Învăţământul Superior în categoria B+ Codul CNCSIS 283 Revista este indexată în baze de date internaţionale Journal of Economic Literature (EconLit) http://www.econlit.org/journal_list.html International Bibliography of the Social Sciences (IBSS) http://www.lse.ac.uk/collections/IBSS/about/alphabeticalJournals.htm Research Papers in Economics (RePEc) http://ideas.repec.org/s/aes/amfeco.html ISSN 1582-9146 www.amfiteatrueconomic.ase.ro Tematica viitoarelor două numere: • Revista nr. 25 – Profesii şi ocupaţii în domeniul comercial • Revista nr. 26 – Managementul calităţii în servicii

Transcript of Revista Amfiteatru Economic Academia de Studii Economice ... · Revista este indexat ă în baze de...

Revista Amfiteatru Economic

Academia de Studii Economice din Bucureşti

Facultatea de Comerţ Anul X ● Iulie 2008 ● Nr. 24

Apariţie semestrialã

Revista Amfiteatru Economic este clasificată şi recunoscută de către Consiliul Naţional al Cercetării Ştiinţifice din Învăţământul Superior în categoria B+

Codul CNCSIS 283

Revista este indexată în baze de date internaţionale Journal of Economic Literature (EconLit) http://www.econlit.org/journal_list.html

International Bibliography of the Social Sciences (IBSS) http://www.lse.ac.uk/collections/IBSS/about/alphabeticalJournals.htm

Research Papers in Economics (RePEc) http://ideas.repec.org/s/aes/amfeco.html

ISSN 1582-9146 www.amfiteatrueconomic.ase.ro

Tematica viitoarelor două numere:

• Revista nr. 25 – Profesii şi ocupaţii în domeniul comercial • Revista nr. 26 – Managementul calităţii în servicii

Colegiul de redacţie Redactor-şef: Vasile DINU Redactor-şef adjunct: Puiu NISTOREANU Secretar general de redacţie: Ion STANCIU Redactori: Rodica PAMFILIE, Gabriela STĂNCIULESCU, Adriana PIETRĂREANU, Laurenţiu TĂCHICIU, Bogdan ONETE, Călin VÎLSAN, Dan-Laurenţiu ANGHEL, Sorin-George TOMA, Alexandru NEDELEA, Cristinel VASILIU, Mădălina ALMĂ.

Consiliul ştiinţific Prof. univ. dr. Ion Gh. Roşca Academy of Economic Studies, Bucharest Prof. univ. dr. Viorel Lefter Academy of Economic Studies, Bucharest Prof. univ. dr. Ion Stancu Academy of Economic Studies, Bucharest Professor Ph.D. Daniel A. Glaser-Segura Our Lady of the Lake University, San-Antonio, Texas

Associate Director Ph.D. Kravtsiv, Vasyl Stepanovych Institute for Regional Research of the Schience

Academy of Ukraine, Lviv

Associate Professor Ph.D. Aaron Ahuvia University of Michigan-Dearborn Professor Ph.D. Abraham Pizam Rosen School of Hospitality Management, University

of Central Florida, Orlando, Florida

Assistant Professor Ph.D Daniel Stavarek Silesian University, School of Business

Administration, Karvina

Ph.D. Yankov (Nicolov) Nicola Tsenov Academy of Economics, Svishtov

Professor Ph.D. Carlos Costa Universidade de Aveiro Associate Professor Ph.D. Čerović Slobodan Faculty of Natural Sciences, Belgrad

Associate Professor Ph.D. Peev Gueorgui New Bulgarian University, Sofia

Chief Assist Professor Ph.D. Vanya Banabakova National Military University, Veliko Turnovo

Ph.D. Tatjana Petrovska Mircevska University St. Cyril and Methodius, Skopje

Teaching Assistant Maja Djucik Faculty of Economics, Belgrad

Prof. univ. dr. Aurel Burciu University“Ştefan cel Mare”, Suceava

Lecturer Dr. George P. Babu University of Southern Mississippi, USA

Lecturer Ph.D. Olga Blinkova Karazin Kharkiv National University, Kharkiv

Professor Ph.D. Jonathan R. Edwards Bournemouth University, Poole Conf. univ. dr. Vasile Dinu Academy of Economic Studies, Bucharest Conf. univ. dr. Puiu Nistoreanu Academy of Economic Studies, Bucharest Prof. univ. dr. Traian Surcel Academy of Economic Studies, Bucharest

Prof. univ. dr. Rodica Milena Zaharia Academy of Economic Studies, Bucharest Conf. univ. dr. Valentin Hapenciuc University „Ştefan cel Mare”,

Suceava

Comisia de referenţi interni Ph.D. Renata TOMLJENOVIC, Institute for Tourism, Zagreb Ph.D. Cerovic SLOBODAN, Faculty of Natural Sciences, Novi Sad Ph.D. Nela POPESCU, Academy of Economic Studies, Bucharest Ph.D. Ion SCHILERU, Academy of Economic Studies, Bucharest Ph.D. George BABU, Pondicherry University, Pondicherry Ph.D. Dimitar EFTIMOVSKI, University „St. Klimet Ohridski”, Bitola Ph.D. Nicolae LUPU, Academy of Economic Studies, Bucharest Ph.D. Adriana CORFU, Instituto Politecnico de Viana do Castelo, Escola Superior de Tecnologia e Gestao, Aveiro

Editura Editura ASE Piaţa Romană, nr. 6, sector 1, Bucureşti, România cod 010374 Telefon: 021/211.26.50/146 E-mail: [email protected] www.ase.ro

Revizie text şi tehnoredactare Liliana MATEI – redactor şef, Editura ASE Violeta ROGOJAN – Editura ASE

AE

Nr. 24 • Iunie 2008 3

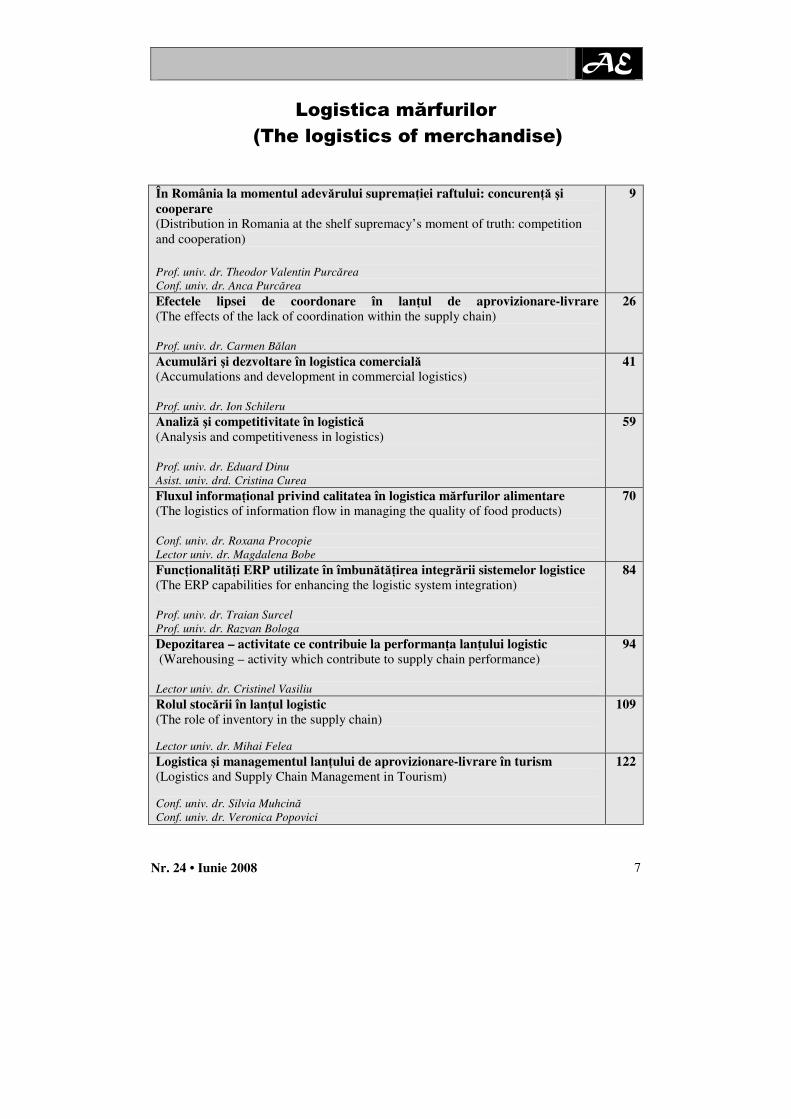

CUPRINS 5 Logistica mărfurilor

The logistics of merchandise Redactor-şef: Conf. univ. dr. Dinu Vasile

I. THE LOGISTICS OF MERCHANDISETHE LOGISTICS OF MERCHANDISETHE LOGISTICS OF MERCHANDISETHE LOGISTICS OF MERCHANDISE

9 Distribution in Romania at the shelf supremacy’s moment of truth: competition and cooperation Prof. univ. dr. Theodor Valentin Purcărea, Conf. univ. dr. Anca Purcărea

26 The effects of the lack of coordination within the supply chain Prof. univ. dr. Carmen Bălan

41 Accumulations and development in commercial logistics

Prof. univ. dr. Ion Schileru

59 Analysis and competitiveness in logistics Prof. univ. dr. Eduard Dinu, Asist. univ. drd. Cristina Curea

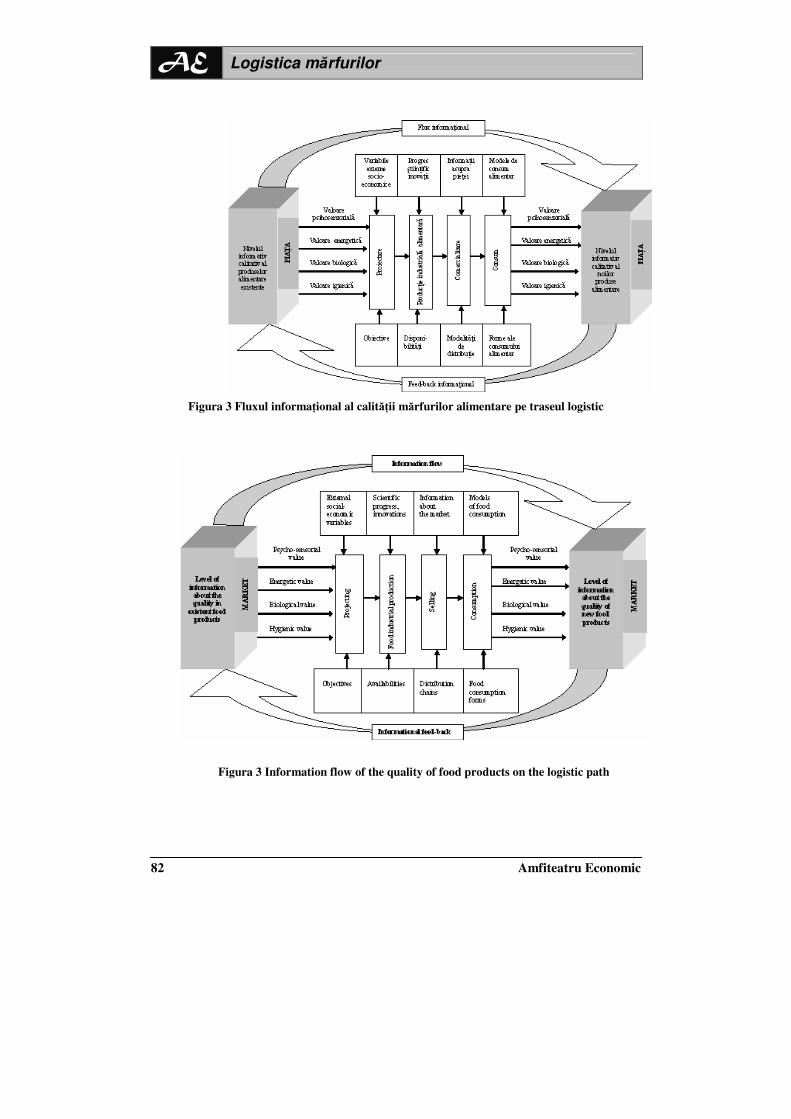

70 The logistics of information flow in managing the quality of food products

Conf. univ. dr. Roxana Procopie, Lect. univ. dr. Magdalena Bobe

84 The ERP capabilities for enhancing the logistic system integration Prof. univ. dr. Traian Surcel, Prof. univ. dr. Razvan Bologa

