Codul de practici si proceduri al autoritatii de marcare temporala ...

Revista Română de Statistică - Supliment nr. 5 / 2019

SUMAR / CONTENTS 5/2019REVISTA ROMÂNĂ DE STATISTICĂ SUPLIMENT

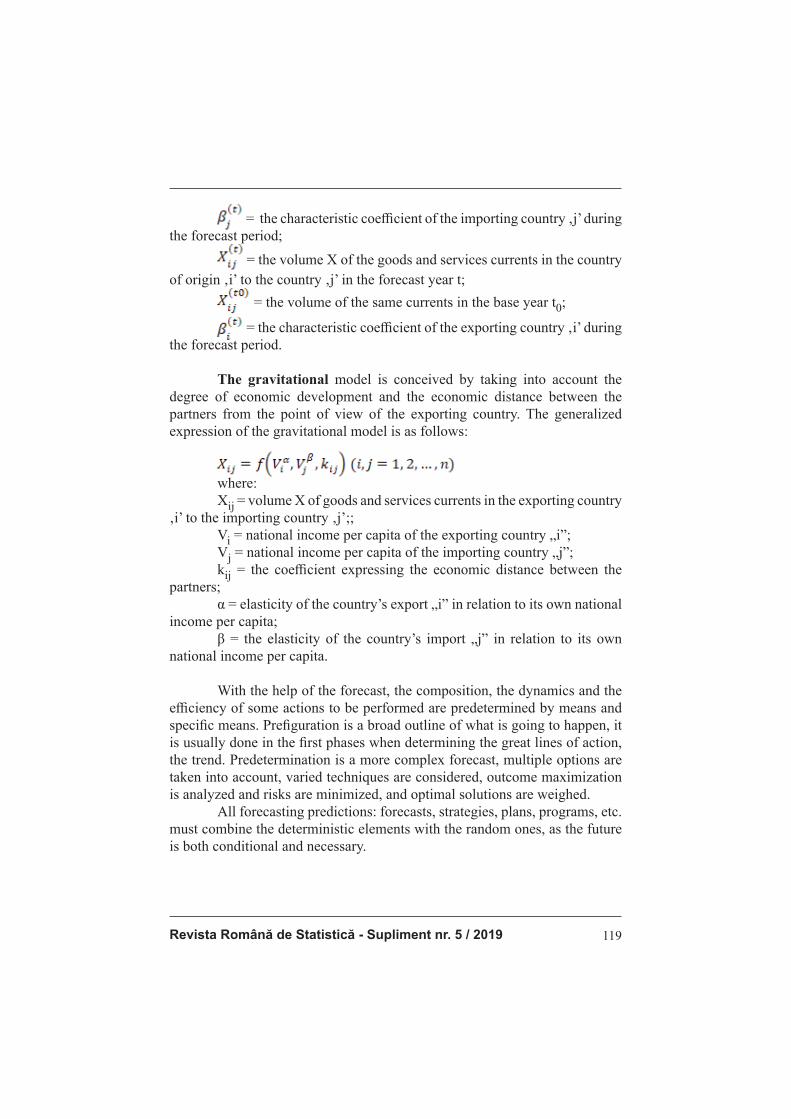

MODELUL GRAVITAȚIONAL UTILIZAT ÎN ANALIZELE ECONOMICE 3THE GRAVITATIONAL MODEL USED IN THE ECONOMIC ANALYZES 21Prof. Constantin ANGHELACHE PhDProf. Gabriela Victoria ANGHELACHE PhDAssoc. Mădălina-Gabriela ANGHEL PhD Gabriel-Ștefan DUMBRAVĂ PhD StudentOana-Ana-Maria SIMA Master Student

THE ANALYSIS OF MACRO-STABILIZATION OF THE FINANCIAL-BANKING SYSTEM 39György BODÓ PhD Student

MODEL DE ANALIZĂ A COMPORTAMENTULUI SOCIETĂȚILOR ÎN PERIOADA POST-CRIZĂ 48ANALYSIS MODEL OF THE POST-CRISIS BEHAVIOR OF THE COMPANIES 56Ștefan Virgil Iacob PhD

STATIC AND STRUCTURAL ANALYSIS OF GROSS DOMESTIC PRODUCT 64Tudor SAMSON Ph.D Student Alexandra PETRE (OLTEANU) PhD Student Cristian OLTEANU PhD StudentMarin-Marius GĂNCIULESCU Master Student

MIGRAȚIA ECONOMICĂ – ANALIZA FACTORILOR DETERMINANȚI AI ACESTEIA 73THE ECONOMIC MIGRATION - ANALYSIS OF ITS DETERMINANTS 83Olivia –Georgiana NIȚĂ PhD Student Alexandru BADIU PhD Student

THE BASEL AGREEMENTS – THE ANALYSIS OF THE BANKING RISKS 93Prof. Gabriela Victoria ANGHELACHE PhDGyörgy BODÓ PhD Student Radu STOICA PhD StudentDaniel GHERASIM Master Student

www.revistadestatistica.ro/supliment

Romanian Statistical Review - Supplement nr. 5 / 20192

ASPECTE TEORETICE PRIVIND ELABORAREA PREVIZIUNILOR MACROECONOMICE 100THEORETICAL ASPECTS REGARDING THE ELABORATION OF THE MACROECONOMIC FORECASTS 111Emilia STANCIU PhD Student Marius POPOVICI PhD Student Alexandra PETRE (OLTEANU) PhD Student Andreea-Ioana MARINESCU PhDGabriela Iuliana CARAIANI Master Student

THE ANALYSIS OF THE FIRM BASED ON THE STATISTICAL INDICATORS 121Prof. Radu Titus MARINESCU PhDDoina AVRAM PhD StudentCristian OLTEANU PhD Student Maria MIREA PhD Student

Revista Română de Statistică - Supliment nr. 5 / 2019 3

Modelul gravitaţional utilizat în analizele economice

Prof. univ. dr. Constantin ANGHELACHE ([email protected])

Academia de Studii Economice din București / Universitatea „Artifex” din București Prof. univ. dr. Gabriela Victoria ANGHELACHE([email protected])

Academia de Studii Economice din București

Conf. univ. dr. Mădălina-Gabriela ANGHEL([email protected])

Universitatea „Artifex” din București

Drd. Gabriel-Ștefan DUMBRAVĂ ([email protected])

Academia de Studii Economice din București Oana-Ana-Maria SIMA Master Student

Abstract Numeroase studii empirice au aratat ca fl uxurile comerciale urmeaza

principiile fi zicii referitoare la gravitatie: doua forte opuse determina nivelul

comertului bilateral intre tari, nivelul activitatii economice si a venitului,

pe de o parte si totalitatea barierelor afl ate in calea derularii comertului,

pe de alta parte. Acestea din urma includ: costurile cu transportul, politici

comerciale prohibitive, nesiguranta exportatorilor si importatorilor privind

evolutia diferitelor conditii de desfasurare a comertului cum ar fi evolutia

cursului valutar, diferentele culturale, existenta frontierelor nationale,

diversitatea preferintelor consumatorilor precum si diverse alte impedimente.

Analiza efectuată de autori evidențiază faptul că modelul gravitațional

asigură posibilitatea analizei comerțului internațional. Ecuațiile de tip

gravitațional au câteva caracteristici care asigură posibilitatea efectuării

studiilor empirice fi ind o ecuație bilaterală. Cu toate ca modelul gravitational

a avut, inca de la inceputurile utilizarii lui, un succes empiric care putea fi

cu difi cultate contestat, acest model a avut totusi parte, o perioada de timp,

si de critici care vizau lipsa unei fundamentari teoretice. Din acel moment a

fost din ce in ce mai mult acceptat faptul ca ecuatia gravitationala poate fi

extrasa pornind de la anumite ipoteze din modele teoretice, cum ar fi modele

ricardiene, modele de tip Heckscher-Ohlin sau modele de scara apartinand

Noi teorii a comertului international. Aceste trei tipuri de modele difera in

esenta prin modul in care este realizata specializarea produselor de catre

diferite tari.

Keywords: comerț internațional, regionalizare, import, export, curs

valutar, model gravitațional, modelul interlink. Classifi cation JEL: C50, F13, F40

Romanian Statistical Review - Supplement nr. 5 / 20194

Introduction Ecuatia gravitatiei este una dintre cele mai utilizate instrumente in studiile empirice privind problemele comertului international. Desi obiectivul principal al modelului gravitational este estimarea potentialului comercial pot fi mentionate si alte directii de utilizare ale acestui model cum ar fi : estimarea

costurilor pe care le implica frontierele dintre natiuni, explicarea evolutiei

ciclice a comertului international, identifi carea efectelor regionalizarii si nu

in ultimul rand explicarea efectului diferitelor variabile economice asupra

comertului cum ar fi spre exemplu, impactul pe care il are volatilitatea sau

evolutia cursului valutar asupra comertului s.a.m.d. Numarul variabilelor

explicative precum si varietatea formelor in care acestea sunt cuantifi cate au

cunoscut asemenea explozie in ultimii 20 de ani incat o simpla enumerare

a acestora devine destul de difi cila si risca sa fi e incompleta. Prin urmare,

in continuare este realizata o prezentare a celor mai importante utilizari ale

modelului gravitational impreuna cu variabilele cele mai semnifi cative fara a

avea pretentia unei prezentari complete.