94 Warehousing – activity which contribute to supply chain performance

Lect. univ. dr. Cristinel Vasiliu

109 The role of inventory in the supply chain

Lect. univ. dr. Mihai Felea

122 Logistics and Supply Chain Management in Tourism

Conf. univ. dr. Silvia Muhcină, Conf. univ. dr. Veronica Popovici

133 Distribution- the synergetic process in establishing the value

Conf. univ. dr. Monica Aureliana Petcu, Conf. univ. dr. Iulia David Sobolevschi

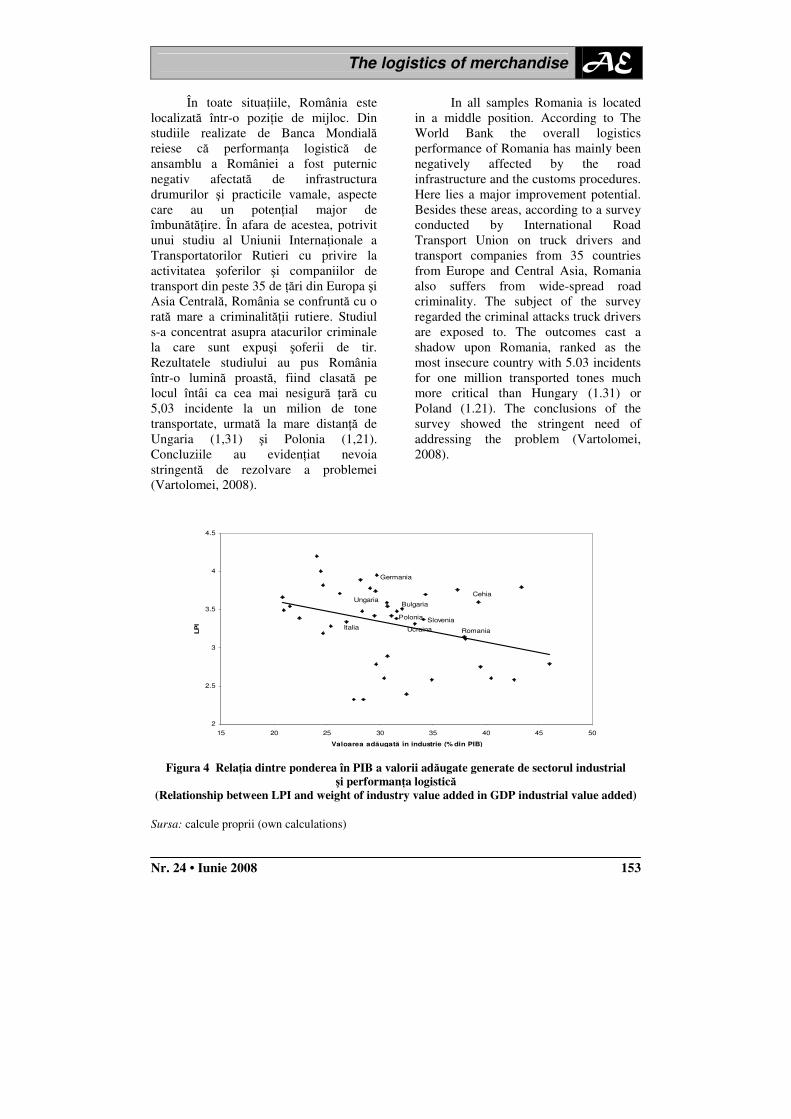

143 An analysis of explanatory factors of logistics performance of a country Conf. univ. dr. Basarab Gogoneaţă

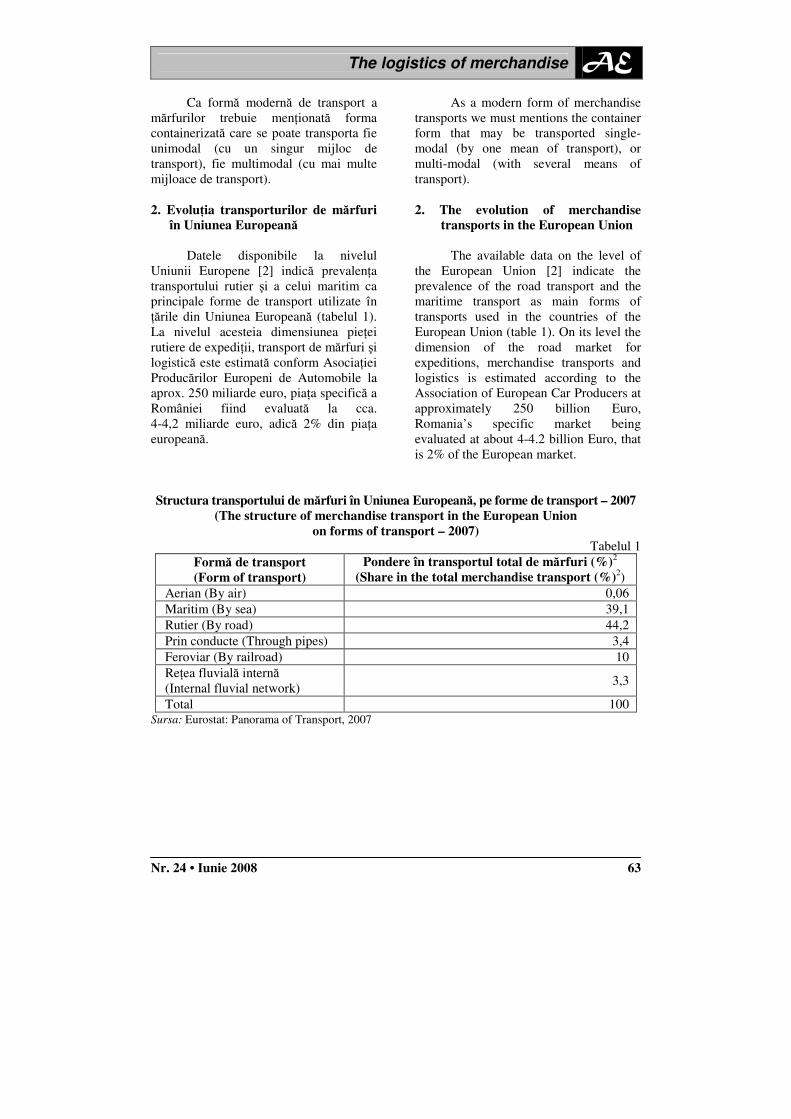

157 Actualities in logistics and transport Conf. univ. dr. Simona Dordea, Conf. univ. dr. Liliana Nicodim

166 A LSCM approach to the romanian pharmaceuticals market Lect. dr. Mihaela Cornelia Prejmerean, Asist. drd. Simona Vasilache

177 The particularities of logistics related to e-commerce Asist. univ. drd. Irina (Albăstroiu) Mărunţelu

192 The importance of reverse logistics for retail activity Prep. univ. drd. Mihaela Moise

210 The growth of freight transport role – implications to logistical framework

Prep. univ. drd. Tatiana-Roxana Nae

224 The performance of the supply chain: Strategical harmonization Lect. univ. dr. Oana Şeitan

AE

Amfiteatru Economic 4

236 Information system for the supply chain management Drd. Delia Adriana Mărincaş

II. Economic Interferences

257 Reservation prices and pre-auction estimates: a study in abstract art Calin Valsan, Robert Sproule

273 How does sector concentration evolve at country and region levels? The european case Lecturer Ph. D. CRIEF Cornel Oros, Lecturer Ph.D. ISEME–ESCEM Researcher, CRIEF, Camelia Romocea Turcu

283 Specifics of Chinese business negotiation practices

Jitka Odehnalová, Master of Economics

III. „Amfiteatru Economic” vă recomandă

299

BUNE PRACTICI

Benefits of academic integrity and mentorship Lect. univ. dr. Nela Popescu

305

NEVOIA DE PERSONALITĂŢI

Omul care a format profesionişti, dar şi caractere: prof. univ. dr. Nicolae Sută Prof. univ. dr. Dumitru Miron

311

RECENZIE DE CARTE

Principles of Hotel Front Office Operations Conf. univ. dr. Nicolae Lupu,

Prep. univ. Andreea Marin-Pantelescu

The logistics of merchandise AE

Nr. 24 • Iunie 2008 5

I. THE LOGISTICS OF MERCHANDISE

(Logistica mărfurilor)

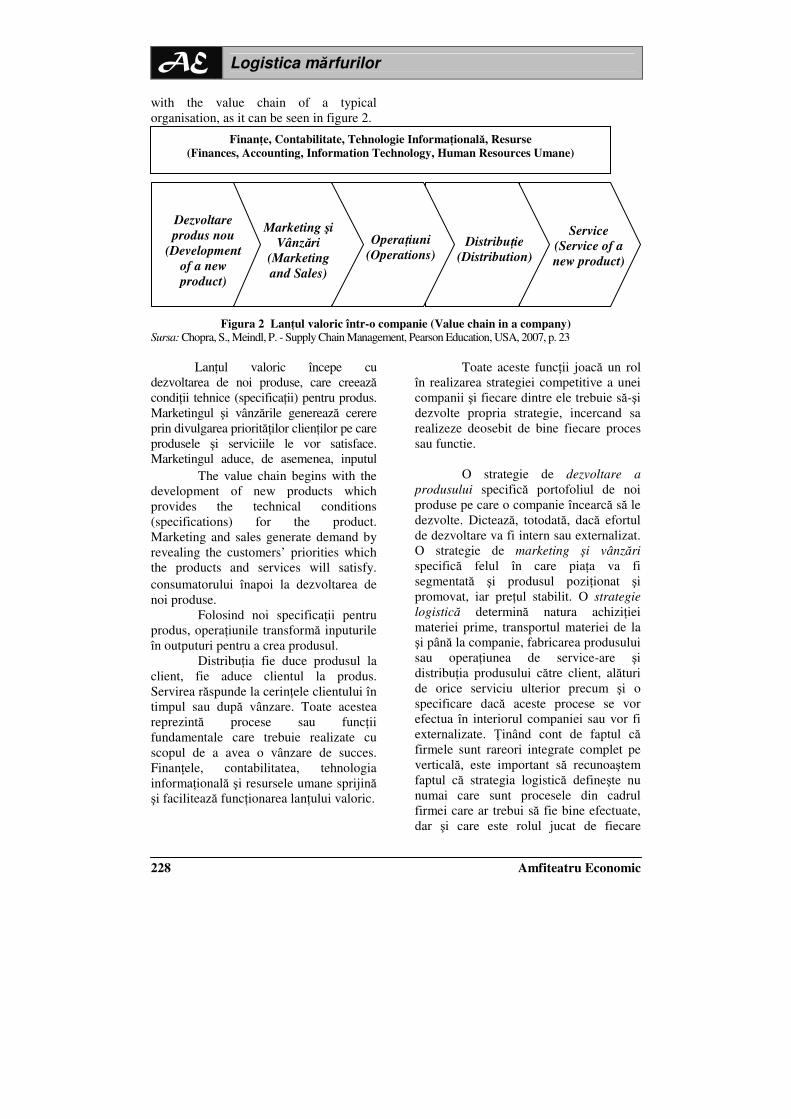

Until recently, logistics was considered to be related especially to the distribution of finite products, as the last stage of the production, being confounded with “down stream logistics”. Such an approach ignored the role of “up stream logistics” (ensuring material resources necessary to the company) and the role of “internal logistics” (making resources available on the production flow).

In reality, achieving the mission of logistics – to ensure required goods and services at the right time and place, by minimizing the cost – demand running a number of inter-correlated operations representing the logistic activities mix. The logistic mix includes two types of activities: core activities and support activities. The “core activities” (buying, transporting, stock management, order processing) are key activities done in almost any logistic channel, and the “support activities” (warehousing, handling of products, packaging, activities related to logistics information flows) are carried on in depending on specific company’s conditions.

Logistics is based on a system conception. Its goal is the rational management of materials and information flows in order to meet demand and to fulfill customers’ orders in due time. Logistics is the science about planning, organizing, managing, control and regulating materials and information flows from their source to the final consumer.

Company’s logistics involves, in the mean time, “the management of materials” (supply, stock management, production programming), and the “physical distribution” (products’ management, warehouse management, transportation management, delivery to the points of sale etc.). More than this, it involves the provision of “services for the clients”. In connection with these components, the external environment of the company is also of interest for logistics, in particular the infrastructures and the socio-political conditions that may facilitate or hamper the free movement of goods and persons.

The logistic capacity of a company is defined by the way in which it organizes and manages people, equipments, locations and operations. The logistic activities fulfill several roles and responsibilities as follows: • Customer service – it concentrates on understanding what are the expectations of customers and on measuring the logistics performance against these expectations; • The forecast of demand – should be such as to assist proper planning, resources allocation and reaching a high level of customer service with minimum cost; • Information management – by collecting and processing in form of information useful to decision making data about customers, transporters and stocks; • Materials handling – bearing a significant cost, may

Până nu demult, logistica era asociată cu distribuţia produselor finite, adică ultima etapă a producţiei, respectiv cu logistica în aval. Acest punct de vedere a ignorat rolul logisticii în amonte (asigurarea disponibilităţii resurselor materiale destinate activităţii firmei) şi a logisticii interne (punerea la dispoziţia producţiei a resurselor necesare).

În realitate, îndeplinirea misiunii logistice de asigurare a bunurilor sau serviciilor, solicitate la momentul şi locul potrivit şi în condiţiile celor mai mici costuri pentru firmă, presupune desfăşurarea unui ansamblu de operaţiuni intercorelate, care constituie mixul activităţilor logistice. Mixul logistic include două categorii de activităţi: de bază şi de susţinere. Activităţile de bază (cumpărarea, transportul, gestiunea stocurilor, prelucrarea comenzilor) sunt operaţiuni cheie care se desfăşoară în aproape orice canal logistic, iar activităţile de susţinere (depozitarea, manipularea produselor, ambalarea, activităţile legate de fluxurile informaţionale logistice) au loc în funcţie de condiţiile specifice ale firmelor.

Concepţia principală a logisticii este conceptul sistemic, iar scopul – gestiunea raţională a fluxurilor materiale şi informaţionale pentru satisfacerea cererii şi expedierea la timp a comenzilor.

Logistica este ştiinţa despre planificarea, organizarea, gestiunea, controlul şi reglementarea circulaţiei fluxurilor materiale şi informaţionale în timp şi spaţiu de la sursa lor primară până la consumatorul final.

Logistica firmei presupune atât domeniul gestiunii materialelor (aprovizionare, gestiunea stocurilor de materiale, programarea producţiei), cât şi domeniul distribuţiei fizice (gestiunea produselor, a depozitelor şi a transporturilor, livrările la punctele de vânzare) dar şi domeniul serviciilor pentru clienţi. Alături de aceste aspecte, mai apar ca argumente de interes logistic: mediul extern, adică infrastructurile şi condiţiile socio-politice care ar putea favoriza dar şi împiedica libera circulaţie a mărfurilor şi/sau a persoanelor.

Capacitatea logistică a unei organizaţii este definită de modul în care aceasta organizează şi gestionează oamenii, echipamentele, locaţiile şi politicile operaţionale. Există o serie de roluri şi responsabilităţi ale activitaţilor logistice, printre care:

• Customer service - se concentrează asupra înţelegerii a ceea ce doresc clienţii şi măsurarea performanţelor logistice faţă de cerinţele acestora;

• Previziunea cererii - trebuie dezvoltată astfel încât să ajute planificarea şi alte activităţi logistice, alocarea resurselor şi atingerea unui înalt nivel de customer service la cel mai mic cost;

• Managementul informaţiei - se referă la date despre clienţi, transportatori şi stocuri ce trebuie să se regăsească în informaţiile utile pentru luarea deciziei;

• Manipularea materialelor - care costă şi poate fi un factor de distrugere, motiv pentru care fabricile şi depozitele trebuie să aibă un design care să permită minimizarea mişcărilor pentru îndeplinirea

AE Logistica mărfurilor

Amfiteatru Economic 6

also generate damage, so factories and warehouses should be designed to minimize the handling in achieving current tasks; • Order processing – is initiating the logistic process; it benefits from electronic technologies that improve speed and accuracy in order fulfillment; • Packaging – ensures the protection of products during the distribution process; • Spare parts and service – should be permanently available in support of the sale activity; • Location – may facilitate achieving a high level of customer service and reducing cost; • Returns – ensuring that defective products or orders incorrectly fulfilled are taken back in an efficient way; • Transportation management – as the most visible component of logistics, transportation may be done by rail, road, water, air, pipes, or internet; • Management of warehouses and distribution

platforms – having the role of keeping products in stock until their use.

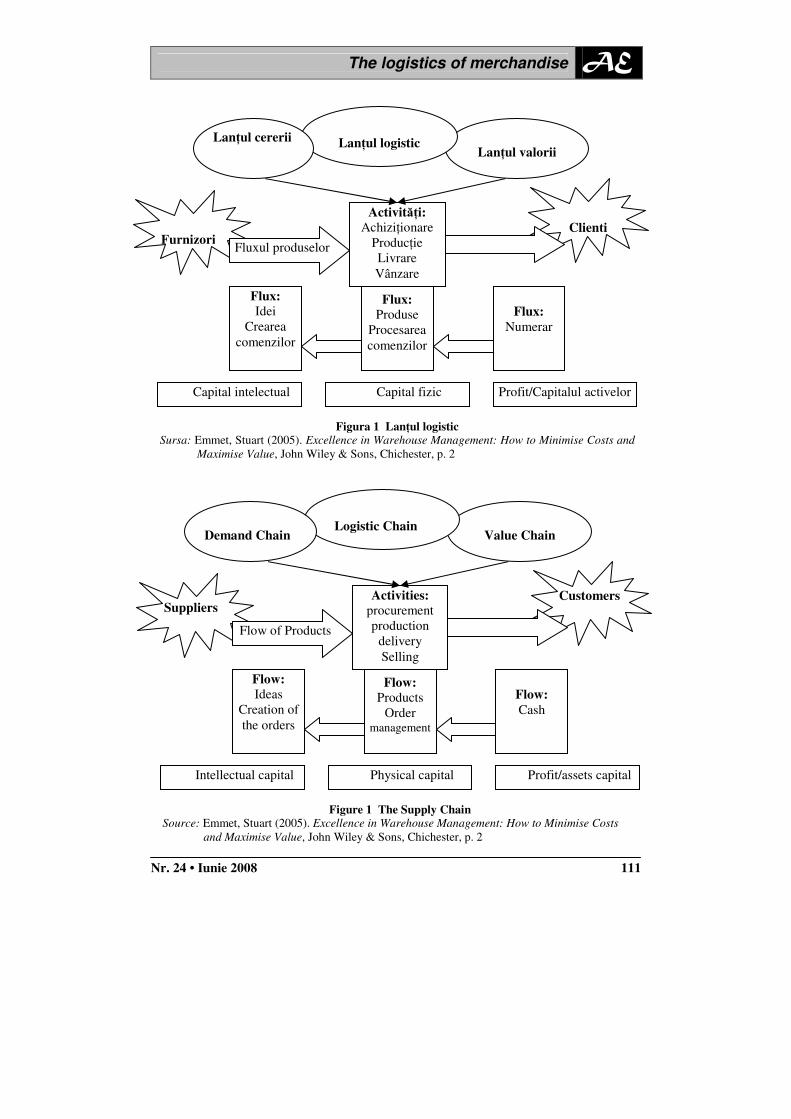

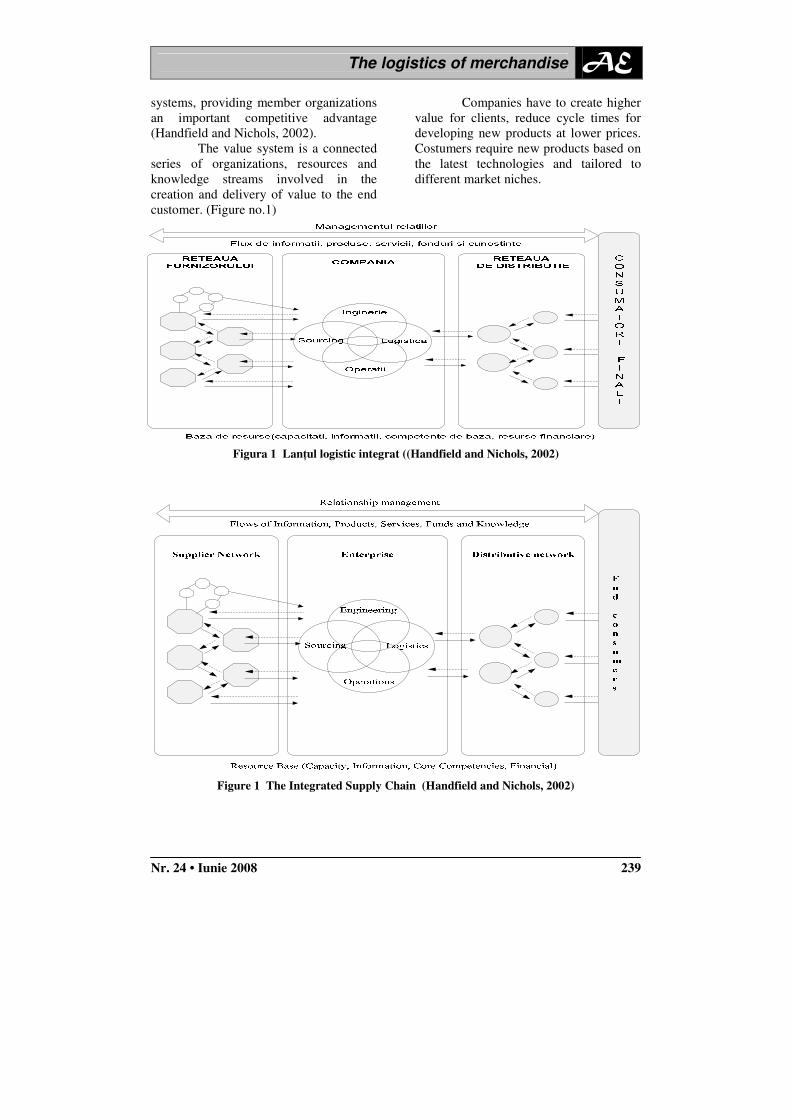

Supply Chain Management is also an important concept in logistics. This concept is more comprehensive than logistics because it involves a network of communications and connections between logistic activities and the company’s personnel. A supply chain is an infrastructure network and distribution options that serve the following functions: buying and procurement of resources, processing and transforming resources in products as well as physical distribution of products to intermediate or final customers. The essential difference between logistics and Supply Chain Management is related to the expansion of logistic cycle from the organization to its suppliers and customers in an integrated way. Actually, a supply chain includes manufacturing and service providing companies as well.

Logistics has an ever increasing role in the activity of the companies, being permanently connected to production, selling, marketing, customers’ serving. By organizing an efficient logistic activity, companies ensure the delivery of the right products at the right time, place, and price, with favorable effects in improving operations efficiency, reducing costs and increasing the level of customer service. In such a way, logistics really contributes to the company’s rate of return, being a source of competitive advantage.