Literature review Anghelache și Anghel (2018), precum și Corbare, Durlauf și

Hansen (2006) au analizat principalele metode și modele econometrice

utilizate în analizele economice. Anghelache (2008) a prezentat indicatorii

statistici aplicați în studiul comerțului international. O tema similară este

analizată de Anghelache și Anghel (2016). Anghelache, Mitruţ și Voineagu

(2013) au studiat aspecte fundamentale ale statisticii macroeconomice.

AnghelachePârţachi, Gonţa și Kralik (2012) au analizat elemente referitoare

la modelul gravitational. Arcidiacono și Miller (2011) au cercetat noțiuni

privind modelele dinamice. Benjamin, Herrard, Hanee-Bigot și Tavere (2010)

au analizat utilizarea modelelor econometrice în activitatea de previzionare.

Dascal, Mattas, Tzouvelekas (2002) au utilizat un model gravitațional în

vederea studiului infl uenței variației cursului valutar asupra comertului

exterior. Elliott, Müller și Watson (2015), precum și Phillips, Sun și Jin (2006)

au studiat aspecte ale testării modelelor econometrice. Johansen și Nielsen

(2010) s-au referit la inferența în cazul modelelor autoregresive. Müller (2007)

a studiat estimarea variațiilor de lungă durată. Newbold, Karlson și Thorne

(2010) au analizat elemente de bază ale statisticii economice. Pesavento și

Rossi (2006) au analizat aspecte ale eșantionării.

Metodologia cercetării Modelul gravitational pentru fl uxurile comerciale internationale isi

are originea in legea atractiei universale propusa de Newton (1687) care face

Revista Română de Statistică - Supliment nr. 5 / 2019 5

cunoscut si unanim acceptat faptul ca forta de atractie intre doua corpuri i

si j este direct proportionala cu produsul maselor si invers proportionala cu

patratul distantelor:

(1)

Mj = masa celor doua corpuri;

Dij = distanta dintre cele doua corpuri;

G = constanta gravitationala.

Asemanarea este izbitoare cu modelul gravitational in varianta sa

traditionala, asa cum este el prezentat in „Deardorff Glossary of International

Economics” cu urmatoarea ecuatie pentru estimarea exporturilor:

Tij = AYi Yj /Dij (2)

Unde:

Tij = exportul din tara i in tara j;

A = constanta;

Yi ,Yj = veniturile nationale;

Dij = distanta dintre cele doua tari.

Acest model, fără a avea initial o teorie economica de provenienta, si reprezentand mai mult o lege universala preluata din fi zica, ii este deopotriva atribuit lui Jan Tinbergen (1962) si Pentti Poyhonen (1963). Modelul a fost preluat si de alte stiinte sociale si utilizat pentru a simula fl uxurile turistice, fl uxurile de emigranti intre diferite tari, fl uxurile de cumparatori spre diferite centre comerciale s.a.m.d. presupunand bineinteles ca aceste fenomene au la baza aceiasi lege de atractie universala. Desi este difi cil a gasi un numitor comun tuturor lucrarilor de specialitate care au fost elaborate in acest domeniu, totusi varianta cea mai uzuala a modelului gravitational ar putea fi reprezentata prin urmatoarea ecuatie:

(3) unde: Xij - totalul exporturilor de la i la j; Yi ,Yj = veniturile tarilor; Li,Lj = populatia; Dij = distanta geografi ca intre i si j; Pij = gradul de acces pe piata de la i la j; Uij = variabila aleatoare normal si identic distribuita, i.i.d. N(0, ) Formula mai poste fi scrisa astfel : (4) unde: yi si yj = veniturile pe cap de locuitor a tarilor partenere astfel incat

Romanian Statistical Review - Supplement nr. 5 / 20196

Parametrii sunt in general estimati prin metoda celor mai mici patrate

pornind de la forma logaritmica a ecuatiei:

(5)

Metoda celor mai mici patrate nu este intotdeauna cea mai potrivita si

poate sa induca distorsiuni serioase in parametrii estimati datorita premiselor,

destul de restrictive, pe care se bazeaza aceasta metoda si care de multe ori nu

se mentin in conditii reale.

Ecuatiile de tip gravitational au cateva caracteristici care pot explica

succesul lor in studiile empirice. In primul rand, ecuatia gravitationala este

bilaterala. Ea explica variabila dependenta, de natura comertului exterior prin

combinarea unor variabile macroeconomice care descriu economia ambelor

tari partenere (marime, venit etc). Pe langa aceste marimi cu caracter bilateral

se adauga indicatorii privind costurile de transport intre cele doua tari si in

general variabile privind accesul pe piata.

In al doilea rand, ecuatia gravitatiei poate fi utilizata pentru a estima

atat factorii de volum cat si factorii privind natura fl uxurilor comerciale. Ultima situatie necesita introducerea unui indice al comertului intraindustrial ca variabila dependenta. Procentul comertului intraindustrial este in general determinat de similitudinea gradulul de inzestrare al tarilor partenere cu factori de productie care poate fi surprinsa si prin diferenta de venit pe cap de

locuitor dintre tari.

In al treilea rand, teoria ofera puternice temelii pentru un model bazat

pe indicatori cu grad redus de complexitate pentru care exista valori inregistrate

in cazul marii majoritati a tarilor si pe o perioada sufi cient de lunga. Aceasta

caracteristica este foarte utila atunci cand scopul este de a integra un numar

mare de tari in model iar baza de date statistice a acestora este limitata.

Modelul gravitational, data fi ind natura variabilelor independente, se

preteaza la analiza comertului international la un nivel ridicat de agregare.

Majoritatea modelelor au fost aplicate pe exporturile totale ale deferitelor tari.

Acest lucru nu exclude bineinteles utilizarea modelului gravitational pentru

date detaliate pe categorii de produse. Un exemplu recent este Gaulier si

Zignago (2004) care utilizeaza date cu un grad ridicat de detaliere pentru a

studia impactul factorilor de proximitate si al nivelului de specializare asupra

comertului.

Pornind de la un model de forma:

Revista Română de Statistică - Supliment nr. 5 / 2019 7

(6)

Unde:

α = constanta in timp si spatiu;

αt = efect fi x , specifi c fi ecarei perioade t si constant in plan teritorial;

αij - efect fi x, specifi c fi ecarei perechi ij si constant in timp;

PIBEit , PIBIjt = PIB-ul pe cap de locuitor al exportatorului respectiv

al importatorului;

PEi,,PIjt, = populatia exportatorului/importatorului;

Dij = distanta dintre cele doua tari;

εij = variabila aleatoare independenta si identic distribuita, de medie

1 si variatie constanta, i. i.d. (1,σ ) care prin logaritmare va deveni:

(7)

putem interpreta parametric β ca si elasticitati ale exportului functie

de factorii de infl uenta dupa rationamentul care urmeaza.

Prin diferentiere de gradul intai dupa variabila temporala t, ecuatia de

mai sus devine

(8)

Se cunoaste faptul ca diferenta logaritmilor aproximeaza ritmul de

crestere:

(9)

aproximarea fi ind cu atat mai puternica cu cat diferenta de la perioada

t-1 la perioada t este mai mica.

Prin urmare, coefi cientii βi i=1,4 arata modifi carea ritmului de

crestere al exporturilor la modifi carea cu 1 (100% in exprimare procentuala) a

ritmului de crestere in evolutia factorilor de infl uenta.

Pentru a obtine interpretarea coefi cientului β5, corespunzator unei

variabile pur teritoriale, se procedeaza in mod analog, insa de data aceasta

diferentele de ordinul intai se vor realiza in plan teritorial. Presupunem

ca perechile de tari ij sunt ordonate dupa un criteriu oarecare. Diferentele

perechilor consecutive pentru un an fi xat, t ar arata astfel:

Romanian Statistical Review - Supplement nr. 5 / 20198

(10)

Coefi cientul β5, va avea de aceasta data aceiasi interpretare ca si

ceilalti coefi cienti cu deosebirea cu variatia se manifesta in plan teritorial si

nu in plan temporal.

Ecuatia (6) nu poate fi estimata direct datorita coliniaritatii dintre

variabile teritoriale de distanta, Dij specifi ca fi ecarei perechi de tari si constanta

in timp si efectul fi x, specifi c fi ecarei perechi αij, ambele avand prin urmare

aceleasi proprietati si aceiasi variatie in profi l teritorial. Prin urmare, vom

inlatura alternativ cele doua variabile.

· Model de analiza structurii comertului international Suprapunerile comerciale (import si export in aceiasi industrie) sunt

examinate de Bergstrand (1989) si Hummels si Levinsohn (1995). Acestia

au construct indici comerciali bilaterali la nivel industrial in ceea ce priveste

comertul intra-industrial. Acesti indicatori sunt agregati la nivel national si

media ponderata a acestora este explicata folosind o ecuatie gravitationala.