As producers are confronted with markets increasingly complex and competitive, the role of logistics in satisfying customers’ requirements will raise. Companies that will be able to better develop strategic alliances with suppliers, transporters, distributors and customers will get higher rates of return compared with companies that do not consider such alliances.

sarcinilor curente; • Procesarea comenzilor - iniţiază actul

logistic, ele fiind din ce în ce mai mult transmise electronic, crescând astfel viteza şi acurateţea de onorare a comenzilor;

• Ambalarea - asigură protejarea produselor în procesul de distribuţie;

• Piese de schimb şi service - trebuie să fie permanent disponibile ca suport pentru activitatea de vânzare;

• Locaţia - poate furniza o serie de facilităţi care să ducă la obţinerea unui bun nivel de customer service şi costuri reduse:

• Retururi - produsele defecte sau comenzile incorecte trebuie să fie returnate în mod eficient;

• Managementul transportului - transportul este cea mai vizibilă activitate logistică, el putând fi: pe calea ferată, rutier, pe apă, prin aer, conducte şi spaţiu cibernetic;

• Managementul depozitelor/centrelor de distribuţie - cu rolul de a stoca produsele până când acestea trebuie utilizate. Un concept logistic important este şi Supply Chain Management. Dacă logistica descrie totalitatea proceselor prin care resursele şi produsele intră, traversează şi ies din companie, Supply Chain Management înglobează un concept mai larg decât logistica, conectând-o cu o întreagă reţea de comunicaţii şi cu personalul companiei. Practic un supply chain reprezintă o reţea de infrastructură şi opţiuni de distribuţie ce îndeplinesc urmatoarele funcţii: cumpararea şi achiziţia de resurse, procesarea şi transformarea resurselor în produse, precum şi distribuţia fizică a produselor finite către clienţi, intermediari sau finali. Diferenţa esenţială dintre cele două este dată de extinderea ciclului logistic de la nivelul organizaţiei la nivelul furnizorilor şi clienţilor, prin integrarea acestora. Practic în suplly chain-uri există atât firme de producţie, cât şi firme furnizoare de servicii.

Logistica are un rol din ce în ce mai important în activitatea firmelor, aflându-se într-o conexiune permanentă cu producţia, vânzarea, marketingul şi servirea clienţilor. Prin organizarea unei activităţi logistice eficiente, se asigură livrarea produselor potrivite la locul şi timpul potrivit, şi la preţul potrivit, permiţând creşterea eficienţei operaţionale, reducerea costurilor şi creşterea nivelului de servire a clienţilor. În acest fel logistica îşi aduce o contribuţie reală la creşterea rentabilităţii firmei, devenind o sursă reală de avantaj competitiv.

Pe măsură ce producătorii se confruntă cu pieţe din ce în ce mai complexe şi concurenţiale, logistica va juca un rol tot mai mare în servirea clienţilor. Acele firme care vor cultiva cel mai bine alianţele strategice cu furnizorii, transportatorii, distribuitorii şi clienţii vor obţine profituri mai mari decât firmele care nu iau în considerare astfel de alianţe.

Editor-in-chief, Prof. univ. dr. Dinu Vasile

AE

Nr. 24 • Iunie 2008 7

Logistica mărfurilor

(The logistics of merchandise)

În România la momentul adevărului supremaţiei raftului: concurenţă şi

cooperare (Distribution in Romania at the shelf supremacy’s moment of truth: competition and cooperation) Prof. univ. dr. Theodor Valentin Purcărea

Conf. univ. dr. Anca Purcărea

9

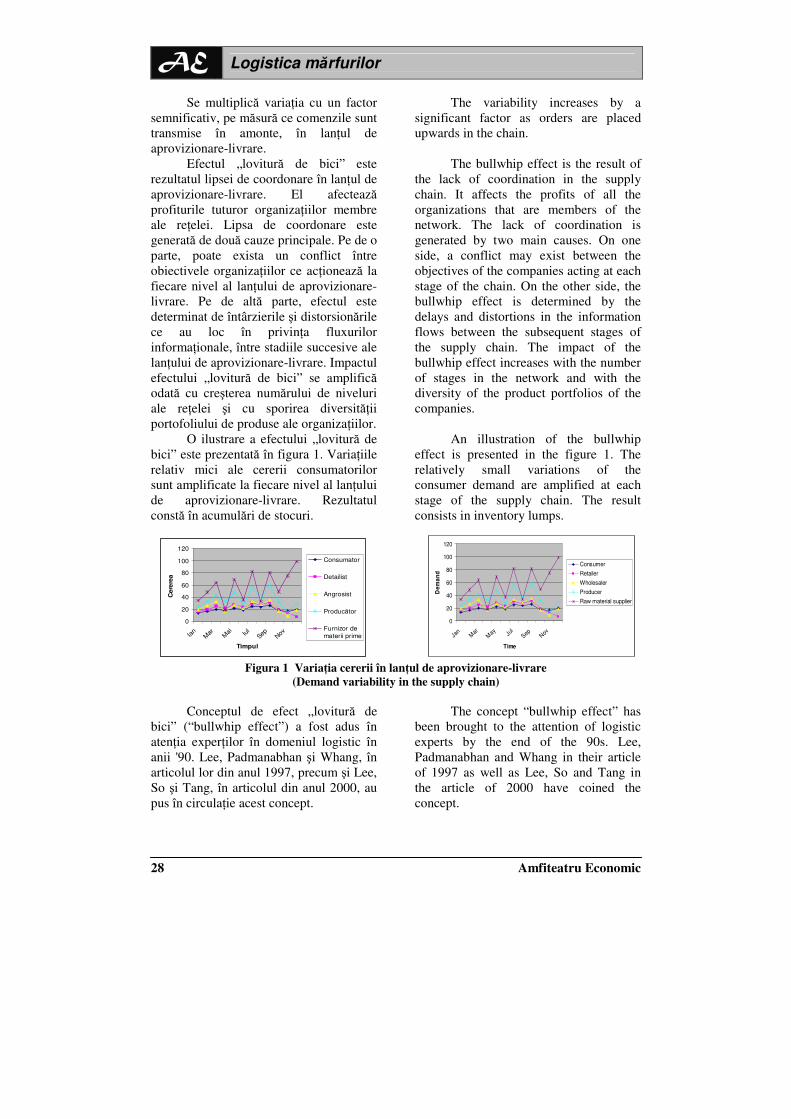

Efectele lipsei de coordonare în lanţul de aprovizionare-livrare (The effects of the lack of coordination within the supply chain) Prof. univ. dr. Carmen Bălan

26

Acumulări şi dezvoltare în logistica comercială (Accumulations and development in commercial logistics) Prof. univ. dr. Ion Schileru

41

Analiză şi competitivitate în logistică (Analysis and competitiveness in logistics) Prof. univ. dr. Eduard Dinu

Asist. univ. drd. Cristina Curea

59

Fluxul informaţional privind calitatea în logistica mărfurilor alimentare (The logistics of information flow in managing the quality of food products) Conf. univ. dr. Roxana Procopie

Lector univ. dr. Magdalena Bobe

70

Funcţionalităţi ERP utilizate în îmbunătăţirea integrării sistemelor logistice (The ERP capabilities for enhancing the logistic system integration) Prof. univ. dr. Traian Surcel

Prof. univ. dr. Razvan Bologa

84

Depozitarea – activitate ce contribuie la performanţa lanţului logistic (Warehousing – activity which contribute to supply chain performance) Lector univ. dr. Cristinel Vasiliu

94

Rolul stocării în lanţul logistic (The role of inventory in the supply chain) Lector univ. dr. Mihai Felea

109

Logistica şi managementul lanţului de aprovizionare-livrare în turism (Logistics and Supply Chain Management in Tourism) Conf. univ. dr. Silvia Muhcină

Conf. univ. dr. Veronica Popovici

122

AE

Amfiteatru Economic 8 8

Distribuţia – proces sinergetic în crearea valorii (Distribution – the synergetic process in establishing the value) Conf. univ. dr. Monica Aureliana Petcu

Conf. univ. dr. Iulia David Sobolevschi

133

O analiză a factorilor determinanţi pentru performanţa logistică a unei ţări (An analysis of explanatory factors of logistics performance of a country) Conf. univ. dr. Basarab Gogoneaţă

143

Actualităţi în logistică şi transport (Actualities in logistics and transport) Conf. univ. dr. Simona Dordea

Conf. univ. dr. Liliana Nicodim

157

Particularităţi ale pieţei româneşti de produse farmaceutice din

perspectiva logisticii şi managementului lanţului de aprovizionare-livrare (A LSCM approach to the romanian pharmaceuticals market) Lect. dr. Mihaela Cornelia Prejmerean

Asist. drd. Simona Vasilache

166

Particularităţile logisticii în comerţul electronic (The particularities of logistics related to e-commerce) Asist. univ. drd Irina (Albăstroiu) Mărunţelu

177

Importanţa logisticii inverse pentru activitatea de comerţ (The importance of reverse logistics for retail activity) Prep. univ. drd. Mihaela Moise

192

Creşterea rolului transporturilor de mărfuri - implicaţii în cadrul logisticii (The growth of freight transport role – implications to logistical framework) Prep. univ. drd. Tatiana-Roxana Nae

210

Performanţa lanţului logistic: armonizarea strategică (The performance of the supply chain: Strategical harmonization) Lector univ. dr. Oana Şeitan

224

Sistem informatic pentru managementul lanţului logistic (Information system for the supply chain management) Drd. Delia Adriana Mărincaş

236

The logistics of merchandise AE

Nr. 24 • Iunie 2008 9

ÎN ROMÂNIA LA MOMENTUL ADEVĂRULUI SUPREMAŢIEI

RAFTULUI: CONCURENŢĂ ŞI COOPERARE (Distribution in Romania at the shelf supremacy’s moment

of truth: competition and cooperation)

Prof. univ. dr. Theodor Valentin Purcărea, Universitatea Româno-Americană,

Bucureşti, România, [email protected]

Conf. univ. dr. Anca Purcărea, Academia de Studii Economice din

Bucureşti, România, [email protected]

Rezumat Acest articol explorează dezvoltarea pieţei de retail din România, evoluţiile actuale

pe această piaţă şi impactul conflictului recent dintre retaileri şi producătorii români,

pornind de la întrebări actuale nu numai în România, dar şi la nivel european. Începutul

acestui conflict producători-retaileri a scos în evidenţă accentul pus pe comportamentul

etic al retailerilor în contextul procesului de cumpărare al produselor de la furnizori,

respectiv numeroasele taxe impuse furnizorilor pentru ca produsele acestora să ajungă pe

rafturile marilor magazine, produsele deplasându-se prin lanţul ofertei a cărui eficacitate

depinde de relaţiile de colaborare dintre participanţii care se confruntă şi cu o serie de

constrângeri legale şi etice, cele legale rezultând, în general, din legislaţia concurenţială şi

cea privind protecţia consumatorilor. România a confirmat poziţionarea sa ca o piaţă

importantă pentru marile lanţuri de distribuţie. Promotorul dezvoltarii reţelelor de retail a

fost comportamentul consumatorului, în provocatorul context al relaţiei dintre impactul

marketingului asupra consumatorului şi impactul consumatorului asupra strategiilor de

marketing.

Numeroase binecunoscute lanţuri de distribuţie participă în prezent în mod activ pe

piaţa românească. A fost evidenţiată necesitatea făuririi unui ecosistem al conversaţiei,

bazat pe comunicare interpersonală, dând naştere unei experienţe partajate, construind

încredere şi întărind relaţiile între participanţii la lanţul ofertei. Aceasta implică evaluarea

relaţiei între producătorii români şi marile lanţuri de distribuţie şi impactul acestei relaţii

asupra bunăstării sociale.

Cuvinte cheie: ●piaţa de retail, ●parteneriat producător-distributor-consumator, ●mari

lanţuri de distribuţie, ●taxe de raft, ●bunăstare a consumatorului.

Clasificare JEL: D23, D43, K21, L41, L42, M38

Abstract

This article explores the development of the Romanian retail market, the recent

evolutions on this market and the impact of the recent conflict between the retailers and the

Romanian producers, starting from current questions not only in Romania but also at

European level. The beginning of this conflict producers-retailers emphasized the accent

placed on the retailers’ ethical behaviour in the context of the buying process of products

from suppliers, namely the numerous slotting fees imposed on the suppliers so that their

products reach the store’s shelves, covering the supply chain’s path whose efficacy depends

on the collaboration relationships between participants, who also confront with a series of

legal and ethical constraints, the legal ones resulting, in general, from the competition

legislation and the one concerning consumers protection. Romania has confirmed its

positioning as an important market for the large distribution chains. The promoter of the

AE Logistica mărfurilor

Amfiteatru Economic 10

development of retail networks has been the consumer behaviour, within the challenging

framework of the relation between marketing’s impact on consumer and consumer’ impact

on marketing strategies.

At the moment, numerous well-known distribution chains are actively participating

on the Romanian market. The necessity of building an ecosystem of conversation, based on

interpersonal communication, is being emphasized, creating a shared experience, building

trust and strengthening the relationships between the participants in the supply chain. This

involves evaluating the relationship between Romanian producers and the large

distribution chains and the impact of this relationship on the social welfare.

Keywords: ●retail market, ●producer-distributor-consumer partnership, ●large

distribution chains, ●slotting fees, ●consumer welfare.

JEL classification: D23, D43, K21, L41, L42, M38

Introducere Un studiu pe care l-am prezentat

cu ocazia Conferinţei Internaţionale privind Comerţul, organizată în anul 2006 de Academia de Studii Economice din Bucureşti (Purcărea, 2006), începea de la legătura dintre proximitatea temporală a debutului proceselor de tranziţie în Europa Centrală şi de Est cu un accent pus - la nivelul Comunităţii Europene - pe nevoia de a examina specificul distribuţiei (octombrie 1989) şi accentul pus pe contribuţia posibilă a sistemului distribuţiei la integrarea şi stimularea unei economii de consum prin formele dinamice de distribuţie (martie 1991). Este recunoscut faptul că modernizarea comerţului în Europa Centrală şi de Est este importantă pentru integrarea economică a ţărilor, fiind necesară dezvoltarea structurilor logistice de distribuţie adaptate nevoilor locale (Purcărea, 1998).

Începând cu 1990, numeroşi lideri de întreprinderi de distribuţie din vest se întrebau ce atitudine comercială ar trebui să adopte în faţa neliniştilor politice, economice şi sociale cu care se confruntă ţările din Europa Centrală şi de Est. Întrebarea de fond era dacă este posibil să faci implanturi comerciale productive pe termen mediu în aceste ţări care se deschid faţă de consum după decenii de privaţiuni.

Introduction A study presented by us on the

occasion of the 2006 International Conference on Commerce organized by the Academy of Economic Studies in Bucharest (Purcarea, 2006), began from the ascertainment of a temporal proximity of the debut of the transition processes in Central and Eastern Europe with a focus – at the European Community level – on the need to examine the specifics of distribution (October 1989) and emphasis on the possible contribution of the distribution system to the integration and stimulation of a consumption economy through the dynamic forms of distribution (March 1991). It is acknowledged, in fact, that the modernization of trade in Central and Eastern Europe is important for the economic integration of the countries, the development of the distribution logistics structures adapted to local needs being required (Purcarea, 1998).

Starting in 1990, numerous leaders of western distribution enterprises wondered what commercial attitude they should adopt in the face of the political, economic and social turmoil with which Central and Eastern European countries were being confronted. The basic question was whether it is possible to make commercial implants lucrative in the medium term in these countries which are opening up to consumption after decades of privation.

The logistics of merchandise AE

Nr. 24 • Iunie 2008 11

Răspunsul la această întrebare a fost considerat afirmativ atât timp cât sunt luate în considerare realităţile specifice (Wegnez, 1998). De fapt, Congresul Internaţional al A.I.D.A. din 2003 (Florenţa, Italia) a confirmat prin vocea lui Christophe Lafougere, Director GIRA, France (“Cum va arăta distribuţia în cele zece noi state membre ale Uniunii Europene”): perioadele de schimbare rapidă sunt momentul ideal pentru a penetra noi pieţe; nu a fost nevoie să se treacă prin fazele dezvoltării retailului din Europa de Vest; pieţele se mişcă direct către capul cozii: hipermarketuri, centre de shopping, supermarketuri orientate spre discount de proximitate/soft.

Care este situaţia pe piaţa românească? Ce se întamplă la nivelul parteneriatului dintre producător şi distribuitor şi în ce măsură beneficiază consumatorul român de evoluţiile înregistrate în acest cadru? Acestea sunt întrebări actuale nu numai în România, dar şi la nivel european. 1. România, o piaţă importantă pentru

marile lanţuri de distribuţie România a confirmat poziţionarea

sa ca piaţă importantă pentru marile lanţuri de distribuţie, fapt dovedit atât de investiţiile efectuate în ultimii ani, cât şi de proiectele în curs şi de intenţiile exprimate în ceea ce priveşte perioada care urmează.

România a recuperat, în anii care au trecut, o parte din golul înregistrat din punct de vedere al dezvoltării pieţei de retail (chiar dacă există încă o semnificativă reţea intermediară de mici magazine şi chioşcuri). Promotorul dezvoltării reţelelor de retail a fost comportamentul consumatorului, în provocatorul context al relaţiei dintre impactul marketingului asupra consumatorului şi impactul consumatorului asupra strategiilor de marketing (Purcărea, 2007).

The answer to this question was considered affirmative as long as the specific realities are taken into consideration (Wegnez, 1998). In fact, as the International A.I.D.A. Congress of 2003 (Florence, Italy) has confirmed by the voice of Christophe Lafougere, GIRA Director, France (“What will distribution be like in the 10 new member states of the European Union”): periods of fast change are the ideal moment to penetrate new markets; there was no need to pass through the phases of West European retail development; the markets are moving straight to the head of the queue: hypermarkets, shopping centres, proximity/soft discount oriented supermarkets.

Which is the situation on the Romanian market? What is happenning at the level of the partnership between producer and distributor and to what extent does the Romanian consumer benefits from the evolutions recorded within this framework? These are current questions not only in Romania but also at European level. 1. Romania, an important market for

the large distribution chains Romania has confirmed its

positioning as an important market for the large distribution chains, a fact proven by the investments in the past years but also by the projects in course and by the intentions that have been declared for the following period.

In the past years Romania has recovered some of the gap registered from the viewpoint of the development of the retail market (even if there was another significant intermediary network of small shops and kiosks). The promoter of the development of retail networks has been the consumer behaviour, within the challenging framework of the relation between marketing’s impact on consumer and consumer’ impact on marketing strategies (Purcarea, 2007).

AE Logistica mărfurilor

Amfiteatru Economic 12

Noile formate - cash&carry (înlocuind angrosiştii), supermarket (reprezentând principalul tip de unitate de retail; cel mai mare ritm de creştere fiind înregistrat la vânzările de produse alimentare, urmate de vânzările de produse nealimentare), hypermarket (oferind o gamă maximă de produse şi o bună performanţă în materie de discount) şi discount - au remodelat imaginea comerţului intern.

În prezent, numeroase lanţuri de distribuţie cu renume activează pe piaţa românească: Metro (începând cu cash & carry, ulterior şi Praktiker şi de curând şi Real Hypermarket ), Carrefour, Auchan, Louis Delhaize (Cora, Mega Image, Profi), Rewe (Selgros/cash & carry, Billa, XXL Mega Discount), Intermarche, Bricostore, Kaufland (de remarcat apariţia în Bucureşti, sectorul 3, a Power Centerului Kaufland) etc., fiecare având o reţea de magazine dezvoltată în concordanţă cu piaţa ţintă şi trăsăturile specifice ale grupului. Intrarea lor pe această piaţă a fost determinată de potenţialul în continuă creştere şi de posibilităţile oferite. Această evoluţie a avut ca rezultat atragerea de noi investiţii, atât ale companiilor existente pe piaţă, cât şi ale altor companii internaţionale. Intrarea unor noi competitori pe piaţa de retail din România, precum Auchan sau Ikea şi intenţiile de extindere crescânde ale celor deja existenţi pe piaţă au stimulat sporirea concurenţei.

În anul 2003 s-a creat şi Asociaţia Marilor Reţele Comerciale (AMRCR), din care faceau parte: Flanco, Artima (achiziţionat ulterior de Carrefour), Bricostore, Cora, Diverta, DoMo, La Fourmi, Mega Image, Mobexpert, Praktiker, Profi, Selgros, Univers’all (achiziţionat ulterior de Carrefour).

The new formats – cash &carry (replacing wholesalers), supermarket (representing the main type of modern retail outlet; the biggest rhythm of growth being recorded at food sales, followed by the non-food sales), hypermarket (offering maximum product range and good discounting performance) and discount have remodelled the image of the domestic trade.

At the moment, numerous well-known distribution chains are actively participating on the Romanian market: Metro (beginning with cash&carry, following Praktiker and recently Real Hypermarket), Carrefour, Auchan, Louis Delhaize (Cora, Mega Image, Profi), Rewe (Selgros/cash & carry, Billa, XXL Mega Discount), Intermarche, BricoStore, Kaufland (it is to be noted the appearance in Bucharest, 3 rd District, of Kaufland Power Center) each having a network of shops developed in accordance with the target market and the specific features of the group. Their entering this market was determined by the continuously increasing potential and the possibilities offered. This evolution resulted in attracting new investments coming from existing companies on the market as well as other international companies. New competitors on the Romanian retail market, such as Auchan or Ikea and the increasing expansion intentions of those competitors already on the market have stimulated the increase of competition.

In 2003, the Large Commercial Networks Association was set up, which included: Flanco, Artima (later acquired by Carrefour), Bricostore, Cora, Diverta, DoMo, La Fourmi, Mega Image, Mobexpert, Praktiker, Profi, Selgros, Univers’all (later acquired by Carrefour).

The logistics of merchandise AE

Nr. 24 • Iunie 2008 13

Se cuvine a remarca totodată şi dezvoltarea lanţurilor de distribuţie specializate (produse farmaceutice, cărţi, muzică, electronică, mobilă, modă, auto etc.), cum ar fi: Sensiblue, Diverta, Flanco, Flamingo, Altex, Global Net, Mobexpert etc.

Marii retaileri au acordat o atenţie deosebită capitalei României, Bucureşti, în ceea ce priveşte deschiderea de supermarketuri şi hypermaketuri (a se vedea tabelul 1: Principalele lanţuri de distribuţie din România, Universitatea Româno-Americană, TOEMM, februarie 2008), fapt explicabil prin raportarea atât la populaţia oraşului (1,9 milioane de locuitori), cât şi la importanţa sa în calitate de centru economic, social şi politic.

Cum însă terenul disponibil pentru acest gen de dezvoltări s-a redus considerabil (iar problema echilibrului între „marea distribuţie” şi comeţul tradiţional rămâne; comerţul tradiţional dominând încă în materie de bunuri de consum cu mişcare rapidă, deşi formatele moderne sunt în expansiune), creşte vertiginos orientarea spre provincie, un mai mare interes pentru dezvoltatori prezentând nu numai oraşele mari - cum sunt Constanţa, Timişoara, Cluj, Sibiu, Iaşi, Piteşti, Galaţi - ci şi cele cu o populaţie mai mare de 70.000 de locuitori.

Competiţia dintre marii retaileri, ca şi între cei mici (care devin tot mai conştienti de importanţa valorificării marketingului de relaţie în contextul constrângerilor bugetare) şi cei mari devine tot mai acerbă, acest lucru fiind reflectat şi de tehnicile de marketing utilizate.

It is worth mentioning the development of specialized distribution chains (pharmaceutical products, books, music, electronics, furniture, fashion, auto, etc.) such as: Sensiblue, Diverta, Flanco, Flamingo, Altex, Global Net, Mobexpert etc.

The large retailers have given special attention to Bucharest, Romania’s capital, in what concerns the opening of supermarkets and hypermarkets (see Table nr. 1: The Main Distribution Chains in Romania, Romanian-American University, TOEMM, February 2008), fact that can be explained by referring to both the population of the city (1,9 millions inhabitants) and its importance as an economic, social and political centre.