O metoda alternativa utilizata pentru a diferentia comertul inter-industrial de

fl uxurile comerciale intra-industriale este explicat in Fontagne, Freudenberg

si Peridy (1998). In lucrarile amintite anterior se estimeaza ponderile in total

comert a tipurilor de comert diferentiindu-se in acest fel de marea majoritate

a modelelor de tip gravitational care estimeaza in general volumul total al

vanzarilor la extern.

Doua lucrari de data recenta care se inscriu pe aceasta linie sunt

Kandogan (2004) si (2004). In ultima lucrare este aratat faptul ca variabilele

explicative au efecte diferite asupra diferitelor componente ale comertului

exterior si ca pe masura ce economiile a doua tari si inzestrarea cu factori de

productie devine din ce in ce mai similara, volumul comertului intra-industrial

orizontal creste. In modelul specifi cat pentru comertul total variabilele sunt

introduse in forma logaritmata:

(11)

αi, γj reprezinta constanta (efectul fi x) aferenta fi ecarci tari, λt

reprezinta efectul asupra comertului pe care il are fi ecare an t (efectul ciclului

economic), δij efectul bilateral asupra comertului (relatia speciala dintre doua

Revista Română de Statistică - Supliment nr. 5 / 2019 9

tari care nu este surprinsa de variabilele explicative), iar celelalte variabile care

apar in model, in ordinea corespunzatoare sunt: distanta, productia cumulata

a celor doua tari, productia medie pe cap de locuitor, variatia absoluta a ratei

reale de schimb, rezerva valutara totala, similaritatea tarilor si diferenta de

inzestrare cu factori de productie. Ultimele doua variabile vor fi prezentate

in detaliu in cele ce urmeaza deoarece nu sunt direct observabile din datele

statistice ofi ciale.

Variabila SIM ia valoarea ln(0,5) atunci cand cele clouad tari obtin

productie identica, grad ridicat de similaritate si scade cand diferenta dintre

tari creste:

(12)

Diferenta de inzestrare cu factori de productie, RF, se calculeaza in

functie de stocul de capital K si forta de munca L a tarilor partenere i si j la

momentul t dupa urmatoarea formula:

(13)

Stocul de capital, K, se poate obtine cu ajutorul formarii brute a

capitalului fi x. Acest indicator ia valoarea 0 atunci cand tarile au aceiasi rata

de inzestrare cu factori de productie si creste data cu cresterea diferentei

dintre tari.

Acelasi tip de model a fost aplicat apoi pe componente ale importurilor

pentru a surprinde modul in care variabilele cauzale isi exercita infl uenta asupra respectivelor componente. Componentele comertului interior au fost identifi cate ca fi ind comertul intraindustrie, vertical si orizontal, precum si

comertul interindustrie. Comertul intraindustrie este calculat dupa formula:

(14)

unde:

Mkijt = importul tarii i din tara j in industria k.

Formula pentru comertul interindustrie este:

(15)

Romanian Statistical Review - Supplement nr. 5 / 201910

Importurile intraindustrie orizontale pot fi defi nite ca fi ind importurile

intraidustrie cu acelasi tip de produse p:

(16)

Unde:

Mkpijt = reprezinta importurile in tara i din tara j pentru produsul p din

industria k la momentul t.

Importul intraindustrie vertical, adica comertul in aceiasi industrie dar

cu produse diferite sau produse cu diferite grade de prelucrare, se calculeaza

astfel:

(17)

· Estimarea efectelor regionalizarii in comertul international Modelele gravitationale au fost utilizate in sens larg pentru a evalua

infl uenta masurilor de politica comerciala asupra fl uxurilor comerciale si in special infl uenta acordurilor de integrare regionala. Daca consideram exemplul a doua tari intre care s-a incheiat un acord de integrare regionala poate fi introdusa o variabila alternativa care ia valoarea 1 daca cele doua tari

se afl a la un momentul t in acord bilateral si 0 in caz contrar. Daca parametrul estimat al variabilei alternative este pozitiv si semnifi cativ atunci se poate

trage concluzia ca regionalizarea creeaza fl uxuri comerciale . Aceasta estimare poate fi facuta cu scopul de a simula potentialul comercial corespunzator

oricarei variante de integrare regionala intre diferite grupe de tari.

Un exemplu de model pentru care ia in considerare cele mai

importance acorduri regionale printre care si Uniunea Europeana este cel

utilizat de Soloaga si Winters (2001). Modelul utilizat ia in considerare pe

langa variabile traditionale si variabile alternative de genul celor amintite

anterior. Ecuatia testata empiric pe importurile a 58 de tari pe perioada 1980-

1996 este:

(18)

Valoarea importurilor tarii i din tara j sunt explicate in functie de PIB,

populatie, doua variabile de distanta, suprafata tarilor, variabile alternative

Revista Română de Statistică - Supliment nr. 5 / 2019 11

pentru existenta frontierei comune, tara insulara sau continentala si

proximitate culturala (limba comuna). Aceste variabile comune diferitelor

modele estimeaza volumul importurilor independent de existenta politicilor

regionale. Pe langa aceste variabile sunt introduse si variabile specifi ce prin

care se estimeaza efectele regionalizarii. Pk reprezinta o variabile alternativa

care ia valoarea 1 daca tara i sau j este participanta la acordul k, coefi cientul

bk arata cu cat este mai mare comertul daca ambele tari fac parte din acordul

k, coefi cientul mk arata cu cat sunt mai mari importurile tarii i care face parte

din acord fata de toti partenerii sai comerciali iar coefi cientul nk arata cu cat

sunt mai mari exporturile tarii participante la acordul k fata de toti partenerii

comerciali.

Alte exemple de studii sunt cel realizat de Cernat (2001), care a analizat

acordurile comerciale intre tarile in curs de dezvoltare in asa numitul comert

sud-sud, Zarzoso si Lehman (2002) aplicat pe cazul tarilor din Mercosur si

UE, Baier si Bergstrand (2002) s.a.m.d.

· Volatilitatile cursului valutar (unifi carea monetara) O lucrare semnifi cativa care realizeaza o comparatie a efectelor

realizarii uniunilor monetare cu efectele volatilitatii cursului valutar este ce

a lui Rose (2000) care arata ca exista un efect pozitiv al realizarii uniunii

monetare asupra comertului si un efect negativ a al volatilitatii cursului valuta

asupra acestuia. Factorii explicative care apar in ecuatia comertului bilateral,

propusa de Rose intre doua tari i si j, reprezinta atat variabile teritoriale cat si

variabile temporale:

(19)

Astfel fl uxurile comerciale bilaterale ־sunt explicate in functie de PIB (Y), populatie(Pop), distanta geografi ca (D), variabile alternative care arata

existenta sau inexistenta: granitei comune (Cont), limbii ofi ciale comune

(Lang), nationalitatii comune legaturilor de tip colonial (ComCol, Colony),

variabile alternative care arata apartenenta tarilor la un acord de liber schimb

(FTA) sau la o uniune monetara (CU) precum si de volatilitatea cursului

valutar nominal intre tarile partenere

· Estimarea comertului la nivel de produs Dascal, Mattas, Tzouvelekas (2002), pentru a analiza efectele

aprecierii cursului valutar, al cresterii productiei si al integrarii in spatiul

Romanian Statistical Review - Supplement nr. 5 / 201912

european asupra comertului exterior cu vin, au utilizat un model de tip

gravitational. Exporturile si importurile tarii i (membra UE) fata de tara j sunt

modelate cu ajutorul ecuatiilor:

(20)

Variabilele explicative sunt PIB-ul pe cap de locuitor Y, variabila de

distanta D, pretul Unitar P, rata de schimb E, indicele productiei de vin A si

apartenenta la Uniunea Europeana, EU. Este de remarcat faptul ca modelele

gravitationale aplicate la nivel de produs presupun introducerea unor variabile

de pret care nu sunt incluse in modelele pentru volumul agregat al comertului.

· Utilizarea modelului gravitational in analiza fl uxurilor

comerciale internationale

Estimarea potentialului comercial este cu certitudine punctul central

al utilizarii modelului gravitational. Aceasta metoda a fost folosita in special

pe cazul tarilor din Europa Centrala si de Est (Wang si Winters, 1991;

Havrylyshyn si Pritchett, 1991; Baldwin, 1993; Gros si Gonciarz, 1995;

Schumacher, 1995 si 1997; Festoc, 1996). Primul pas consta in selectarea

tarilor unde se presupune ca s-a atins potentialul comercial. Intr-o maniera

simetrica se considera fl uxurile comerciale bilaterale intre cele doua tari.

Se estimeaza apoi parametrii unei ecuatii de tip gravitational care explica

exporturile bilaterale in cadrul exemplului. Aceasta ecuatie este utilizata cu

scopul de a simula un comert bilateral natural intre oricare doua tari, pornind

de la variabile dependente cum ar fi : distanta dintre cele doua tari si populatia

celor doua tari. Aceste exporturi bilaterale obtinute in urma simularii sunt

comparate cu exporturile inregistrate, pentru a deduce potentialul exportului

bilateral. Aceasta metoda poate fi explicata atat la nivel macroeonomic cat si

la nivel industrial.

Una din variantele elaborate in cadrul Sectiei de Analiza a Pietei a

Centrului International de Comert (CIC) de catre L. Fontagne si J.M. Pasteels,

cunoscuta sub denumirea „TradeSim” versiunea a doua se incadreaza in

Revista Română de Statistică - Supliment nr. 5 / 2019 13

aceasta categoric de modele. Acest model a fost testat atat pentru date la

nivel sectorial cat si pentru fl uxurile totale si are urmatoarea formula generala

pentru estimarea potentialului comertului exterior:

(21)

unde:

i = tara exportatoare;

j = tara importatoare;

Xij = comertul intre tarile i si j;

Yi = PIB-ul tarii i;

di = densitatea populatiei tarii i;

cnfl ij = intensitatea confl ictului dintre cel doua tari;

ISDi = investitiile straine directe pe cap de locuitor pentru tara i lg -

diversitatea lingvistica in tara i;

tel ij = produsul densitatii liniilor telefonice in tarile i si j;

Dij = distanta dintre i si j;

B ij = daca tarile i si j sunt vecine (=1), daca nu (=0);

T ij = gradul de acces bilateral pe piata (pentru comertul intre i si j );

clt ij = etalonul bilateral pentru obiceiurile si traditiile pe care le au in

comun cele 2 tari.

Aceasta varianta reprezinta o extindere a modelului gravitational de baza

prin adaugarea unor noi variabile cum ar fi diversitatea lingvistica intre tarile

partenere, existenta unor granite comune, existenta unor momente importante de

intersectie in evolutia istorica, utilizarea unei monede comune, nivelul barierelor

tarifare si nu in ultimul rand infrastructura informationala. De obicei aceste

variabile sunt introduse ca variabile alternative in ecuatia gravitationala.

Modelul gravitational al CIC a fost dezvoltat in general pentru a

analiza potentialul comercial al tarilor in curs de dezvoltare si al economiilor

afl ate in tranzitie.

Veniturile si distanta sunt variabilele traditionale cel mai mult folosite

in modelele de tip gravitational. Pentru o cuantifi care a veniturilor in general

este utilizat Produsul Intern Brut total sau pe cap de locuitor in functie de

modelul specifi cat. Pe de o parte PIB-ul tarii exportatoare arata capacitatea de

productie si deci de export a acesteia. Pe de alta parte PIB-ul tarii importatoare,

ca reprezentare a veniturilor sale, arata capacitatea de cumparare a tarii

importatoare. Prin urmare PIB-urile ambelor tari sunt in mod direct corelate

cu volumul fl uxurilor comerciale. Utilizarea PIB-ului pe cap de locuitor este

justifi cata de faptul ca tarile cu un nivel de trai apropiat au preferinte sau

cerere similara. iar pentru tarile cu nivel de trai ridicat ponderea consumul de

bunuri de provenienta straina este mai mare.

Romanian Statistical Review - Supplement nr. 5 / 201914

In general sunt utilizate veniturile nominale transformate la rata de

schimb aferenta perioadei respective. Oricum, elasticitatea comertului functie

de venit poate fi alterata cand se iau in considerare economii in curs de dezvoltare

sau tari afl ate in tranzitie. Utilizarea PPP (Paritatii Puterii de Cumparare) poate de asemenea sa conduca la modifi cari a elasticitatii comertului in functie de

nivelul venitului. In cele din urma, s-a dovedit ca uneori PPP este mult mai

potrivita pentru a estima potentialul comercial pe termen lung, un orizont in

care evolutia ratei de schimb se apropie de echilibru. Pe termen scurt insa, este

mult mai potrivita utilizarea ratei de schimb nominale.

Un alt factor de infl uenta care, datorita importantei lui, a inceput sa apara frecvent in modelele de tip gravitational este gradul de accesibilitate al pietei. Deoarece modelul gravitational este prin constructie, in general, bilateral, este necesara o masura bilaterala a accesului pe piata care tine cont de toate regimurile preferentiale. 0 solutie este oferita de Bouet (2001) care propune un indicator care inglobeaza toate tipurile de taxe, tarife, contingente inclusiv masuri antidumping intr-o valoare unica. Aceste valori pentru fi ecare pereche de tari

partenere sunt cuprinse in baza de date MAC Map. Un tarif prea mare sau prea

mic, implica importuri prea mari, respectiv prea mici, iar contributia acestora la

protectia generala este redusa sau inregistreaza o crestere. Utilizand importurile

nationale ca ponderi se ajunge la o subevaluare a nivelului de protectie.

Pana la construirea bazei de date mai sus amintite au fost utilizate pe

scara larga variabile alternative pentru existenta acordurilor regionale. Pentru

ca in general tarile afl ate intr-un acord sunt in general si tari vecine sau tari cu un trecut istoric apropiat, exista riscul aparitiei multicoliniaritatii, situatie in care parametrii nu sunt unic determinati. Factorii culturali sunt deseori introdusi in modelul gravitational sub forma unor variabile alternative care, de regula, variaza, intre 0 si 1. Complexitatea aspectelor culturale este mult simplifi cata, in majoritatea

modelelor de tip gravitational, prin reducerea factorilor culturale la limba

nationala (fi e ofi ciala, fi e limba vorbita) si la legaturile de tip colonial. Date

extrem de utile pot fi preluate din „Exporters’ Ecncyclopedia” (Enciclopedia

Exportatorilor) editata de Dun & Bradstreet. De regula, in modelul gravitational traditional cheltuielile de tranzactionare si de transport sunt determinate de doua variabile: existenta unei granite comune si distanta fi zica intre cele doua tari. Asa cum se va putea

vedea in continuare, modele mai recente includ si alte variabile explicative

pentru cheltuielile de tranzactionare.

· Existenta granitelor comune este reprezentata in general de o

variabila alternativa care ia valoarea 1 in cazul in care tarile partenere sunt tari

vecine sau valoarea 0 in caz contrar.

Revista Română de Statistică - Supliment nr. 5 / 2019 15

Distanta este reprezentata de lungimea arcului de cerc dintre capitalele

sau principalele orase ale tarilor i si j. Latitudinea φ si longitudinea λ, celor

doua orase se transforma initial in radiani (II/360) iar apoi se calculeaza

distanta dupa urmatoarea formula:

(22)

unde:

z = 6367 (daca distanta este exprimata in km)

Loungani, Mody si Razin (2002) lanseaza ideea ca variabila

de distanta surprinde, pe langa cheltuielile propriu zise de transport, si

cheltuielile de informare si cercetare a pietei tarii de destinatie. Pentru a

surprinde in mod distinct efectul cheltuielilor de informare si cercetare autorii

au propus introducerea unei variabile care sa surprinda intensitatea structurii

informationale. Aceasta variabila se calculeaza ca produs al numarului de linii

telefonice pe cap de locuitor in cele doua tari partenere.

Un alt factor care infl uenteaza volumul comertului exterior este

calitatea infrastructurii de transport care poate fi apreciata prin procentajul

drumurilor pavate in lungimea totala a drumurilor sau ca densitate a lungimii

liniilor de cale ferata (lungime cale ferata raportata la suprafata). De obicei,

variabilele care exprima calitatea infrastructurii, fi e informationale fi e de

transport, sunt puternic corelate atat intre ele cat si cu PIB-ul pe cap de locuitor.

Prin urmare utilizarea lor in cadrul aceluiasi model ridica semne de intrebare.

Țarile mari au tendinta de a desfasura o buna pare a comertului pe

teritoriul tarii lor. Din aceasta cauza suprafata totala a unei tari poate fi folosita

pentru a explica volumul comertului directionat spre exterior.

Existenta Institutul de Cercetare a Confl ictelor Internationale din

Heidelberg deschide posibilitatea introducerii unei variabile de confl ict in

explicarea fl uxurilor comerciale. Conform defi nitiilor elaborate in cadrul

acestui institut exista patru forme majore care caracterizeaza intensitatea

confl ictelor internationale: confl ict latent, criza, criza severa si razboi carora

li se pot atribui valori de la 1 la 4 in ordinea cresterii intensitatii starii

confl ictuale. Variabila care se preteaza a fi introdusa intr-un model trebuie sa

fi e o combinatie intre intensitatea starii confl ictuale si durata ei.

Diversitatea lingvistica intr-o anumita tara este considerata un

stimul al comertului international. Indicele diversitatii lingvistice reprezinta

probabilitatea ca doua persoane alese la intamplare sa aiba limbi materne

diferite. Cu cat acest indice este mai apropiat de 1 cu atat este mai mare

diversitatea lingvistica in acea tara.

Romanian Statistical Review - Supplement nr. 5 / 201916

Gradul de pregatire intelectuala creeaza premise pentru comert, insa

este o variabila puternic corelata cu PIB-ul pe cap de locuitor si prin urmare

nu se recomanda introducerea celor doua variabile in acelasi model.

Fluxurile investitiilor straine directe pe cap de locuitor arata

atractivitatea de care se bucura o tara pe plan extern, arata gradul de

deschidere economica, stabilitatea mediului economic si legislativ, conduce

la dezvoltarea mediului tehnologic si a marketing-ului international. Toate

aceste premise si efecte ale ISD pot crea conditiile unui mediu prielnic pentru

dezvoltarea comertului exterior. Este necesara insa mentiunea ca impactul

ISD asupra exporturilor depinde si de natura investitiilor si de marimea tarii

gazda. Investitiile in tarile mari precum Rusia sunt directionate in primul rand

catre piata interna, spre deosebire de tari ca Estonia spre exemplu.