As the land available for such developments has been considerably reduced (and there remains the problem of the equilibrium between the large distribution chains and traditional commerce; traditional commerce still dominates in terms of fast pace consumer goods, although modern formats are expanding), the orientation towards province is growing very rapidly, a higher interest for creators consisting of not only the large cities – like Constanţa, Timişoara, Cluj, Sibiu, Iaşi, Piteşti, Galaţi – but also those having a population of over 70.000 inhabitants.

The competition between big retailers, as well as between the small retailers( which are becoming more and more aware of the importance of valuing relationship marketing in the context of budget constraints) and big retailers are becoming more and more bitter, which is also reflected by the marketing techniques that are used.

AE Logistica mărfurilor

Amfiteatru Economic 14

Principalele lanţuri de distribuţie din România

(The Main Distribution Chains in Romania) Tabelul 1

Sursa: Universitatea Româno-Americană, TOEMM, februarie 2008 (Romanian-American University, TOEMM, February 2008)

Nr. de magazine (No. of stores)

Nr. (No.)

Nume

(Name)

Grup

(Group)

Format

(Format)

Total (Total)

Bucureşti (Bucharest)

Anul intrării pe piaţa

românească (Year of

entry into the Romanian market)

1 Carrefour Hyparlo Group Hypermarket 10 5 2001 2 Cora Louis Delhaize Hypermarket 3 2 2003 3 Real Metro Group Hypermarket 13 1 2006 4 Auchan Auchan Group Hypermarket 3 1 2006 5 Pic Grup Pic Hypermarket 4 0 2004 6 Metro Metro Group Cash&Carry 23 4 1996

7 Selgros Rewe Zentral AG

Cash&Carry 17 3 2000

8 BricoStore BricoStore Do It Yourself

9 4 2002

9 Praktiker Metro Group Do It Yourself

14 2 2002

10 Spar - Hypermarket

Spar Hypermarket 1 0 2006

11 Spar - Supermarket

Spar Supermarket 13 0 2006

12 Billa Rewe Zentral AG

Supermarket 25 3 1999

13 Mega Image Louis Delhaize Supermarket 18 15 1994

14 G’Market GimRom Holding

Supermarket 5 3 1999

15 Interex Intermarche Supermarket 9 0 2001 16 Profi Louis Delhaize Discounter 44 0 1995 17 Plus Tengelmann Discounter 50 3 2005 18 Kaufland Lidl & Schwarz Hypermarket 31 2 2005

19 Penny Market Rewe Zentral AG

Discounter 40 1 2001

20 Penny Market XXL

Rewe Zentral AG

Discounter 5 1 2001

21 Artima (Carrefour)

Carrefour Supermarket 21 0 2001

22 Altex Grup Altex Specialised store

125 11 1992

23 Domo Domo Specialised store

110 11 1994

24 Flanco International

Flanco International

Specialised store

110 11 1992

25 Cosmo Cosmo Specialised store

78 9 1998

The logistics of merchandise AE

Nr. 24 • Iunie 2008 15

Un trend care confirmă această

stare de fapt este efortul marcant de diferenţiere, fie prin creşterea volumului exclusivităţilor puse în vânzare, fie prin combinaţia dintre vânzările offline şi cele online. În acest ultim caz se ţine pasul cu evoluţia comportamentului consumatorilor, tot mai mulţi dintre aceştia (tot mai exigenţi din punct de vedere al considerării raportului calitate-preţ şi a serviciilor conexe oferite) studiind deja ofertele online (volumul de publicitate online sporeşte; modelul de afacere este în plină schimbare tinzând catre cel vestic), chiar dacă iau deciziile tot în supermarket sau hypermarket.

Un alt trend din ce în ce mai vizibil în ultimii doi ani este dezvoltarea accelerată a brandurilor de distribuitor (produse alimentare, electrocasnice, îmbrăcăminte), care încep să câştige încrederea consumatorilor, fidelizându-i prin aceste branduri proprii, oferite de marile magazine (în cazul magazinelor de tip discount ponderea acestor branduri proprii în totalul produselor oferite este mult mai mare) şi furnizate, în cea mai mare parte, de producători autohtoni (care respectă standardele de calitate conform caietelor de sarcini). Principalul element de atracţie pentru consumatori este preţul mai scăzut (produse alimentare, bunuri de consum de unică folosinţă, electrocasnice), comparativ cu al altor produse din gama respectivă, în condiţiile garanţiei privind calitatea. Pentru ca acest preţ să fie scăzut nu se recurge la o promovare agresivă (organizarea de prezentări de mostre în magazin, în diferite perioade; sampling-uri efectuate în magazine şi promovare prin pliante trimise clienţilor potenţiali, cum sunt, de exemplu, cei din categoria HoReCa; cât priveşte ambalajul, acesta este, de regulă, modest).

A trend that confirms this state of facts is the important effort of differentiation, either through increasing the volume of products that are sold with a character of exclusivity, either by combining offline and online sales. In the last case, a special emphasis is placed on the evolution of consumer behaviour, an increasing number of consumers (more and more strict from the point of view of considering the quality-price ratio and the related services offered) already studying online offers (the volume of online publicity is growing; the business model is changing aiming at the Western version), even if they are still making decisions in the supermarket or hypermarket.

Another apparent trend in the last two years is fast development of distribution brands (food products, labor-saving devices, clothes), which start to gain the trust of consumers, making them more loyal through these personal brands, offered by the large shops (for discount shops, the weight of these personal brands in the overall amount of products offered is much bigger) and largely supplied by local producers (which respect the quality standards according to the work instructions). The most important point for consumers is the lowest price (food products, one-use consumer goods, labor-saving devices) compared to that of other products from the same range of products, in the conditions of the guarantee concerning the quality. For that price to be low, the aggressive promotion is not applied (organizing sampling presentations in the shops, at different times; samplings carried out inside the shops and promotion through folders and magazines sent to potential clients, like, for example, those from the category HoReCa; in what concerns the packaging, this is, most times, modest).

AE Logistica mărfurilor

Amfiteatru Economic 16

2. Evoluţii recente pe piaţa românească

de retail Numai în anul care a trecut “marea

distribuţie” s-a îmbogăţit cu 152 de magazine, pe primul loc aflându-se cele din zona discounterilor (tendinţa menţinându-se şi în anul în curs). Astfel, la magazinele din acest ultim tip s-a mai adaugat un număr de 63 de unităţi (cele mai multe - 20 - Penny Market, urmat de Profi cu 19, Plus Discount cu 16 şi MiniMAX cu 8), în timp ce la supermarketuri încă 36, iar la hypermarketuri încă 29, plus încă 3 unitati în segmentul cash&carry (Selgros).

Se impun şi următoarele precizări: faptul că prin achiziţia Artima (supermarket), Carrefour (trecere la abordare multi-format) a fost reţeaua cu cel mai mare numar de magazine adaugate, el dechizând şi patru noi unităţi tip hypermarket (Bucureşti, Cluj-Napoca, Iaşi, Brăila); Kaufland a deschis 14 unităţi, mai mult cu 4 faţă de cifra anunţată iniţial); retailerul olandez Spar a deschis doar 6 unităţi din cele 20 anunţate; hypermarketul Real a intrat şi pe piaţa Capitalei, Bucureşti; Auchan a mai crescut numărul unităţilor cu 4; lanţul de hypermarketuri autohton Pic a ajuns la 4 unităţi (deschizând la Brăila şi Oradea; pentru anul în curs a anunţat deja deschiderea a încă 2); s-au consolidat şi unele reţele de magazine locale (Ethos – care a anunţat deja pentru anul 2008 şi investiţii green-field; Fidelio; Primăvara; Oncos; Trident – care intenţionează să deschidă în 2008, în afară de magazine format supermarket şi un hypermarket, precum şi un lanţ de magazine de proximitate; Wolf) etc.

Anul 2007 şi începutul anului 2008 a evidenţiat atât afectarea extinderii lanţurilor de magazine de lipsa terenurilor/spaţiilor disponibile, cât şi recurgerea la noi modalităţi de diferenţiere în atragerea şi menţinerea clienţilor, exemple: program non-stop

2. Recent evolutions on the Romanian

retail market Only in the last year the large

distribution chains have been enriched with 152 stores, on the first place being situated those in the area of discounts (the same tendency remained this year). This last category of stores added another 63 units (most of them -20 - Penny Market, followed by Profi with 19, Plus Discount with 16 and MiniMAX with 8), while in the case of supermarkets another 36, and hypermarkets another 29, plus another 3 units in the cash&carry segment (Selgros).

The following should be also mentioned: the fact that by acquiring Artima (supermarket), Carrefour (going for a multi-format approach) represented the network with the greatest number of stores that were opened, added to the units with the format mentioned earlier are the four new hypermarket-type units (Bucureşti, Cluj-Napoca, Iasi, Braila); Kaufland opened up 14 units, four more units than the initial number; Spar, the Dutch retailer, opened only 6 units out of the 20 announced; the hypermarket Real entered the Capital’s market, Bucharest; Auchan increased the number of units with 4; the local hypermarkets chain Pic reached 4 units (opening in Braila and Oradea; for the current year they announced the opening of another 2); some local networks of stores consolidated (Ethos – which already announced for the year 2008 green-field in; Fidelio; Spring; Oncos; Trident – which intends to open in 2008, together with the supermarket-format stores, also a hypermarket as well as proximity stores; Wolf) etc.

The year 2007 and the beginning of 2008 emphasized the impact on the extension of stores chains by the lack of available land/spaces, as well as finding new ways of differentiating in order to attract and retain clients: non-stop program

The logistics of merchandise AE

Nr. 24 • Iunie 2008 17

(Metro cash&carry la Bucureşti) sau mai lung, prin deschidere mai devreme (Real, în ţară); cafenele (Real la Timişoara; Billa la Baia Mare); franciza (Spar, în perspectiva apropiată); merchandising îmbunătăţit în raport cu diferite axe de inovaţie, îmbinarea dintre distribuţie şi merchandising sugerând în final tocmai răspunsul la perpetua cautare de către consumator a acelui loc cu personalitate cu care acesta doreşte să se identifice din nou şi din nou, dezvoltând chimia personalităţilor.

3. Recentul conflict între retaileri şi

producătorii români. Ce-i de făcut?

Particularitatea distribuţiei, având în vedere impactul local al fiecăreia dintre manifestările sale este de a materializa accesul la cerere printr-o multiplicare a punctelor de vânzare. Una dintre tendinţele pe care distribuţia le manifestă, din acest punct de vedere, este cercetarea sinergiilor şi a cooperărilor care pot conduce firmele de distribuţie de tipuri, forme şi mărimi diferite la punerea în practică a unor politici comerciale comune. Din momentul în care, prin efectul cumulativ al acestor acorduri accesul pe piaţă al concurenţilor este împiedicat, sunt aplicabile (în afara excepţiilor pe categorii sau individuale) regulile de interdicţie prevăzute de legislaţia în materie de concurenţă. Nu acelaşi lucru se întâmplă când aceste obstacole comportă restricţii între aceiaşi parteneri. Aceasta este consecinţa caracterului general al interdictiei restricţiilor concurenţei chiar în interiorul reţelei. O restricţie a concurenţei nu este legitimă datorită faptului că poate avea ca efect întărirea poziţiei concurenţiale a reţelei. Concurenţa între producători este, în general, mai vizibilă decât cea între distribuitorii aceluiaşi brand.

(Metro cash & carry in Bucharest) or longer hours, through opening earlier (Real, in the country); cafés (Real in Timisoara; Billa in Baia Mare); franchise (Spar, in perspective); improved merchandising regarding different axis of innovation, the mix between distribution and merchandising (Purcarea, 2007), ultimately suggesting the answer to the customer’s perpetual quest for finding that place with personality which he wishes to identify with over and over again, developing the chemistry of personalities.