Pentru a crea o variabila explicative cat mai completa pentru fl uxurile

comerciale dintre doua tari partenere ar fi ideala utilizarea fl uxurilor de ISD

bilaterale dintre cele doua tari. Din pacate, fl uxurile bilaterale de ISD nu sunt

disponibile decat pentru tarile OCDE.

· Utilizarea modelului INTERLINK in generarea ecuatiilor comertului exterior

Modelul de echilibru global INTERLINK elaborat de OCDE este o

reprezentare a economiei mondiale si este format dintr-un set de submodele

pentru fi ecare tara membra OCDE impreuna cu ecuatiile de legaturi comerciale

si fi nanciare cu sase regiuni formate din tari non-membre OCDE. Prin cele peste

4000 de ecuatii pe care le contine, modelul INTERLINK trateaza economia

mondiala ca pe un tot integrat surprinzand aspecte multiple ale acesteia atat

din punctul de vedere al economiilor individuale cat si din punctul de vedere

al legaturilor internationale. Acest model, estimat pe date trimestriale, are un

rol operational in proiectiile si simularile pe care le realizeaza OCDE si care

sunt prezentate in publicatia „OECD Economic Outlook”.

Initial modelul INTERLINK a fost conceput ca un model al comertului

mondial care treptat s-a extins prin adaugarea unor relatii legate de cererea si

oferta agregate, salarii medii pe economie, preturile unor bunuri esentiale,

agregate monetare, rate ale dobanzii, cursuri de schimb valutar, situatii ale

bugetelor de stat si fl uxuri investitionale.

Relatiile de export, considerate in general ca fi ind in esenta

determinate de cerere, reprezinta comportamentul agentilor comerciali pe

o piata internationala care poseda un anumit grad de omogenitate si care

determina un comportament, intr-o anumita masura similar, al actorilor pe

piata internationala. Intr-un model al comertului international ne putem astepta

prin urmare ca parametrii care caracterizeaza comportamentul exportatorilor

Revista Română de Statistică - Supliment nr. 5 / 2019 17

pe o anumita piata sa prezinte un anumit grad de similitudine care poate sa

justifi ce abordarea comertului mondial printr-un sistem de ecuatii, impreuna

cu anumite restrictii care sa asigure consistenta comertului insumat al tarilor

individuale cu volumul cererii agregate la nivel mondial.

Setul ecuatiilor de export din cadrul modelului INTERLINK porneste,

ca de altfel multe alte modele din literature de specialitate, de la premisa unei

relatii inverse dintre performanta exportului si intensitatea competitivitatii pe

plan international. Performanta exportului unei tari este cuantifi cata ca si cota

de piata (volumul exportului raportat la cererea pietei de destinatie care la

randul ei este determinate ca o medie ponderata a importurile tarilor de pe

piata intenationala). Competitivitatea pe piata internationala este cuatifi cata

in termeni de preturi de export relative, preturile competitorilor din pietele

alternative fi ind ponderate si insumate.

Modifi carile competivitatii, cuantifi cate ca preturi relative, nu pot

sa explice evolutia performantei exporturilor in toata complexitatea ei. Prin

urmare, pe langa factorii de cerere (competitiviatatea mediului extern) este

utila introducerea unor elemente legate de calitatea produselor, de conditiile

de livrarea sau de distributie a acestora, adica a factorilor legati de oferta.

Aceste aspecte sunt insa mult mai greu de surprins intr-un model de natura

cantitativa. 0 alternativa, adoptata in cadrul INTERLINK, este modelarea

fl uctuatiilor care nu sunt explicate de competitivitatea preturilor, prin utilizarea unei functii de tendinta non-liniare. f (t) = exp(α(t – β)2) (23)

unde:

α < 0;

t = este variabila timp.

Decizia adoptarii unor astfel de functii a fost luata dupa ce in

prealabil a fost tatonata ideea utilizarii unor functii de tendinta liniare sau a

unor coefi cienti de elasticitate diferiti de unu care nu au putut insa surprinde

evolutia performantei exporturilor intr-un numar atat de divers de tari datorita

rigiditatii lor functionale. Functia nonliniara adoptata, prezentata anterior, are

o forma sufi cient de fl exibila si are proprietatea ca in timp tinde la 0 adica,

efectul ei asupra performantei exportului se anuleaza in timp.

Functia non-liniara are capacitatea de a surprinde modifi carile

performantei exporturilor care sunt legate de stadiul de dezvoltare al unei tari.

Schimbarile bruste de natura structurala, care implica trecerea de la exportul

de resurse primare la produse manufacturate iar apoi, intru-un stadiu mai

avansat la exportul de servicii sunt evidentiate intr-o prima faza de cresteri

exponentiale care se aplatizeaza pe masura maturizarii respectivei economii

nationale. Aceasta evolutia este insotita de fl uxurile de investitii straine directe

Romanian Statistical Review - Supplement nr. 5 / 201918

masive pentru aducerea mediului tehnologic dintr-o tara in curs de dezvoltare

la nivelul tarilor mai dezvoltate, din partea tarilor mai dezvoltate existand in

primul rand motivatia costurilor mai reduse ale fortei de munca. Noua teorie

a comertului care pune accentul pe importanta cresteri profi turilor bazate pe

economiile de scara si relatia dintre exporturi si rata de crestere a productiei

interne (Krugman 1989) justifi ca introducerea unor termeni legati de oferta

cum ar fi PIB-ul sau stocul de capital al tarii exportatoare. Functia de tendinta

non-liniara are rolul de a inlocui toti acesti factori si de a surprinde efectul

agregat al tuturor aspectelor legate de oferta.

Ecuatia estimata pentru fi ecare tara membra OECD si pentru fi ecare

din cele sase regiuni formate din tari non-membre OECD (printre care si

Europa Centrala si de Est) are urmatoarea formula:

(24)

ceea ce se mai poate scrie, pentru a face vizibila forma specifi ca unui

model de corectie, astfel:

(25)

unde:

∆ = diferenta de ordinul 1;

XMV = volumul exportului;

XMVMKT = cererea pe piata internationala;

XMPERF = XMV/XMVMKT = performanta exportului;

RPXM = pretul relativ ale exporturilor;

f(t) = trend non-liniar.

Procedura de estimare presupune in prima faza estimarea ecuatiei

pentru fi ecare tara luata individual prin metoda celor mai mici patrate iar apoi

efectuarea unor teste pentru semnifi catia coefi cientilor, pentru autocorelatii

in valorile reziduale (test de tipul multiplicatorului Lagrange), pentru

normalitatea valorilor reziduale, pentru corectitudinea modelului din punct de

vedere functional (testul RESET) si pentru prognoza si stabilitatea modelului

(testul Chow). In urma testelor efectuate ecuatiile sunt ajustate, iar unele pot fi

Revista Română de Statistică - Supliment nr. 5 / 2019 19

chiar eliminate. Se trece apoi la abordarea setului de ecuatii ca sistem, ecuatiile

avand coefi cienti comuni, fi xati in plan teritorial pentru toate variabilele mai

putin pentru functia de tendinta f(t). Datorita faptului ca in urma estimarii

sistemului cu ajutorul metodei celor mai mici patrate s-a obtinut o corelatie

semnifi cativa intre valorile reziduale in plan teritorial, adica intre valorile

reziduale corespunzatoare diverselor tari, s-a hotarat adoptarea metodei de

estimare SURE (Seemingly Unrelated Regression Estimation). Merita amintit

faptul ca tari recent integrate in UE care sunt si membre OECD (Ungaria,

Cehia, Polonia) ridica probleme in procesul de estimare datorita numarului

redus de date.

Romania nefi ind membra OCDE nu este surprinsa in setul de ecuatii

pentru comertul exterior din cadrul modelului INTERLINK ca tara individuala

ci doar membra a unei grupe de tari non-membre. Propuneri specifi ce pentru

modelarea comertului Romaniei, atat sub forma unor modele de corectie, cat

si sub alte forme, sunt facute in capitolul patru. Lipsa unui numar sufi cient de

date statistice va reprezenta si acest caz insa un obstacol in calea obtinerii unor

rezultate cu o semnifi catie statistica ridicata.

Conclusions O serie de elemente sunt preluate din studiile efectuate de mulți

cercetători, astfel încât modelul gravitațional a ajuns din punct de vedere

teoretic un model utilizabil în studiile comerțului internațional.. Așa depildă

se explică variabila dependentă, de natura comerțului internațional prin

combinarea unor variabile macro-economice. rezultă că ecuația gravitațională

poate fi utilizată cu succes pentru a estima atât factorii de volum cât și factorii

privind natura fl uxurilor comerciale. Teoria privind utilizarea acestui model

este bazată pe indicatori cu grad redus de complexitate pentru care există

valori înregistrate în majoritatea țarilor pe o perioadă sufi cient de lungă.

Apreciem că modelul gravitațional, prin natura variabilelor independente,

se pretează la analiza comețului internațional la un nivel ridicat de agregare.

Acest model poate fi utilizat și în analiza structurală a comețului internațional

pe categorii de produse sau chiar pe produse și servicii considerate. Autorii

evidențiază relațiile matematice utilizabile în cazul analizelor pe baza

modelului gravitațional.

References 1. Anghelache, C., Anghel, M.G. (2018). Econometrie generală. Teorie și studii de

caz, Editura Economică, Bucureşti

2. Anghelache, C., Anghel, M.G. (2016). Bazele statisticii economice. Concepte

teoretice şi studii de caz, Editura Economică, Bucureşti

Romanian Statistical Review - Supplement nr. 5 / 201920

3. Anghelache, C., Mitruţ, C., Voineagu, V. (2013). Statistică macroeconomică. Sistemul Conturilor Naţionale, Editura Economică, Bucureşti

4. Anghelache, C., Pârţachi, I., Gonţa E., Kralik, L. (2012). Gravitational Model for the Analysis of Commercial Flows, International Conference “Conjuncture and quality trends in the economic development of society”, April 26-28, 2012, Romanian Statistical Review, Supplement, 261-268

5. Anghelache, C. (2008). Tratat de statistică teoretică şi economică, Editura Economică, Bucureşti

6. Arcidiacono, P., Miller, R.A. (2011). Conditional Choice Probability Estimation of Dynamic Discrete Choice Models with Unobserved Heterogeneity. Econometrica, 79 (November 2011), 1823-1867

7. Benjamin, C., Herrard A., Hanee-Bigot, M., Tavere, C. (2010). Forecasting with

an Econometric Model, Springer 8. Corbare, D., Durlauf, S., Hansen, B. (2006). Econometric Theory and Practice

- Frontiers of Analysis and Applied Research, Cambridge University Press 9. Dascal, M., Mattas, K., Tzouvelekas, V. (2002). An analysis of EU wine trade:

A gravity model approach. International Advances in Economic Research, 8 (2), 135-147

10. Elliott, G., Müller, U.K., Watson, M.W. (2015). Nearly Optimal Tests When a Nuisance Parameter is Present Under the Null Hypothesis. Econometrica, 83, 771-811

11. Johansen, S., Nielsen, M. (2010). Likelihood inference for a fractionally

cointegrated vector autoregressive model, CREATES Research Papers 2010-24, School of Economics and Management, University of Aarhus

12. Müller, U.K. (2007). A Theory of Robust Long-Run Variance Estimation. Journal

of Econometrics, 141, 1331-1352. 13. Newbold, P., Karlson, L.W., Thorne, B. (2010). Statistics for Business and

Economics, 7th ed., Pearson Global Edition, Columbia, U.S 14. Pesavento, E., Rossi, B. (2006). Small–sample Confi dence Interevals for

Multivariate Impulse Response Functions at Long Horizons. Journal of Applied

Econometrics, 21 (8), 1135–1155 15. Phillips, P.C.B., Sun, Y., Jin, S. (2006). Spectral Density Estimation and Robust

Hypothesis Testing using Steep Origin Kernels without Truncation. International

Economic Review, 47, 837-894.

Revista Română de Statistică - Supliment nr. 5 / 2019 21

THE GRAVITATIONAL MODEL USED IN THE ECONOMIC ANALYZES

Prof. Constantin ANGHELACHE PhD ([email protected])

Bucharest University of Economic Studies / „Artifex” University of Bucharest

Prof. Gabriela Victoria ANGHELACHE PhD ([email protected])

Bucharest University of Economic Studies

Assoc. Mădălina-Gabriela ANGHEL PhD ([email protected])

„Artifex” University of Bucharest

Gabriel-Ștefan DUMBRAVĂ PhD Student ([email protected])

Bucharest University of Economic Studies

Oana-Ana-Maria SIMA Master Student

Abstract Numerous empirical studies have shown that trade fl ows follow the

principles of gravity-related physics: two opposing forces determine the

level of bilateral trade between countries, the level of economic activity

and income, on the one hand, and all the barriers to trade, on the other.

The latter include: transport costs, prohibitive trade policies, insecurity of

exporters and importers about the evolution of various trade conditions such

as the evolution of the exchange rate, cultural diff erences, the existence of

national borders, the diversity of consumer preferences and various other

impediments. The authors’ analysis highlights the fact that the gravitational

model ensures the possibility of international trade analysis. Gravitational

equations have several characteristics that make it possible to carry out

empirical studies being a bilateral equation. Although the gravitational

model had, since the beginning of its use, an empirical success that could

be challenged with diffi culty, this model had, however, for some time, also

criticism regarding the lack of a theoretical substantiation. From that moment

on, it has been increasingly accepted that the gravitational equation can be

extracted from certain hypotheses from theoretical models such as ricardian

models, Heckscher-Ohlin models or scale models belonging to New Theories

of International Trade. These three types of models diff er in essence by the

way in which product specialization is made by diff erent countries.

Keywords: international trade, regionalization, import, export,

exchange rate, gravity model, interlink model.

JEL Classifi cation: C50, F13, F40

Romanian Statistical Review - Supplement nr. 5 / 201922

Introduction The equation of gravity is one of the most used tools in empirical

studies on international trade issues. Although the main objective of the

gravitational model is the estimation of the commercial potential, other

directions of use of this model can be mentioned, such as: the estimation of

the costs that the frontiers between nations involve, the explanation of the

cyclical evolution of the international trade, the identifi cation of the eff ects

of the regionalization, and last but not least explaining the eff ect of various

economic variables on trade such as for example the impact of volatility or

the evolution of currency exchange on commerce and so on The number of

explanatory variables and the variety of forms in which they are quantifi ed have

experienced such an explosion over the past 20 years that a mere enumeration

of them becomes rather diffi cult and risks being incomplete. Therefore,

there is a presentation of the most important uses of the gravitational model

along with the most signifi cant variables without having the requirement of a

complete presentation..

Literature review Anghelache and Anghel (2018) and Corbare, Durlauf and Hansen

(2006) analyzed the main econometric methods and models used in economic

analyzes. Anghelache (2008) presented the statistical indicators applied in the

study of international trade. A similar theme is analyzed by Anghelache and

Anghel (2016). Anghelache, Mitruţ and Voineagu (2013) studied fundamental

aspects of macroeconomic statistics. AnghelachePârţachi, Gonţa and Kralik

(2012) analyzed elements related to the gravitational model. Arcidiacono

and Miller (2011) investigated concepts of dynamic models. Benjamin,

Herrard, Hanee-Bigot and Tavere (2010) analyzed the use of econometric

models in predictive activity. Dascal, Mattas, and Tzouvelekas (2002) used

a gravitational model to study the infl uence of exchange rate fl uctuations on

foreign trade. Elliott, Müller and Watson (2015), and Phillips, Sun and Jin

(2006) studied aspects of econometric models testing. Johansen and Nielsen

(2010) referred to inference in autoregressive models. Müller (2007) studied

the estimation of long-term variations. Newbold, Karlson and Thorne (2010)

analyzed basic elements of economic statistics. Pesavento and Rossi (2006)

analyzed aspects of sampling.

Methodology, data, results and discussions The gravitational model for international trade fl ows originates in the

law of universal attraction proposed by Newton (1687) which makes known

and unanimously accepted that the force of attraction between two bodies

Revista Română de Statistică - Supliment nr. 5 / 2019 23

i and j is directly proportional to the product of the masses and inversely

proportional to the square of the distances:

(1)

Mj = mass of the two bodies;

Dij = distance between the two bodies;

G = gravitational constant.

The similarity is striking with the gravitational model in its traditional

version, as it is presented in „Deardorff Glossary of International Economics”

with the following equation for estimating exports:

Tij = AYi Yj /Dij (2)

where:

Tij = export from country to country j;

A = constant;

Yi ,Yj = national income;

Dij = distance between the two countries.

This model, originally having an economic theory of origin, and

representing more of a universal law taken from physics, is also attributed

to Jan Tinbergen (1962) and Pentti Poyhonen (1963). The model was also

taken up by other social sciences and used to simulate tourist fl ows, migratory

fl ows between diff erent countries, buyers fl ows to diff erent shopping malls

s.a.m.d. assuming of course that these phenomena are based on the same law

of universal attraction.

Although it is diffi cult to fi nd a common denominator of all specialized

papers that have been elaborated in this fi eld, however, the most common

variant of the gravitational model could be represented by the following

equation:

(3)

where: Xij = total exports from i to j;

Yi ,Yj = country revenue;

Li,Lj = population;

Dij = geographic distance between i and j;

Pij = degree of market access from i to j;

Uij = normal and identically distributed random variable, i.i.d. N(0,

)

The formula can be written as follows:

(4)

where: yi and yj = income per capita of the partner countries so

Romanian Statistical Review - Supplement nr. 5 / 201924

Parameters are generally estimated by the smallest square method

based on the logarithmic form of the equation:

(5)

The smallest square method is not always the most appropriate and

can cause serious distortions in the estimated parameters due to the rather

restrictive premises on which this method is based and which often do not

remain in real terms.