3. The recent conflict between retailers

and Romanian producers. What

must be done? The particularity of distribution,

considering the local impact of each of its manifestations, is to materialise access to demand through a multiplication of the points of sale. One of the tendencies of distribution, from this point of view, is the research of the synergies and cooperation that can lead different types, forms and size distribution enterprises to put into practise certain common commercial policies. From the moment in which, through the cumulative effect of these agreements, the competition’s access to the market is hindered, the interdiction regulations provided by the legislation in the field of competition are applicable (other than the exceptions by category or individual ones). The same thing does not take place when these obstacles entail restraints between the same partners. This is the consequence of the general character of the interdiction of competition restraint, even inside the network. A competition restriction is not legitimate due to the fact that it can have the effect of strengthening the competitive position of the network. Competition between producers is, generally, more visible than that between distributors of the same brand.

AE Logistica mărfurilor

Amfiteatru Economic 18

Prima săptămână a lunii martie 2008 a fost marcată în România de un conflict, comentat pe larg, între producătorii români şi retaileri (Purcărea, 2008), în contextul în care Parlamentul European a adoptat, la Strasbourg, în deschiderea sesiunii plenare din data de 18 februarie 2008, o declaraţie scrisă privind investigarea şi remedierea abuzului de putere al marilor supermarketuri operând în Uniunea Europeană (UE), prin care se solicită Comisiei Europene să investigheze şi să propună măsuri potrivite (REF.: 20080215IPR21454;http://www.europarl.europa.eu/).

Începutul acestui conflict producători-retaileri a scos în evidenţă accentul pus pe comportamentul etic al retailerilor în contextul procesului de cumpărare al produselor de la furnizori, respectiv numeroasele taxe impuse furnizorilor pentru ca produsele acestora să ajungă pe rafturile marilor magazine, produsele deplasându-se prin lanţul ofertei a cărui eficacitate depinde de relaţiile de colaborare dintre participanţii care se confruntă şi cu o serie de constrângeri legale şi etice, cele legale rezultând, în general, din legislaţia concurenţială şi cea privind protecţia consumatorilor.

Să ne amintim că într-o scrisoare transmisă în 1998, Bernd Hallier, Director Executiv al EuroHandelsinstitut din Germania (EHI), Preşedinte al “EuroShop” şi al “European Retail Academy” (ERA, 2005), ulterior prezenţei domniei sale la Bucureşti în luna mai 1998 cu ocazia celui de-al 24-lea Congres Internaţional al A.I.D.A ( dânsul este şi membru al Consiliului A.I.D.A. Bruxelles), se precizează că economia de piaţă nu este ferită de lovituri şi nici nu reuşeşte pe deplin dacă nu este crescută o anumită bază de management şi, stare socială mijlocie.

The first week of March 2008 was marked in Romania by a conflict largely commented between retailers and Romanian producers (Purcarea, 2008), within the context that European Parliament has adopted in Strasbourg at the opening of the plenary session in February 18, 2008, a written declaration, on investigating and remedying the abuse of power by large supermarkets operating in the EU, calling upon the European Commission's DG Competition to investigate and propose adequate measures (REF.: 20080215IPR21454, http://www.europarl.europa.eu/).

The beginning of this conflict

producers-retailers emphasized the accent placed on the retailers’ ethical behaviour in the context of the buying process of products from suppliers, namely the numerous slotting fees imposed on the suppliers so that their products reach the store’s shelves, covering the supply chain’s path whose efficacy depends on the collaboration relationships between participants, who also confront with a series of legal and ethical constraints, the legal ones resulting, in general, from the competition legislation and the one concerning consumers protection.

Let us remember that in a letter

sent by Bernd Hallier, Managing Director of EuroHandelsinstitut Germany (EHI), President of the EuroShop Advisory Board and Executive Member of the European Retail Academy (ERA, 2005), subsequent to his esteemed presence in Bucharest in May 1998 for the 24th A.I.D.A. International Congress (the Professor also being a member of A.I.D.A.’s Council), it is specified that a market economy is neither sheltered from strikes nor can it fully succeed if a certain management base and middle social state is not grown.

The logistics of merchandise AE

Nr. 24 • Iunie 2008 19

Dr. Hallier s-a aplecat asupra corelaţiei dintre “aşa-numitele schimbări politice în multe ţări din Europa Centrală şi de Est şi necesitatea oamenilor de a trăi, de a consuma ca în Vest, punând faţă în faţă “radicalizarea în Vest” cu “radicalizarea în Est”, în contextul în care “forţele pieţei nu cad din cer, ci trebuie să fie dezvoltate cu grijă şi pe termen lung” (Purcărea, 1998). Întreprinderile care acţionează în comerţ - arată Dr. Hallier - se confruntă cu o serie întreagă de probleme: capacitatea managerială devine legată în mod deosebit de lupta operativă pentru supravieţuire zilnică; asigurarea punctelor de desfacere pentru a se putea construi un potenţial de debuşeu suficient de mare; lipsa de know-how în domeniul tehnologiei şi cercetării comerciale; lipsa mijloacelor financiare pentru introducerea tehnologiei moderne.

Dificultatea (observăm că Dr. Hallier l-a anticipat cu mai bine de un an pe profesorul de la Harvard, Jeffrey Sachs, n.n) constă în faptul că, în decursul unui deceniu şi cu resurse de capital reduse, trebuie realizat ceea ce în Vest s-a obţinut într-o evoluţie de peste 50 de ani. Salturile cuantice ale întreprinderilor vestice pentru Europa Centrală şi de Est sunt, mai ales în competiţia cu marile grupuri internaţionale, greu de realizat. Ca urmare a puternicei dinamici a comerţului, sublinia Dr. Hallier, se preiau multe întreprinderi din Europa Centrală şi de Est (E.C.E.) de către străini. Rezultă de aici o problemă grea pentru E.C.E. Dacă, comerţul originar din E.C.E. este supus competiţiei internaţionale, atunci aceste întreprinderi de comerţ pierd calitatea de solicitanţi pentru furnizorii naţionali. Comercianţii vestici nu vor lista însă suplimentar furnizorilor naţionali din E.C.E. Doar logica rabatului E.C.R. este cea care vorbeşte pentru o legatură de comandă şi nu pentru un sortiment împrăştiat.

Dr. Hallier concerned himself with the correlation between “the so-called political changes in many Central and Eastern Europe and the need for people to live and consume as in the West, placing face to face “the radicalization in the West” with “the radicalization in the East”, in the context in which “market forces do not fall from the sky, but must be developed with care and in the long term” (Purcarea, 1998). The enterprises that are active in trade – shows Dr. Hallier – are confronted with a whole series of problems: managerial ability becomes tied especially to an operative battle for day to day survival; ensuring points of sale to be able to build a sufficiently large outlet potential; the lack of technological and commercial research know-how; the lack of financial means to introduce modern technology.

The difficulty lies in the fact that what was achieved in the West in a 50 year evolution must be accomplished within a decade and with low capital resources. The quantum leaps of the Western enterprises for Central and Eastern Europe are difficult to accomplish, especially in the competition with the big international groups. As a result of the strong dynamics of trade, underlined Dr. Hallier, many enterprises in Central and Eastern Europe (CEE) are being taken over by foreigners. The result is a difficult problem for CEE. If the trade that originates in the CEE is subjected to international competition, then these trade enterprises lose the quality of petitioner for national suppliers. Western trade companies will not additionally list, though, the national suppliers from the CEE. Only the logic of the discount within ECR partnership is what speaks for an order connection and not a scattered assortment.

AE Logistica mărfurilor

Amfiteatru Economic 20

De aici rezultă o mare problemă pentru fiecare ofertant industrial şi cu aceasta şi pentru locurile de muncă în domeniul producţiei în E.C.E.

În mod evident, procesul de negociere producător-retailer depinde de puterea economică a lanţului de magazine. Un document OECD neclasificat DAFFE/CLP(99)21 (OECD, 1999) evidenţia faptul că: marii distribuitori cu amănuntul devin tot mai serioşi concurenţi ai furnizorilor din amonte şi se pot bucura de o putere substanţială de cumpărare; acolo unde un număr suficient de consumatori etalează un comportament de tipul “one-stop-shopping”, rezultatul va fi puterea semnificativă de cumparare pentru retaileri; protecţia concurenţilor nu este echivalentă cu protecţia concurenţei şi rămâne dificil de dovedit că un furnizor afectat actualmente este lipsit de alternativa echivalentă pentru a negocia cu un retailer acuzat.

În acelaşi an, în România apărea traducerea unei lucrări (Silbiger, 1999) în care se făcea trimitere şi la: semnificaţia spaţiului de pe raft; “unitatea de expunere a marfii” (stock keeping unit - SKU); faptul că retailerul urmăreşte să fie plătit pentru fiecare SKU utilizată; lupta pentru expunerea optimă a mărfurilor; plata sumelor de bani stabilite ad-hoc pentru rezervarea spaţiului pe raft, apărând noi bariere la intrarea pe piaţă. Tot în 1999, doi profesori americani (Aalberts şi Jennings, 1999), referindu-se la această practică a taxelor de raft devenită comună, lansau chiar întrebarea dacă este vorba de mită, de marketing de facilitare sau doar de concurenţă obişnuită.

The result is a big problem for each industrial supplier and with the latter also for work places in the production field in CEE.

Obviously, the producer-retailer negotiation process depends on the economic power of the stores’ chain. OECD’s unclassified document DAFFE /CLP (99) 21 (OECD, 1999) “underlined that: large multi-product retailers (“retailers”) are increasingly becoming serious competitors of the served up-stream suppliers and could enjoy substantial buyer power; where a sufficient number of consumers display “one-stop shopping” behaviour, the result will be significant buyer power for retailers ; protecting competitors is not equivalent to protect competition and it remains difficult to prove that an affected supplier actually lacks an equivalent alternative to dealing with an accused retailer.

In the same year, in Romania,

appeared the translation of a paper (Silbiger, 1999) in which there were some references made to: the signification of the space on the shelf; “the exposure unit of the merchandise” (stock keeping unit - SKU); the fact that the retailer seeks to be paid for each SkU used; the fight for optimal exposure of merchandise; the payment of the sums of money established ad-hoc for the booking of the shelf space, appearing new barriers to entry on the market. Still in year 1999, two American proffessors (Aalberts and Jennings, 1999), have analysed this common practice of slotting fees by launching the question if it is”bribery, facilitation marketing or just plain competition”.

The logistics of merchandise AE

Nr. 24 • Iunie 2008 21

Într-o altă lucrare de specialitate (Nestle, 2007) se subliniază că: profitabilitatea magazinului nu mai este doar o problemă de preţ plătit pentru un produs în raport cu costurile sale, ci de colectarea venitului pentru „închirierea” spaţiului pe raft; plasamentul produsului depinde de un sistem de „stimulente”, care sunt mai mari în funcţie de cât de bun este plasamentul; „acest sistem dezgustător pune magazinele alimentare de retail în control ferm al pieţei”, „mergând dincolo de o simplă problemă de cerere şi ofertă” etc.

Taxele de raft au fost analizate în timp din diferite perspective, ele apărând: la confluenţa «instrument economic eficient» (şcoala de gândire a „eficienţei”, accentuând cum pot taxele să sporească eficienţa în canalele de distribuţie) - «manifestări negative ale puterii de piaţă» (şcoala de gândire a „puterii de piaţă”, argumentând că taxele afectează concurenţa şi bunăstarea consumatorului (Bloom şi alţii, 1999); ca „doar un instrument promoţional nou reprezentând o parte a «plăcintei promoţionale» din care producătorii aleg atunci când alocă resursele de marketing” (Bone şi alţii, 2004).