Gravitational equations have several characteristics that can explain

their success in empirical studies. First, the gravitational equation is bilateral.

It explains the dependency variable, the nature of foreign trade by combining

macroeconomic variables that describe the economics of both partner

countries (size, income, etc.). In addition to these bilateral sizes, we add the

transport cost indicators between the two countries and, in general, market

access variables.

Secondly, the gravitational equation can be used to estimate both the

volume factors and factors related to the nature of commercial fl ows. The

latter situation requires the introduction of an index of intra-industrial trade

as the dependent variable. The percentage of intra-industrial trade is generally

determined by the similarity of the partner countries’ endowment with the

factors of production that can be surprised and by the per capita income gap

between countries.

Thirdly, theory provides powerful groundwork for a model based on

low-complexity indicators for which there are values for a large majority of

countries and for a suffi ciently long period. This feature is very useful when

the purpose is to integrate a large number of countries into the model and their

statistical database is limited.

The gravitational model, given the nature of the independent variables,

is suitable for the analysis of international trade at a high level of aggregation.

Most models have been applied to total exports of hardwoods. This does

not of course exclude the use of the gravitational model for detailed data by

product category. A recent example is Gaulier and Zignago (2004) that use

highly detailed data to study the impact of proximity factors and the level of

specialization on commerce.

Starting from a pattern of shape:

Revista Română de Statistică - Supliment nr. 5 / 2019 25

(6)

where:

α = constant in time and space;

αt = fi xed eff ect, specifi c for each period t and constant in the territorial

plane;

αij = fi xed eff ect, specifi c to each pair ij and constant over time;

PIBEit, PIBIjt = GDP per capita of the respective exporter and importer;

PEi,,PIjt, = the exporter / importer’s population;

Dij = distance between the two countries;

εij = the random and identically distributed random variable of mean

1 and constant variation, i. i.d. (1,σ ) which by logarithm will become:

(7)

we can interpret parameter β as the elasticity of export by infl uence

factors after the following reasoning.

By fi rst degree diff erentiation after the temporal variable t, the

equation above becomes

(8)

It is known that the logarithm diff erence approximates the rhythm of

growth:

(9)

the approximation being stronger as the diff erence from period t-1 to

period t is lower.

Consequently, the coeffi cients βi i=1,4 show the change in the

growth rate of exports at the change by 1 (100% in percentage expression) of

the growth rate in the evolution of the infl uence factors.

In order to obtain the interpretation of the β5, coeffi cient, corresponding

to a purely territorial variable, proceed analogously, but this time the fi rst

order diff erences will be made on a territorial level. We assume that pairs of

countries ij are ordered according to a certain criterion. The diff erences of the

consecutive pairs for a fi xed year would not look like this:

Romanian Statistical Review - Supplement nr. 5 / 201926

(10)

The coeffi cient β5 will now have the same interpretation as the other

coeffi cients, with the diff erence with the variance being manifested in the

territorial and not temporal plan.

Equation (6) can not be estimated directly due to the collinearity

between territorial variables of distance, Dij specifi es each pair of countries

and the constant over time and the fi xed eff ect, specifi c to each αij pair, both

having the same properties and the same territorial variation. Therefore we

will alternately remove the two variables..

• Model of the analysis of the international trade structure Trade overlaps (import and export to the same industry) are examined

by Bergstrand (1989) and Hummels and Levinsohn (1995). They have

constructed bilateral trade indices at industrial level in terms of intra-industry

trade. These indicators are aggregated nationwide and their weighted average

is explained using a gravitational equation. An alternative method used to

diff erentiate inter-industrial trade from intra-industrial trade fl ows is explained

in Fontagne, Freudenberg and Peridy (1998). In the above-mentioned works

we estimate the weights in the total trade of the types of trade, diff erentiating

in this way the vast majority of the gravitational models that generally estimate

the total volume of external sales.

Two recent works on this line are Kandogan (2004) and (2004). In

the last paper it is shown that the explanatory variables have diff erent eff ects

on diff erent components of the foreign trade and that as the economies of the

two countries and the supply of production factors become more and more

similar, the volume of horizontal intra-industrial trade increases. In the model

specifi ed for total trade, the variables are entered in the logarithm form:

(11)

αi, γj represents the constant (fi xed eff ect) aff erent to each country, λt

represents the trade eff ect of each year t (the eff ect of the economic cycle), δij the bilateral eff ect on trade (the special relationship between two countries not

surprised by the explanatory variables) , and the other variables appearing in

the model in the proper order are: distance, cumulative production of the two

countries, average output per capita, absolute variation of the real exchange

Revista Română de Statistică - Supliment nr. 5 / 2019 27

rate, total foreign exchange reserve, country similarity and diff erence in

endowment with factors of production. The last two variables will be detailed

in the following because they are not directly observable from offi cial statistics.

The SIM variable takes the value ln (0.5) when the cloudy ones get identical

production, high degree of similarity and decrease when the diff erence

between countries increases:

(12)

The diff erence in production factor, RF, is calculated according to the

capital stock K and the labor force L of the partner countries i and j at time t

following the following formula:

(13)

The capital stock, K, can be obtained by means of gross fi xed capital

formation. This indicator takes the value 0 when countries have the same

production factor endowment rate and increase with increasing country

diff erences.

The same type of model was then applied to import components to

capture how causal variables exert infl uence on the components. Internal trade components were identifi ed as intra-industry trade, vertical and horizontal, as

well as inter-industry trade. Intra-industry trade is calculated by formula:

(14)

where:

Mkijt = importing country i from country j into industry k.

The formula for inter-industry trade is:

(15)

The horizontal intra-industry imports can be defi ned as intra-Austrian

imports with the same product type p:

(16)

where:

Mkpijt = represents imports in country and country j for product p in

industry k at time t.

Romanian Statistical Review - Supplement nr. 5 / 201928

Imports of vertical intra-industry, ie trade in the same industry but with diff erent

products or products of diff erent processing grades, are thus calculated:

(17)

• Estimating the eff ects of regionalization in international trade The gravitational models have been widely used to assess the

infl uence of commercial policy measures on trade fl ows and, in particular, the

infl uence of regional integration agreements. If we consider the example of

the two countries between which a regional integration agreement has been

concluded, an alternative variable that takes the value 1 may be introduced if

the two countries are at a time t in the bilateral agreement and 0 otherwise. If

the estimated parameter of the alternative variable is positive and signifi cant

then it can be concluded that regionalization creates trade fl ows. This estimate

can be made in order to simulate the commercial potential corresponding to

any regional integration between diff erent groups of countries.

An example of a model for which the most important regional

agreements are considered, including the European Union, is that used by

Soloaga and Winters (2001). The model used also takes into consideration

traditional and variable variables such as those mentioned above. The equation

empirically tested on the imports of 58 countries during 1980-1996 is:

(18)

The value of country and country imports is explained by GDP,

population, two distance variables, country surface, alternative variables for

the existence of the common border, insular or continental country and cultural

proximity (common language). These variables common to diff erent models

estimate the volume of imports independent of the existence of regional

policies. In addition to these variables, specifi c variables are introduced to

estimate the eff ects of regionalization. Pk is an alternative variable that takes

the value 1 if country i or j is a participant to the k agreement, the bk coeffi cient

shows the higher the trade if both countries are part of the k agreement, the mk

coeffi cient shows the higher the country’s imports and is part of the agreement

against all its trading partners and the nk coeffi cient shows the higher the

exports of the country participating in the agreement k to all trading partners.

Revista Română de Statistică - Supliment nr. 5 / 2019 29

Other examples of studies are those conducted by Cernat (2001),

which analyzed trade agreements between developing countries in so-called

south-south trade Zarzoso and Lehman (2002) applied to the Mercosur and

EU countries, Baier and Bergstrand (2002) et al.

• Exchange rate volatility (monetary unifi cation) A signifi cant work that compares the eff ects of monetary union with

the eff ects of exchange rate volatility is that of Rose (2000), which shows that

there is a positive eff ect of monetary union on trade and a negative eff ect of

exchange rate volatility on it. The explanatory factors appearing in the bilateral

trade equation proposed by Rose between two countries i and j represent both

territorial variables and temporal variables:

(19)

Thus, bilateral trade fl ows - are explained by GDP (Y), population

(Pop), geographical distance (D), alternative variables that show existence or

nonexistence: common border (Cont), common language (ComCol, Colony),

alternative variables that show countries belonging to a Free Trade Agreement

(FTA) or a monetary union (CU) and the volatility of the nominal exchange

rate between partner countries

• Estimation of commerce at product level Dascal, Mattas, Tzouvelekas (2002) used a gravitational model to

analyze the eff ects of foreign exchange appreciation, production growth and

integration in European space on wine trade. Exports and imports of country i

(EU member) to country j are modeled using equations:

(20)

The explanatory variables are GDP per capita Y, D variable, Unitary

P, E exchange rate, A wine production index and EU membership, EU. It

is noteworthy that gravity models applied at the product level involve the

Romanian Statistical Review - Supplement nr. 5 / 201930

introduction of price variables that are not included in the models for the

aggregate volume of trade.

• Using the gravitational model in the analysis of international

trade fl ows

Estimating the commercial potential is certainly the central point of

using the gravitational model. (Wang and Winters, 1991; Havrylyshyn and

Pritchett, 1991; Baldwin, 1993; Gros and Gonciarz, 1995; Schumacher, 1995

and 1997; Festoc, 1996). The fi rst step is to select countries where trade

potential is presumed to have been achieved. In a symmetrical manner, bilateral

trade fl ows between the two countries are considered. We then estimate the

parameters of a gravitational equation that explains bilateral exports in the

example. This equation is used to simulate a natural bilateral trade between

any two countries, starting from dependent variables such as the distance

between the two countries and the population of the two countries. These

bilateral exports resulting from simulation are compared to registered exports

to deduce bilateral export potential. This method can be explained at both

macroeconomic and industrial level.

One of the variants developed by the International Trade Center

(CIC) Market Review Section by L. Fontagne and J.M. Pasteels, known as the

„TradeSim” second version fall into this categorical pattern. This model has

been tested for both sectoral and total data fl ows and has the following general

formula for estimating the potential for external trade:

(21)

where:

i = exporting country;

j = importing country;

Xij = trade between countries i and j;

Yi = GDP of the country i;

di = population density of the country i;

cnfl ij = the intensity of the confl ict between the two countries;

ISDi = foreign direct investment per capita for the country i;

lg = linguistic diversity in the country i;

tel ij = product density of telephone lines in countries i and j;

Dij = distance between i and j;

Revista Română de Statistică - Supliment nr. 5 / 2019 31

B ij = if countries i and j are neighbors (= 1), if not (= 0);

T ij = degree of bilateral access to the market (for trade between i and j);

clt ij = the bilateral standard for the customs and traditions common to

the two countries.

This variant represents an extension of the basic gravitational model

by adding new variables such as the linguistic diversity between the partner

countries, the existence of common borders, the existence of some important

moments of intersection in historical evolution, the use of a common currency,

the level of tariff barriers and not the latest information infrastructure. Usually

these variables are introduced as alternate variables in the gravitational

equation.

The CIC’s gravitational model was generally developed to analyze

the trade potential of developing countries and economies in transition.

Income and distance are the traditional variables most used in

gravitational models. For a quantifi cation of earnings in general, Gross

Domestic Product or total per capita is used based on the specifi ed model. On

the one hand, the GDP of the exporting country shows the production capacity

and therefore its export. On the other hand, the importing country’s GDP, as a

representation of its revenue, shows the purchasing capacity of the importing

country. Therefore, the GDP of both countries is directly correlated with the

volume of trade fl ows. The use of per capita GDP is justifi ed by the fact that countries with a near living standard have preferences or similar demand. and for countries with high living standards, the share of foreign goods is higher. In general, the nominal incomes converted into the exchange rate for that period are used. However, income elasticity of trade may be altered when developing or transition economies are considered. The use of PPPs (Purchasing Power Parity) can also lead to changes in trade elasticity according to income levels. Finally, it has turned out that sometimes PPP is more appropriate to estimate the long-term commercial potential, a horizon in which the evolution of the exchange rate approaches equilibrium. In the short term, however, it is more appropriate to use the nominal exchange rate. Another factor of infl uence which, due to its importance, has begun to occur frequently in gravitational models is the degree of market accessibility. Because the gravitational model is generally bilateral, a bilateral measure of market access that takes into account all preferential regimes is necessary. One solution is provided by Bouet (2001) which proposes an indicator that includes all types of taxes, tariff s, contingencies including anti-dumping

measures at a single value. These values for each pair of partner countries are

included in the MAC Map database. A too high or too low tariff involves too

high or too low imports, and their contribution to general protection is reduced

Romanian Statistical Review - Supplement nr. 5 / 201932

or increases. Using national imports as weights leads to an underestimation of

the level of protection.

Until the construction of the abovementioned database, there have

been widely used alternative variables for the existence of regional agreements.

Because in general the countries in an agreement are generally neighbors or

countries with a close historical past, there is a risk of multicollinearity, where

the parameters are not uniquely determined.

Cultural factors are often introduced into the gravitational model in the

form of alternative variables that typically range between 0 and 1. The complexity

of cultural aspects is much simplifi ed in most gravitational models by reducing

cultural factors to the national language (either offi cial, or spoken language)

and colonial ties. Extremely useful data can be downloaded from „Exporters’

Ecccyclopedia” (Encyclopedia of Exporters) edited by Dun & Bradstreet.

Typically, in the traditional gravitation model, transaction and

transportation costs are determined by two variables: the existence of a

common border and the physical distance between the two countries. As will

be seen later, more recent models include other explanatory variables for

transaction costs.

• The existence of common borders is generally represented by

an alternative variable that takes the value 1 if the partner countries are

neighboring countries or the value 0 otherwise.

The distance is represented by the length of the circle arch between

the capitals or main cities of countries i and j. Latitude φ and length λ, the two

cities are initially transformed into radians (II / 360) and then the distance is

calculated according to the following formula:

(22)

where:

z = 6367 (if the distance is expressed in km)

Loungani, Mody and Razin (2002) launch the idea that the distance

variable surpasses, besides the actual transport costs, also the information and

research expenditures of the market of the destination country. To dramatically

capture the eff ect of information and research spending, the authors proposed

to introduce a variable to capture the intensity of the information structure.

This variable is calculated as the product of the number of telephone lines per

capita in the two partner countries.

Revista Română de Statistică - Supliment nr. 5 / 2019 33

Another factor infl uencing the volume of external trade is the quality

of the transport infrastructure, which can be appreciated by the percentage of

paved roads in the total length of the roads or as the density of the length of the

railway tracks (surface length of the railroad). Typically, variables that express

the quality of the infrastructure, either information or transport, are strongly

correlated with each other and with GDP per capita. Therefore, using them

within the same model raises questions.

Large countries tend to develop a good trade in their country. This is

why the total surface of a country can be used to explain the volume of trade

directed towards the outside.

The existence of the Heidelberg International Confl ict Research

Institute opens the possibility of introducing a confl ict of interest in explaining

trade fl ows. According to the defi nitions developed within this institute, there

are four major forms that characterize the intensity of international confl icts:

latent confl ict, crisis, severe crisis and war, which can be assigned values from

1 to 4 in order of increasing the intensity of the confl ict state. The variable that

is likely to be introduced into a model must be a combination of the intensity

of the confl ict state and its duration.

Linguistic diversity in a particular country is considered a stimulus of

international trade. The index of linguistic diversity is the likelihood that two

people randomly chosen will have diff erent mother tongues. The closer this

index is to 1, the linguistic diversity in that country is greater.

The degree of intellectual training creates prerequisites for commerce,

but it is a strongly correlated variable with per capita GDP and therefore it is

not recommended to introduce the two variables into the same model.

FDI fl ows per capita show the attractiveness a country enjoys

externally, shows the degree of economic openness, the stability of the

economic and legislative environment, leads to the development of the

technological environment and international marketing. All these premises

and eff ects of FDI can create the conditions for a favorable environment for

the development of foreign trade. It is necessary, however, to mention that the

impact of FDI on exports depends on the nature of the investments and on

the size of the host country. Investments in large countries such as Russia are

primarily directed towards the domestic market, unlike countries like Estonia

for example.

To create the most comprehensive explanatory variable for trade

fl ows between two partner countries, it would be ideal to use bilateral FDI

fl ows between the two countries. Unfortunately, bilateral FDI fl ows are only

available for OECD countries.

Romanian Statistical Review - Supplement nr. 5 / 201934

• Using the INTERLINK model in generating the foreign trade equations

INTERLINK global equilibrium model developed by the OECD is a

representation of the world economy and is composed of a set of sub-models

for each OECD member country with trade and fi nancial equations with six

regions consist of non-OECD countries. With its over 4,000 equations, the

INTERLINK model treats the world economy as an integrated one, capturing

multiple aspects of it, both in terms of individual economies and in terms of

international ties. This model, estimated on quarterly data, has an operational

role in the OECD projections and simulations that are presented in the OECD

Economic Outlook.

Originally, the INTERLINK model was designed as a model of

world trade that gradually expanded by adding aggregate supply and demand,

average salary to economy, key commodity prices, monetary aggregates,

interest rates, exchange rates, of state budgets and investment fl ows.

Export relations, generally considered to be essentially demand-

driven, represent the behavior of commercial agents on an international

market that possesses a certain degree of homogeneity and which leads

to somewhat similar behavior of actors on the international market. In a

pattern of international trade, we can therefore expect that the parameters

that characterize exporters’ behavior on a certain market will show a certain

degree of similarity that can justify approaching world trade through a system

of equations, along with certain restrictions to ensure the consistency of the

aggregate trade of individual countries with aggregate aggregate demand in

the world.

The set of export equivalences in the INTERLINK model, like

many other specialty literature models, starts from the premise of an inverse

relationship between export performance and international competitiveness.

The export performance of a country is quantifi ed as the market share (the

volume of export compared to the demand of the destination market, which

in turn is determined as a weighted average of the countries’ imports from the

intentional market). Competitiveness on the international market is quoted in

terms of relative export prices, with the prices of competitors in the alternative

markets being weighted and summed up.