La începutul lunii aprilie 1999 Office of Fair Trading - OFT (organizatie profesională independentă având sediul în Londra, binecunoscut reprezentant al familiei internaţionale a concurenţei) a arătat - după o investigaţie antitrust care s-a desfăşurat mai multe luni - că nivelul înalt al profiturilor supermarketului şi al preţurilor necesită continuarea investigaţiei. Conform unui comunicat de presă din 26 noiembrie 2004 al organizaţiei “Prietenii pământului” (www. foe.co.uk) OFT a fost solicitat de o serie de grupuri reprezentând consumatori, fermieri, mici furnizori, mici magazine şi interese de mediu înconjurător să deschidă o nouă investigaţie privind puterea de piaţă a marilor retaileri britanici

In another scientific approach

(Nestle, 2007), it is emphasized that:

„store profitability is not simply a matter

of the price charged for a product

compared to its costs” but also of

collecting revenue by „<< renting >> real

estate to the companies whose products

they sell”; this „unsavory system puts

retail food stores in firm control of the

market place”, and „goes beyond a simple

matter of supply and demand”.

The slotting fees have been analysed in time from different perspectives, appearing: at the junction between « efficient economic tool » (the „efficiency” school of thought”, stressing how the fees can enhance efficiency in distribution channels) - « negative manifestation of marketplace power » (the „market power” school of thought”, arguing that the fees damage competition and consumer welfare) (Bloom and others, 1999); „simply a new strategic promotional tool, part of a “promotional pie” from which manufacturers choose when allocating marketing resources” (Bone and others, 2004).

At the beginning of April 1999 the Office of Fair Trading - OFT (an independent professional organisation based in London and a well-known representative of the international competition family) has pointed out - after an antitrust investigation that was carried out over several months - that the high level of supermarket profits and prices requires further investigation. According to a press release from November 26 2004 of “Friends of the earth” (www. foe.co.uk) the OFT has been asked by a range of groups representing, consumers, farmers, small suppliers, small shops and environmental interests to open a new investigation over the market power of the leading Britain’s retailers

AE Logistica mărfurilor

Amfiteatru Economic 22

[spunând,de exemplu, că în studiul său din anul 2000, Comisia Concurentei - CC (CC conduce anchete în profunzime în ceea ce priveşte fuziunile, pieţele şi reglementarea principalelor industrii reglementate) a descoperit că vânzarea sub cost efectuată de marile supermarketuri a afectat micii concurenţi care au fost mai puţin abili în subvenţionarea încrucişată a pierderilor pe articolele alimentare cheie; CC a arătat că, prin subminarea competitivităţii unităţilor învecinate, s-ar reduce accesul şi alegerea consumatorilor şi că aceasta ar afecta în mod particular consumatorii cu venituri mici sau pe aceia cu mobilitate limitată]. Un an mai târziu, la sfârşitul lunii octombrie 2005, OFT şi-a reconsiderat regulile anterioare protejând sectorul de băcănie (apărând poziţia marilor lanţuri de supermarket britanice după o anchetă care a durat aproape doi ani) din investigaţia efectuată de CC şi a exprimat preocupări serioase în privinţa metodelor de lucru ale principalelor lanţuri de supermarket: Tesco, Asda, Sainsburys şi Morrisons.

În martie 2007 noi am aratat (Purcărea, 2007) că există o reală provocare pentru autoritatea de concurenţă: creşterea semnificativă a puterii de cumpărare (de la furnizori) a “marii distribuţii”, făcându-se trimitere şi la:

• investigaţia deschisă pe data de 9 mai 2006 în Marea Britanie de către OFT;

• raportul prezentat pe 15 ianuarie 2007 de GfK, împuternicit de Comisia Concurenţei;

• raportul privind supermarketurile, din anul 2000, al Comisiei Concurenţei (raport care concluziona că s-a dovedit că supermarketurile au abuzat de poziţia lor de putere şi s-au angajat în practici - au fost identificate 27 - care au afectat defavorabil competitivitatea furnizorilor,

[saying, for instance, that in its 2000 study the Competition Commission - CC (CC conducts in-depth inquiries into mergers, markets and the regulation of the major regulated industries) found that below-cost selling by the big supermarkets was damaging to smaller competitors who were less able to cross subsidize losses on key food items; the CC pointed out that, by undermining the competitiveness of neighbourhood outlets, accessibility and choice to consumers would be reduced, and that this would particularly affect consumers on low incomes or those with limited mobility]. A year later, by the end of October 2005, OFT has reconsidered its previous ruling protecting the grocery sector (defending the position of the leading Britain’s supermarket chains after an enquiry that lasted almost two years) from investigation by the CC and, expressed serious concerns over the working methods of the main supermarket chains: Tesco, Asda, Sainsburys and Morrisons.

In March 2007 we showed that

(Purcarea, 2007) there is a real challenge for the competition authority: the significant growth of buying power (from suppliers) of the large distribution chains, also rememberig the followings:

• investigation opened in UK on

may 9, 2006 by OFT; • the report presented on January

15, 2007 by GfK, imputernicit/ empowered by the CC;

• the CC 2000 report on UK supermarkets (concluding that there was evidence that supermarkets were abusing their position of power and engaging in 27 identified practices that adversely affected the competitiveness of suppliers, some practices operating against the public interest; to address these practices’

The logistics of merchandise AE

Nr. 24 • Iunie 2008 23

unele practici operând împotriva interesului public; pentru a se putea adresa acestor efecte defavorabile s-a recomandat introducerea unui cod de practici (intrat în vigoare la 17 februarie 2002) care să guverneze relaţiile supermarket-furnizor; în februarie 2004 OFT a publicat prima ediţie revăzută a codului, teama de consecinţele plângerii fiind identificată ca raţiune cheie pentru lipsa de eficacitate a codului.

De remarcat că, în context, Comisia Concurenţei a constatat că mulţi furnizori au ezitat în a veni cu dovezi (Purcărea, 2007).

În S.U.A., de exemplu, este binecunoscut faptul că furnizorii plătesc distribuitorilor taxe pentru plasarea produselor pe rafturile magazinelor (Food Marketing Institute, 2002). S-au reliefat astfel: schimbarea în materie de cheltuieli promoţionale, devenind mult mai greu să ajungi la consumatori prin intermediul mass media şi mult mai uşor în magazinele (începând prin a avea produsele plasate pe raft) unde consumatorii cumpără actualmente; opinia exprimată de Comisia Federală de Comerţ (Federal Trade Commission - FTC) că taxele de raft necesită o abordare caz cu caz, existând o “amplă autoritate în tratarea oricăror probleme care pot apărea” în această privinţă.

Concluzii

Putem spune astfel că astăzi există o certă nevoie de a făuri un ecosistem al conversaţiei, bazat pe comunicare interpersonală, dând naştere unei experienţe partajate, construind încredere şi întărind relaţiile între participanţi (atât la dezbaterea subiectului mediatizat, cât şi la lanţul ofertei), ieşind din rutina neconversaţională.

Scopul comun al unui parteneriat responsabil producător – distribuitor –consumator este soluţia la problema reală a afectării atât a consumatorului român (care trebuie să fie în centrul preocupării oricărei afaceri), cât şi a producătorului

adverse effects it was recommended that a code of practice (entered in force on February 17, 2002) be introduced to govern supermarket - supplier relationships; in February 2004 OFT has published the first revised edition of the code, the fear of complaint consequences being identified as the main reason for the lack of effectiveness of this code.

It is worth to note that CC found that many suppliers did hesitate in bringing evidence (Purcarea, 2007).

In USA, for instance, it is wellknown that the suppliers pay distributors slotting allowances for product placement on store shelves (Food Marketing Institute, 2002). It was underlined: the shift in promotional spending, becoming much harder to reach consumers through the mass media and much easier in the stores (starting by having products placed on the shelf) where consumers actually buy; the opinion expressed by the Federal Trade Commission (FTC) that the slotting fees approach need to be considered on a case-by-case basis, FTC already having “ample authority to deal with any problems that may arise”.

Conclusions We can therefore state that in the

actual context there is a certain need to: build a conversation ecosystem, based on interpersonal communication, resulting in a shared experience, building trust and strengthening the relationships between participants (both at the level of the debate regarding the general topic and at the level of the participants in the supply chain), getting out of the non-conversational routine.

The common goal of a mutually responsible partnership producer-distributor-consumer is the solution to the real problem of affecting both the Romanian consumer (which must be

AE Logistica mărfurilor

Amfiteatru Economic 24

român, pentru a putea beneficia de avantajele pieţei concurenţiale.

În confruntarea curentă cu eşecurile pieţei, o politică raţională pe termen lung, bine informată şi bine implementată, trebuie să ia în considerare şi evaluarea relaţiei producători români - “marea distribuţie” şi impactul acestei relaţii asupra bunăstării sociale. Bunăstarea consumatorului român - pe măsura evoluţiei comportamentului acestuia sub influenţa puternică a impetuoaselor demersuri comunicaţionale de marketing integrate - depinde din ce în ce mai mult de: comerţul desfăşurat de lanţurile de magazine, context în care se impune a acorda atenţia cuvenită oportunităţii reglementării adecvate; prestaţiile producătorilor români supuşi presiunii rezultate din concentrarea puterii de piaţă la “marea distribuţie”; raportul dintre utilizarea puterii de piaţă verticală (urmând dezvoltării mai întâi a puterii de piaţă orizontală) şi efectele de eficienţă şi impactul atât asupra consumatorului, cât şi asupra concurenţilor mici şi mijlocii (datorită sporirii comportamentului anticoncurenţial pe orizontală ca rezultat al exploatării avantajelor obţinute pe verticală).

Suntem toţi consumatori şi răspundem la mesaje de comunicare, consumul incluzând, suplimentar obiectelor tangibile, experiente intangibile, idei şi servicii. Oamenii de marketing se angajează în marketing personalizat şi personalizare de masă. Cunoaşterea se actualizează în mod continuu şi există o sofisticare crescândă a tehnicilor şi a metodelor prin combinarea abordărilor cognitive şi emoţionale în dezvoltarea materialelor de comunicare. Atât oamenii de marketing, cât şi reglementatorii se luptă cu aspectele etice şi sociale ale marketingului.

placed in the centre of each business) and the Romanian producer, in order to benefit from the advantages of the competitive market.

Within the current confrontation with the failures of the market, a long-term rational policy, well-informed and well implemented, must also take into account the evaluation of the relationship between the Romanian producers and the large distribution chains and its impact on the social welfare. The welfare of the Romanian consumer - in the context of the evolution of his behaviour under the strong influence of the impetuous integrated marketing communication steps - depends more and more on: the commerce undertaken by the stores chains, context in which we have to consider the opportunity of adequate regulation; the services offered by Romanian producers facing resulting pressures coming from the concentration of market power at the level of large distribution chains; the ratio between using the vertical market power (following the extension of horizontal market power) and the efficiency effects and the impact on both the consumer , and small and medium competitors ( due to the increase in the non-competitive behaviour on the horizontal as a result of the exploitation of vertically obtained advantages).

We are all consumers and we respond to communication messages, consumption including, in addition to tangible objects, intangible experiences, ideas and services. Marketers are engaging in personalized marketing and mass customization. Knowledge is continually updated and there is an increasing sophistication of research techniques and methods, by mixing cognitive and emotional approaches in the development of the communication materials. Both, marketers and regulators struggle with ethical and social aspects of marketing.

The logistics of merchandise AE

Nr. 24 • Iunie 2008 25

References [1] Purcărea, Theodor, The distribution of fast moving consumer goods on the Romanian

market: the challenge of the dynamic competitivity, „Proceedings of the the 2006 International Conference on Commerce” (ISBN-10 973-594-785-4 / ISBN-13 978-973-594-785-9), Academy of Economic Studies in Bucharest, March 27 - March 29, 2006, Vol. [2] Purcărea, Theodor, Racordarea României la circuitul manifestãrilor de specialitate ale

lumii distribuţiei, în “Marketing – Management”, nr.3/1998, pp. 6-7. [3] Wegnez, F. Leon, Reflexions des mots et des idees pour la gestion des entreprises de

distribution, C.B.D. - A.I.D.A., 1998, pp. 96-97. [4] Purcărea, Theodor, Distribuţie şi Merchandising, Editura Universitară Carol Davila, Bucureşti, octombrie 2007. [5] Purcărea, Theodor, Războiul raftului în economia conversaţiei sau dincolo de